Introduction to the Securities Litigation and the Lack of Internal Controls

Securities Litigation and the lack of internal controls rarely begins with a single bad decision. More often, it begins with a system that quietly permits bad decisions to accumulate, go undetected, or go unreported. In modern enforcement and private shareholder litigation, one theme appears with consistent frequency: allegations that a company lacked effective internal controls. When internal controls fail, financial reporting quality deteriorates, disclosure risk rises, and the probability of a restatement, regulatory inquiry, or shareholder suit increases.

The market’s expectations are not ambiguous. Public companies are expected to maintain robust internal control over financial reporting (ICFR), effective disclosure controls and procedures (DCP), and corporate governance mechanisms that identify and escalate risk before it becomes a public crisis. When those expectations are not met, securities litigation often follows, anchored in the argument that investors were misled because the company’s control environment did not support reliable reporting or timely disclosure.

This article explains how internal control weaknesses become securities claims, why “control problems” are frequently framed as “disclosure fraud,” and what boards and executives can do now to reduce future litigation exposure.

If you need reprentation in securities class action lawsuits, or you have additional questions about securities litgation, corporate govrnance, your shareholde rights, call Timothy L. Miles today for a free case evaluation. 855-846-6529 or [email protected] (24/7/365).

Inadequate Internal Control

Poor internal controls have become a bigger trigger for securities litigation since the Sarbanes-Oxley Act of 20022 came into effect:

- Executive certification requirements: CEOs and CFOs must sign off on financial statements. They need to verify they have reviewed reports and confirm these documents tell the truth. Executives who knowingly approve incorrect financial reports face USD 1.00 million fines and possible 10-year prison terms.

- Prevalence in litigation: Internal control claims and restateement cases made up 14% of securities class action cases in 2025, leading to accounting violations which accounted for another 16% of federal securities class actions in 2025,

- Common control deficiencies: Problems often stem from poor staffing and technical expertise, weak review processes, bad account reconciliation, loose controls over quarterly provisions, and simply not having robust corporate governance controls.

Studies show that auditors who issue adverse internal control opinions might reduce their legal risk in shareholder lawsuits. Companies might benefit from spotting and sharing control weaknesses instead of hiding them.

Disclosure Controls and Procedures (DCP)

DCP are designed to ensure that information required to be disclosed in periodic and current reports is recorded, processed, summarized, and reported within the time periods specified by SEC rules and forms. DCP also addresses escalation and communication, meaning the organization’s ability to elevate relevant information to the right decision-makers in time to disclose.

In litigation, plaintiffs frequently allege that DCP failed when a company did not disclose known trends, uncertainties, or adverse events, or when it issued overly confident risk disclosures that did not match operational reality.

Why Control Failures Become Securities Lawsuits

Internal control deficiencies, on their own, do not automatically create private liability. The litigation risk emerges when control problems intersect with market-facing statements, such as earnings releases, SEC filings, investor presentations, and public guidance. Control failures are used in complaints as evidence of one or more of the following:

- False or misleading statements about financial results, operational metrics, or business performance.

- Misleading statements about risk, including “risk factors” that describe a threat as hypothetical when it is already materializing.

- Misleading statements about compliance, particularly when a company claims to maintain strong controls, high integrity, or robust governance.

- Scienter or recklessness, meaning the company and its executives knew, or were reckless in not knowing, that statements were inaccurate.

Control allegations also serve a strategic pleading purpose. Plaintiffs may not initially have access to internal documents. Control failures, restatements, auditor changes, and late filings are public signals that can support an inference that management lacked a reasonable basis for its statements.

Repetition matters. If a company repeatedly discloses control deficiencies, repeatedly delays remediation, or repeatedly reports “progress” that does not translate into measurable improvement, the narrative becomes one of governance failure rather than isolated error.

Such scenarios often lead to securities litigation, which serves as a vital mechanism for investor protection against corporate misconduct.

Common Litigation Pathways: How the Story Typically Unfolds

While facts vary across industries, securities litigation tied to internal controls often follows a recognizable sequence.

Improve Disclosure and Transparency Practices

Clear disclosure and transparency practices shield companies from securities litigation. Your company needs structured processes to review and share information. This builds trust with stakeholders and protects the organization.

Review public statements and filings regularly

A systematic review of corporate communications helps you avoid inconsistencies that could trigger securities class actions:

- Line up board minutes with public disclosures – Make sure your company’s public statements and filings reflect what happens in board meetings. Use board minutes as your guide when drafting disclosure documents to keep everything in sync. Differences between boardroom decisions and investor communications might lead to claims of misleading disclosures.

