Introduction to Countering Common Defense Arguments in Securities Class Actions

- Securities Class Actions: You may have probably noticed something if litigating a securities class action lawsuit: defense playbooks are getting tighter, faster, and more standardized.

- The Good News: Is that most “common” defense arguments are common for a reason—they work when plaintiffs do not anticipate them early. In 2025, the edge often comes from building your record and theory to preempt the motion to dismiss, shape class certification, and box in loss causation and damages before the expert phase.

- This Comprehensive Guide: Breaks down the defense arguments you are most likely to see in securities fraud class actions (primarily Molina Healthcare Class Action Lawsuit: An Essential Guide on What You Need to Know for Your Rights [2025] and Section 20(a)), and practical ways to counter them—using tactics that align with current pleading standards, class certification realities, and the way courts analyze price impact and causation post-Halliburton.

- For Instance: Understanding the complex arena of securities class actions can significantly bolster your strategy. Whether it’s a Firefly Aerospace Class Action lawsuit or a Baxter Class Action lawsuit, having a comprehensive understanding of these cases can provide valuable insights.

- Free Case Evaluation: If you suffered losses in a securities class action lawsuit and need representation, or just have general questions about your rights as a shareholder, call, at no charge, Timothy L. Miles today for a free case evaluation. (855)-846-6529 or [email protected]. The only call you will have to make.

What Has Changed (and what has not) in Securities Litigation in 2025

Before we get into the specific arguments, here’s the practical landscape you are litigating in:

- Motions to dismiss are still the main battlefield

-

- Private Securities Litigation Reform Act of 1995 (PSLRA) and Rule 9(b) remain the choke point.

- “Tell me exactly what was false and why at the time” is still the core demand.

- Price impact fights are more sophisticated

-

- Defendants increasingly bring event studies earlier and more aggressively.

- Plaintiffs need clean event selection and leakage/overlap defenses ready.

- Courts are skeptical of “fraud by hindsight,” but receptive to well-pleaded contemporaneous facts

- Internal reports, channel checks, regulator communications, and competitor disclosures matter—when tied to the challenged statements. This is where a Whistleblower Lawyer in Nashville can play a critical role, as whistleblowers often provide key internal information that can substantiate claims.

- AI-driven disclosure review is raising the bar

-

- Both sides are using tools to compare transcripts, risk factors, guidance language, and peer disclosures.

- If your complaint reads like it missed obvious contradictions, it will be treated like it.

In some instances, like with certain medications such as Dupixent, there may be significant legal implications due to associated health risks. Similarly, in cases involving drugs like Zepbound which have been linked to dry eye syndrome, such medical disclosures could also impact ongoing securities litigation.

A quick way to use this guide on securities litigation

You can treat each section as a checklist:

- What the defense will argue?

- Why courts sometimes buy it?

- How to counter it?

- What to build into the complaint (or class cert record)?

This guide may also be useful in understanding various class action lawsuits, such as the Avantor Class Action Lawsuit, which provides insights into common arguments and judicial responses.

Similarly, the StubHub Class Action Lawsuit serves as an exhaustive investor guide that could help in comprehending the broader implications of such legal proceedings.

For those interested in the medical sector, the Inspire Medical Class Action Lawsuit offers a timeline of events that could be beneficial for understanding similar cases.

In the pharmaceutical industry, the Telix Pharmaceuticals Class Action Lawsuit provides an unabridged guide on what investors must know about class action lawsuits in that field.

Lastly, the Stride Class Action Lawsuit presents frequently asked questions that could further clarify any doubts regarding class action lawsuits.

1) “You didn’t plead falsity—this is just opinion, puffery, or optimism”

What the defense will argue in seeking dismissal under heightened pleading standards in securities litigation

The statements are:

- Immaterial puffery (“we’re well-positioned,” “strong demand”).

- Non-actionable optimism or corporate cheerleading.

- Opinion protected unless you plead disbelieved opinion or omitted material facts that make it misleading.

- Forward-looking and thus protected by the PSLRA safe harbor (see the next section).

Why courts sometimes accept it in securities class actions

- Complaints often:

- Quote hopeful language without supporting it with verifiable facts.

- Fail to explain what current facts made the statement misleading.

- Confuse “ended badly” with “was false when said.”

How to counter it (practically)

1. Tie each statement to a measurable reality

When addressing misleading statements, scienter or loss causation, it’s crucial to anchor each claim in quantifiable data. Use:

- guidance ranges

- KPI claims (churn, CAC, margin, utilization, backlog, AR days, NPL ratios)

- statements about specific products, compliance status, supply, demand, or customer retention

For example, in the context of the Perrigo class action lawsuit, shareholders can utilize measurable realities to counter false claims made by the defendant which artificially inflated stock prices.