- Set up regular certification processes – Following Sarbanes-Oxley, many companies now use disclosure controls to back up CEO and CFO certifications. You might want to add:

- Sub-certification procedures for ESG and financial data

-

- Ways to protect people who report concerns

- Keep information similar across platforms – Your message should stay consistent across all disclosure channels. Numbers and metrics should match exactly whether they appear in proxy statements or on corporate websites. Different numbers on different platforms could lead to SEC questions and make investors doubt your information’s reliability.

- Keep detailed records of oversight activities – About 20% of Fortune 100 companies share what they did based on board evaluations. These records show careful oversight and can prove proper governance if litigation occurs.

Quick disclosure plays a significant role too. Sharing information quickly, even preliminary data, helps stakeholders make better decisions and manage their expectations. This works especially well during company restructuring or other major events.

Work closely with legal and investor relations teams

Strong communication between board committees and corporate teams improves transparency and lowers litigation risk:

- Make use of disclosure committees – Many companies created disclosure committees after Sarbanes-Oxley. Senior officers from accounting, legal, investor relations, tax, internal audit and key business units usually join these committees. Make sure ESG committees work closely with disclosure committees to share information easily.

- Create clear review steps – Your disclosure committee should review ESG reports, website content, and standalone reports. The committee should also share relevant SEC reporting details with management teams to keep everything consistent.

- Work better with investor relations – IR professionals help relate market and company news while managing investor views. They should:

-

- Gather and study company and industry information early

-

- Present negative news carefully to reduce investor concerns

- Plan for crisis communication – Clear communication during tough times shows you take responsibility and care about stakeholders. Companies need to:

-

- Explain their action plans clearly

These practices do more than just protect against litigation. Boards that share information about their evaluation process show their dedication to good governance. Fortune 100 companies that improved their board evaluation disclosures saw better director training programs, board structure, and governance documentation.

Good transparency should run through your whole organization, starting at the top. Clear rules and strong processes help share information responsibly and consistently. This builds trust – your best defense against securities litigation.

Conduct Regular Risk Assessments

Proactive risk assessment is the life-blood of good board oversight. It helps directors spot and reduce potential securities litigation risks early. A regular, structured review of both old and new risks gives corporate boards an edge in today’s fast-changing business world.

Identify litigation-prone areas

Boards need a systematic way to spot litigation risks through structured assessment practices:

- Maintain complete risk registers – Management should document all enterprise-wide risks and assign specific board committees to oversee them. This practice ensures every major risk area gets board attention.

- Implement critical self-questioning processes – Directors should ask themselves if they can:

-

- Describe the company’s risk management framework clearly

-

- Name the organization’s top risks without hesitation

- Check risk assessments against external standards – Boards should compare management’s risk list with industry reports and sector analyses to verify everything is covered. External checks help find blind spots in internal assessment processes.

- Document all oversight activities well – Board minutes need to show careful review of key risks to create a clear oversight record. These documents serve as vital proof of meeting fiduciary duties if litigation happens.

- Set clear committee duties – Risk oversight should go to the right committees—financial risks to audit teams, HR risks to compensation committees. This approach ensures each risk type gets expert attention.

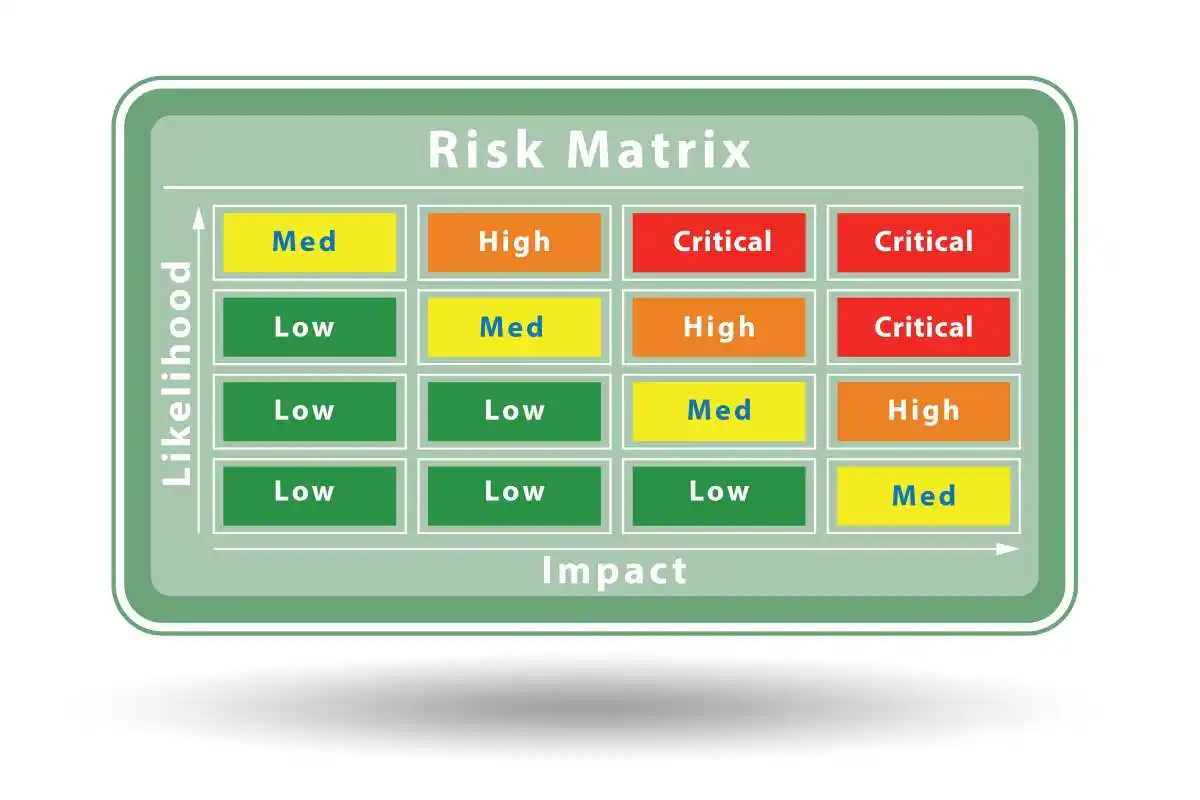

A structured assessment method builds a stronger defense against litigation claims. Good boards rate risks on impact (1-3) and likelihood (1-3), then multiply these scores to set priorities. This numbers-based approach helps put resources where they matter most.

Shareholder Claim: Misstatement, Causation, Damages

Plaintiffs typically allege that the company’s statements were false or misleading and that investors suffered damages when the truth emerged. Allegations regarding internal controls are often used to support the claim that misleading disclosure was not an accident but a foreseeable outcome of governance and control failures. Effective [internal controls that detect financial statement fraud](https://classactionlawyertn.com/internal-controls-that-detect-financial-statement-fraud3/) can help prevent such situations.

Prepare for Shareholder Class Actions

Corporate boards face major threats from shareholder class actions that demand legal expertise and readiness to respond. Securities class action lawsuits grow more complex each day, and boards need strategic preparation beyon simple governance practices to handle potential legal challenges.

Understand the Simple and Affiliated Ute presumptions

You can develop better defense strategies by knowing the legal presumptions that govern securities class actions:

- The Affiliated Ute presumption applies when we base claims on omissions, which lets courts presume reliance in cases that focus on omissions rather than affirmative misstatements

- Courts have determined this presumption doesn’t apply when “the claims of fraud at issue were not based primarily on omissions”

- The Basic presumption connects market efficiency and price impact, and defendants must prove lack of price impact during class certification

- The Sixth Circuit joins other courts to create a “high hurdle” for accessing Affiliated Ute’s “narrowly viewed” reliance presumption

- Courts use multi-factor tests to analyze whether claims focus on omissions, which helps determine the applicable presumption

Develop a litigation response plan

A well-laid-out litigation response framework helps minimize disruption when lawsuits begin:

- Create a dedicated litigation team with members from legal, IT, human resources, and other key departments to handle securities litigation awsuit responses

- Use data preservation protocols to map data sources and identify relevant information quickly, and keep records for at least ten years

- Provide securities litigation response training to employees who manage commercial relationships or handle sensitive data about preserving attorney-client privilege and document obligations

- Select specific team members to assess when the company should become lead plaintiff or opt out of class actions based on loss thresholds

- Create clear procedures with custodian banks for handling settlement notices and filing proof of claim forms on time

Legal understanding and operational readiness are vital to prepare for securities class actions. Boards show due diligence during litigation by knowing reliance presumptions and implementing structured response plans.