2. Plead the “why misleading” piece like a ledger

For every misleading statement made:

- document what was said

- clarify what the market would interpret it to mean

- present contemporaneous contradictory fact(s)

- provide evidence (CW, document, regulator, competitor, data)

This approach is particularly relevant in cases such as the Dupixent cancer lawsuit, where misleading information about a medication’s effects could have serious implications.

3. Use “half-truth” framing in securities litigation and accounting fraud

Many legal victories hinge on identifying statements that are:

This strategy is especially effective when dealing with:

- risk disclosures that describe a known problem as hypothetical

- “we are monitoring” language when the problem is already manifesting

4. Be selective: Hit lack of internal controls hard along with corporate governance and accounting fraud

Choose your strongest statements wisely:

- fewer, clearer, more provably misleading claims often outweigh a long list of vague quotes

What to include in the complaint in securities litigation to overcome heightened pleading standards

Bulletproof falsity allegations often include:

- Time-stamped internal metrics (even approximate ranges)

- Specific internal warnings (emails, meetings, audit findings)

- Customer-level facts (cancellations, non-renewals, reduced orders)

- Regulatory or auditor friction (comment letters, restatement risk, control failures)

2) “Safe harbor: these were forward-looking statements with cautionary language”

What the defense will argue under heightened pleading standards

The defense will argue that the statements in question are projections, guidance, plans, objectives, or “expectations” and that they were accompanied by cautionary language. Alternatively, they may argue that the plaintiffs did not plead “actual knowledge” of falsity for forward-looking statements.

Why courts sometimes accept it

- Standard warning language can be surprisingly effective if plaintiffs don’t:

- distinguish between current false statements and predictions

- argue that the warnings were insufficient because risks had already occurred

How to counter it under heightened pleading standards

Separate present facts from future projections: show scienter through lack of internal controls

- Attack:

- “we are seeing strong demand” (present)

- “we have resolved supply issues” (present)

- “our pipeline is strong” (present)

- Don’t let defendants re-label those as “forward-looking.”

Challenge “meaningful cautionary language”

- Caution must be:

- specific

- tailored

- not purely generic

Use “risk already materialized” allegations and argue fraud on the market

- Strong pattern:

- “They warned if X happens”

- But X was already happening

- For instance, consider the ongoing issues related to Zepbound Eye Issues, which have been linked to certain medical treatments. This serves as an example of a risk that has already materialized.

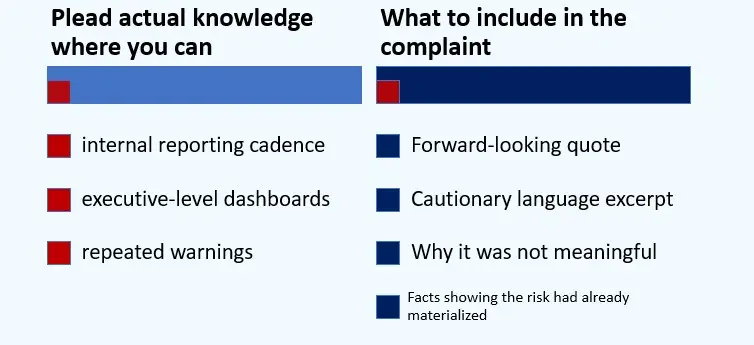

Plead actual knowledge where you can to beat scienter arguments and loss causation

- Actual knowledge can be inferred from:

- internal reporting cadence

- executive-level dashboards

- repeated warnings

- remediation failures

What to include in the securities class action lawsuits

- A simple but effective structure:

- Forward-looking quote

- Cautionary language excerpt

- Why it was not meaningful (generic, inconsistent, or contradicted by known facts)

- Facts showing the risk had already materialized

3) “Scienter isn’t strong enough—at best this is negligence or bad business”

What the defense will argue

- Plaintiffs failed to plead a “strong inference” of scienter under the PSLRA.