The Legal Theory: From Control Weakness to Misleading Statement

To understand why internal controls are central in securities litigation, it helps to understand how plaintiffs connect controls to disclosure.

Misrepresentation by Financial Reporting

- If a company issues financial statements that later require correction, plaintiffs may argue that the original statements were materially false.

- A restatement is not proof of fraud, but it can strengthen allegations that the company lacked a reasonable basis for its reporting.

- This is where having [top internal controls for fraud prevention](https://classactionlawyertn.com/top-internal-controls-for-fraud-prevention/) becomes crucial.

Misrepresentation by Omission

- A company can face claims not only for what it said, but also for what it failed to disclose.

- If management knew of material problems but did not disclose them, the omission may be framed as misleading, especially when the company simultaneously made optimistic statements about performance, compliance, or risk management.

Misstatements About Controls Themselves

Public companies often state in periodic filings that:

- Disclosure controls are effective.

- ICFR is effective.

- There were no material changes in internal controls.

- Identified weaknesses are being remediated.

If those statements are contradicted by later disclosures or auditor findings, plaintiffs may argue the company misled investors about the reliability of its reporting infrastructure. Such scenarios often stem from weak internal controls and can lead to false financial statements. Furthermore, these instances could potentially result in securities fraud class actions, emphasizing the need for robust internal control systems in preventing securities fraud.

Scienter and the “Control Narrative”

In many cases, the primary dispute becomes whether the defendants acted with the required state of mind for fraud claims. Control failures can be used to support scienter allegations by arguing:

- The issues were pervasive and long-standing.

- The company had repeated warnings, such as audit findings, whistleblower complaints, or regulator interactions.

- Executives signed certifications attesting to controls and disclosure quality.

- The company pursued aggressive accounting or guidance in spite of known deficiencies.

The central idea is repetition and foreseeability. Controls are the system designed to prevent misstatements. If that system is demonstrably weak, plaintiffs argue that misleading disclosure was not merely possible, but likely.

Red Flags That Commonly Appear in Complaints

Securities complaints tied to internal controls frequently reference identifiable red flags, many of which are preventable with disciplined governance.

Restatements and Revisions

A restatement is often the most visible signal of reporting failure. Even when the root cause is an error rather than misconduct, litigation may allege that the company’s prior statements lacked a reasonable foundation.

Material Weaknesses That Persist Across Periods

One material weakness can occur even in mature organizations. The litigation risk increases when:

- Weaknesses remain unremediated for multiple reporting periods.

- Remediation plans are vague, delayed, or not resourced.

- Management claims progress without demonstrating measurable control improvements.

Rapid Growth Without Control Scaling

High-growth companies are particularly exposed when:

- Financial operations lag behind revenue scale.

- Acquisitions are integrated without control harmonization.

- International expansion outpaces governance capacity.

Growth is not a defense. In litigation, it is often framed as the reason controls should have been strengthened earlier.

Auditor Turnover and Disputes

Changes in auditors, especially abrupt resignations or reportable events, are frequently highlighted as evidence of reporting instability.

Critical Warning Patterns That Signal Manipulation

- Revenue-Expense Disconnections: Manifest through systematic patterns that careful analysis can detect before they escalate into major fraud cases:

-

- Timing Discrepancies: Revenue rises while cash flow remains stagnant or decreases, typically indicating fabricated sales or inappropriate revenue recognition practices. Companies may recognize expenses in different periods than their related revenues, creating artificial profit improvements that violate basic accounting standards.

-

- Unexplained Financial Fluctuations: Sudden changes in revenues or expenses occurring without corresponding operational activities often signal deliberate manipulation. These patterns become particularly suspicious when certain expense categories decrease unusually despite revenue growth.

-

- External Verification Contradictions: Companies whose quarterly change in Google Trends search volume ranks in the bottom quartile while reported revenue growth ranks in the top quartile demonstrate 165% higher odds of subsequently restating their initial reported revenue. This external metric provides crucial verification because it remains outside management control.

-

- Suspicious Documentation Patterns: Round expense figures ($100.00, $250.00) appearing frequently across financial reports may indicate estimation or fabrication rather than actual documented costs. Excessive use of “miscellaneous” expense categories often conceals inappropriate purchases requiring investigation.

Frequent Changes in Accounting Methods: Manipulation Through Policy Shifts

- Consistent Application: Consistent application of accounting principles forms the cornerstone of reliable financial reporting and market transparency. Frequent changes in accounting methods represent a sophisticated form of financial statement fraud that enables management to manipulate reported results while maintaining an appearance of regulatory compliance.

- Pattern Recognition: Financial analysts and auditors identify frequent accounting policy alterations as critical indicators demanding immediate investigation and enhanced scrutiny.

Why These Mismatches Create Substantial Legal Exposure

- Fundamental Accounting Violations: Expense and revenue mismatches directly contravene the matching principle, which mandates that expenses be recognized during the same period as their related revenues. This violation transforms financial statements from reliable business indicators into misleading documents that can trigger securities litigation.

- Earnings Management Opportunities: These mismatches provide management with powerful tools for manipulating reported performance. Decision-makers can deliberately shift expenses between reporting periods to smooth earnings, meet analyst expectations, or trigger executive compensation bonuses—all practices that distort actual operational efficiency.

- Systemic Governance Failures: Research demonstrates that firms engaging in expense manipulation typically exhibit broader control weaknesses, including disproportionate accounts receivable growth and insufficient bad debt allowances. These companies frequently employ “common channels for upward earnings management” across multiple financial statement areas, creating comprehensive deception schemes.

- Subjective Judgment Vulnerabilities: Expense recognition offers particularly attractive manipulation opportunities because many expense-related items depend on management estimates for warranty provisions, doubtful accounts, and depreciation schedules. These subjective areas provide extensive room for inappropriate adjustments while appearing legitimate to casual observers.

Industry-Specific Exposure: Controls Fail Differently Across Sectors

The sources of internal control risk vary by sector, but the litigation pattern remains consistent. Securities litigation can arise from various sectors due to specific control failures.

- Technology and SaaS: revenue recognition, contract modifications, multi-element arrangements, and KPI governance.

- Biopharma and life sciences: disclosure of trial data, regulatory interactions, and going concern assessments.

- Financial services and fintech: credit loss reserves, compliance controls, model risk management, and transaction monitoring.

- Manufacturing and retail: inventory valuation, shrink reserves, supplier rebates, and cost capitalization.

- Energy and extractive industries: reserves accounting, impairment, and environmental liabilities.

The forward-looking implication is straightforward. Control design should reflect business model risk. Generic controls create generic coverage, which is rarely sufficient when litigation follows a specific accounting or disclosure failure.

Systematic Detection Strategies for Investment Protection

- Ratio analysis and trend evaluation provides the foundation for identifying problematic expense-revenue relationships through mathematical precision rather than subjective assessment.

- Financial Relationship Analysis: Calculate expense-to-revenue ratios across multiple periods to identify unusual variations. Revenue growth rates should generally parallel expense growth rates unless clear operational changes justify divergence.

- Timing Verification Procedures: Examine whether expenses align with their corresponding revenues in appropriate periods. Unusual expense deferrals or accelerations without clear business justification warrant immediate investigation, particularly when occurring near period-end dates.

- Category-Specific Scrutiny: Compare warranty expenses against historical patterns and industry standards. Evaluate bad debt allowances relative to accounts receivable growth patterns. Review depreciation methods and useful life assumptions for potential manipulation.

- Third-Party Validation Methods: Cross-reference reported business activity with external data sources including web traffic patterns and search trends. Analyze expense reports across similar employee roles to identify statistical outliers.

- Continuous Monitoring Framework: Regular audits—both systematic and random—create essential safeguards against expense manipulation. Categories requiring substantial management judgment demand heightened analytical attention due to their elevated manipulation potential.

- Professional Skepticism Application: Companies achieving exceptional margin improvements without corresponding operational changes require comprehensive investigation. Sudden expense pattern modifications rarely occur naturally without substantial business model adjustments or technological innovations that management can clearly document and explain.

The Strategic Disclosure Question: When Control Issues Become Material

A recurring challenge is determining when internal control issues, audit findings, or operational breakdowns rise to the level of material disclosure. Materiality is facts-and-circumstances based, but the litigation risk increases when companies:

- Delay disclosure of known weaknesses.

- Use boilerplate risk factors that do not reflect current conditions.

- Frame known problems as hypothetical risks.

- internal control issues, audit findings

A proactive approach emphasizes internal escalation and early evaluation. The goal is not maximal disclosure. The goal is accurate disclosure, consistent with the company’s real risk posture.

Common Triggers of Securities Litigation

Securities class action lawsuits do not just appear out of nowhere. Corporate boards need to know what sparks these legal challenges to take preventive steps before issues get worse. Let’s look at three main triggers that need your attention.

Misleading disclosures and omissions

Information shared—or not shared—with investors is the life-blood of securities litigation. Recent patterns show that small disclosure issues can create big legal problems:

- Material misstatements: The Securities Act holds companies liable when publicly filed documents contain material misstatements or omissions during registered securities offerings. These include false financial metrics, inflated revenue projections, or misrepresented business relationships.

- Half-truths vs. pure omissions: The Supreme Court ruled in Macquarie Infrastructure Corp. v. Moab Partners, L.P.. in 2024 that “pure omissions are not actionable under Rule 10b-5(b)“. The failure to disclose required information can still support a claim if it makes other statements misleading. The difference lies between saying nothing (pure omission) and making statements that become misleading without context (half-truth).

- Burden of proof elements: Plaintiffs must prove three critical elements in fraud claims under Section 10(b) of the Securities Exchange Act: falsity (a misleading statement), scienter (intent to defraud), and causation (stock price inflation from false statements and subsequent drops when truth emerged).

These cases pack a punch financially. NERA reports that combined settlement amounts for cases settled in 2022 hit USD 4.00 billion, which is USD 2.00 billion more than the inflation-adjusted amount in 2021.

Conclusion: Internal Controls Are a Litigation Control, Too

Internal controls are often discussed as accounting infrastructure. In reality, they are litigation infrastructure. A company with effective controls produces accurate reporting, reliable disclosure, and documented decision-making. Such internal controls are also crucial in preventing fraud. On the contrary, a company with weak controls produces uncertainty, corrections, surprises, and market shocks. Securities litigation is frequently the downstream consequence, often linked to poor corporate governance.

Robust corporate governance reduces this risk through repetition and discipline: repetition in testing, repetition in escalation, repetition in remediation, and repetition in oversight. Organizations that invest early in control maturity, disclosure rigor (following guidelines such as those outlined in this materiality assessment guide), and board-level accountability are not merely complying with standards. They are protecting shareholder value, preserving credibility, and positioning the company for sustainable access to capital.

In a market that increasingly prices governance quality, internal controls are not an administrative requirement. They are a strategic asset and a proactive defense against potential litigation risks associated with weak corporate governance.

Frequently Asked Questions about

What role do internal controls play in securities litigation?

Internal controls are critical in securities litigation because their failure often leads to poor financial reporting, increased disclosure risks, and a higher likelihood of restatements or shareholder lawsuits. Allegations frequently focus on a company’s lack of effective internal controls, which can mislead investors about the reliability of financial statements and timely disclosures.

What is Internal Control Over Financial Reporting (ICFR) and why is it important?

ICFR consists of policies and procedures designed to ensure the reliability of financial reporting and compliance with GAAP. It is essential because material weaknesses in ICFR signal potential misstatements in financial statements, increasing the risk of securities fraud. Robust ICFR helps public companies avoid litigation related to inaccurate financial disclosures.

How do Disclosure Controls and Procedures (DCP) impact a company’s legal risk?

DCP ensure that information required by SEC rules is accurately recorded, processed, and reported on time. Failures in DCP often lead to allegations that a company did not disclose known risks or adverse events promptly, or provided misleading risk disclosures. Such lapses increase the probability of securities litigation due to investor misinformation.

Why do internal control failures often lead to allegations of disclosure fraud?

Internal control failures become grounds for disclosure fraud allegations when they coincide with public statements like earnings releases or SEC filings that are false or misleading. Plaintiffs argue that weak controls resulted in inaccurate financial reports, misstated risks, or false claims about compliance and governance, suggesting management knew or was reckless about these inaccuracies.

What are common signs that indicate a company might face securities litigation due to internal control issues?

Public signals include repeated disclosures of control deficiencies, delays in remediation efforts, restatements of financials, auditor changes, late filings, and unfulfilled promises of improvement. These patterns suggest governance failures rather than isolated errors, increasing the likelihood of investor lawsuits alleging misconduct.

How can boards and executives reduce future securities litigation exposure related to internal controls?

Boards and executives can reduce litigation risk by implementing strong internal controls over financial reporting and disclosure procedures, promptly addressing identified weaknesses, ensuring accurate and timely disclosures, enhancing communication channels for risk escalation, and fostering a culture of transparency and compliance aligned with regulatory expectations.