- Alternative inferences: honest mistake, unexpected market shift, operational challenges, competitive pressure, macro conditions

- The will emphasize :no insider trading (or only routine sales), no restatement, executives had plausible explanations

Why courts sometimes accept it in securities litigation

- Complaints often rely on:

- Allegations based on what the defendant should have known

- Relying solely on executive titles

- Generalized whistleblower statements without specific details

- Admissions made after the fact without connecting them to prior knowledge

How to counter it

1. Build scienter as a mosaic, not a single smoking gun

Combine:

- core operations + specific internal reports

- timing + magnitude of miss

- confidential witnesses with role/detail

- contemporaneous competitor signals

- regulator/auditor interactions

- admissions framed as “we were already seeing X”

2. Show motive in non-cliché ways to prove scienter

Beyond “they wanted to keep the stock price high,” focus on:

- a pending offering

- debt covenants

- acquisition currency

- executive comp tied to specific metrics

- a turnaround narrative requiring “beat and raise”

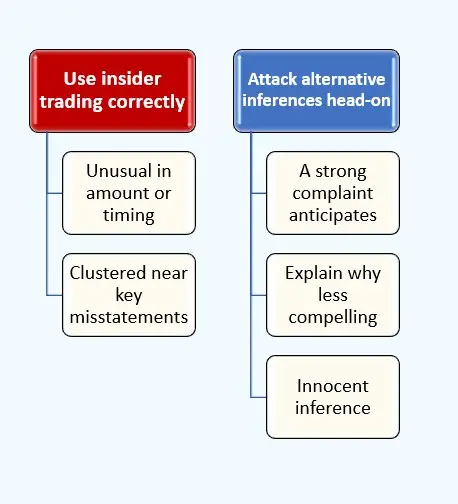

3. Use insider trading correctly for scienter

Insider sales help most when they are:

- unusual in amount or timing

- clustered near key misstatements

- inconsistent with prior trading plans

If you don’t have good sales, don’t force it—courts penalize weak trading theories.

4. Attack alternative inferences head-on and show accounting fraud

A strong complaint anticipates:

- the “innocent inference”

- and explains why it’s less compelling given the alleged reporting/alerts

What to build into securities class action lawsuits

Scienter-friendly pleading typically includes:

- who received what report, when

- how often metrics were reviewed

- what thresholds triggered escalation

- what defendants did (or didn’t) do in response

- how they spoke publicly despite those warnings

4) “Confidential witnesses are unreliable / not particularized enough”

What the defense will argue

- The defense will argue that the CWs lack basis of knowledge, are too junior, provide hearsay, and are not tied to specific time periods.

- Alternatively, the defense may argue that the allegations made by the CWs are “conclusory.”

Why courts sometimes buy it

- Courts expect:

- job titles

- time period of employment

- reporting lines

- specific meetings/documents

- Generic “former employee” allegations get discounted.

How to counter it

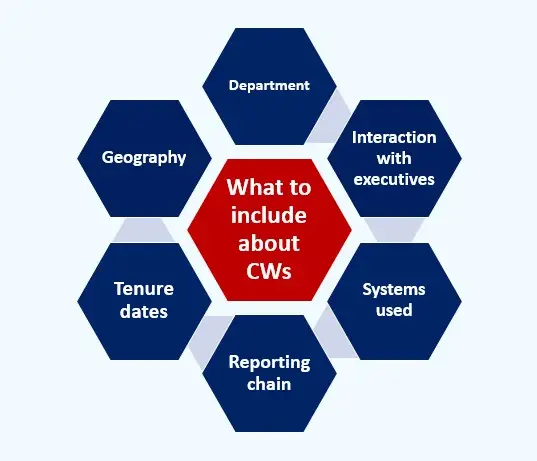

- Over-particularize CW foundations to show scienter

- Include:

- department

- geography

- tenure dates

- reporting chain

- frequency of interactions with executives

- systems used (CRM, ERP, risk dashboards)

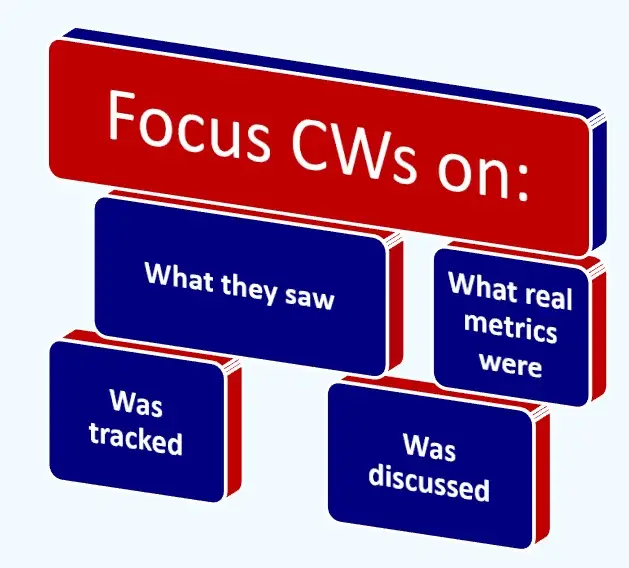

- Use multiple CWs to corroborate the same fact

- Courts trust:

- Avoid CWs opining on state of mind

- Focus CWs on:

- what they saw

- what was tracked

- what was discussed

- what the real metrics were

What to build into the complaints in securities litigation

A CW paragraph template that works:

- role + tenure + scope

- direct exposure to the topic

- specific example(s) with dates

- link to a challenged statement

For instance, if you are dealing with a case related to the Dupixent Cancer Lawsuit, you would want to include your role in the matter, how long you’ve been involved, and the scope of your involvement. Additionally, it would be beneficial to share any direct exposure you have had to the topic, provide specific examples with dates, and link to any statements that have been challenged regarding the lawsuit.

5) “No loss causation—your ‘corrective disclosure’ wasn’t corrective”

This point is particularly relevant in cases where individuals have suffered adverse effects from medications, such as Zepbound, which has been linked to serious vision problems. If you or someone you know has experienced vision loss after taking Zepbound, it may be worth exploring the possibility of a Zepbound vision loss lawsuit.

Similarly, other medications like Wegovy and Mounjaro have also been associated with vision loss. For those who have suffered Wegovy-related vision issues, or Mounjaro-induced eye problems, seeking legal advice could provide some recourse.

What the defense will argue

- The alleged disclosure:

- didn’t reveal the truth

- was merely negative news, macro-driven, or industry-wide

- was “mixed” or not new

- was leaked earlier (no surprise to market)

- Or the price drop was due to:

- interest rates, sector rotation, geopolitical events, etc.

Why courts sometimes accept it

- Plaintiffs sometimes:

- label any drop as corrective

- ignore confounding news

- fail to connect the disclosure to the alleged misrepresentation

How to counter it under heightened pleading standards

- Draft the corrective disclosure theory early: If your disclosure theory is unclear, the entire case becomes unclear.

- Use “partial corrective disclosure” and “materialization of the risk” where appropriate: Don’t overly rely on a single “truth bomb” if the truth emerged gradually.

- Separate confounders: Do this explicitly by listing other news during the same time period and explaining why the market reaction corresponds to the fraud revelation. For example, if there are reports about Wegovy causing blindness, this could serve as a significant confounder in a case related to the drug.

- Use analyst reports and market commentary: Instead of using them as filler, utilize them to demonstrate what the market learned and how that learning connected to the alleged truth.

What to build into the complaint

- Loss causation allegations that tend to hold up:

- clear timeline of revelations

- quotes from analysts tying drop to the fraud-related information

- acknowledgement of other news + why it doesn’t explain the magnitude/timing

In cases involving weight loss drugs like Mounjaro, Trulicity, Saxenda, or Zepbound, it’s crucial to consider potential side effects such as vision loss. For instance, if a patient experiences Mounjaro vision loss, they should seek legal counsel from a specialized lawyer. Similarly, those affected by Trulicity or Saxenda and suffering from vision-related complications should also consult with experienced attorneys in these fields.

Moreover, if there are any adverse effects related to Zepbound, it’s essential to reach out to a lawyer who specializes in such cases. It’s vital for patients using these medications to be extremely observant of any potential vision effects associated with GLP-1 weight loss drugs, as recent medical studies have uncovered troubling trends in this area.

6) “No price impact / Basic presumption rebutted (Halliburton II)”

What the defense will argue

- Even if statements were false, they had no price impact.

- The market did not react:

- at misstatement time (no price increase)

- at correction time (drop due to something else)

- They’ll use event studies to rebut Basic at class cert.

Why courts sometimes buy it

- Plaintiffs sometimes assume market efficiency arguments are enough.

- Plaintiffs sometimes ignore that some statements don’t move price (especially confirmatory or “maintenance” statements).

- Plaintiffs sometimes pick noisy event windows.

How to counter it

Prepare for price impact before class cert

Treat price impact as a merits-adjacent issue that shows up early. This is particularly relevant in cases like the Skye Bioscience Class Action Lawsuit, where understanding price impact can significantly influence the outcome.

Use price maintenance theory carefully

Many courts accept that some lies maintain inflation rather than increase it—but you need:

- a coherent explanation

- credible expert framing later

Choose clean event windows

Avoid:

- earnings days with lots of unrelated disclosures

- macro shock days

- multi-topic press releases

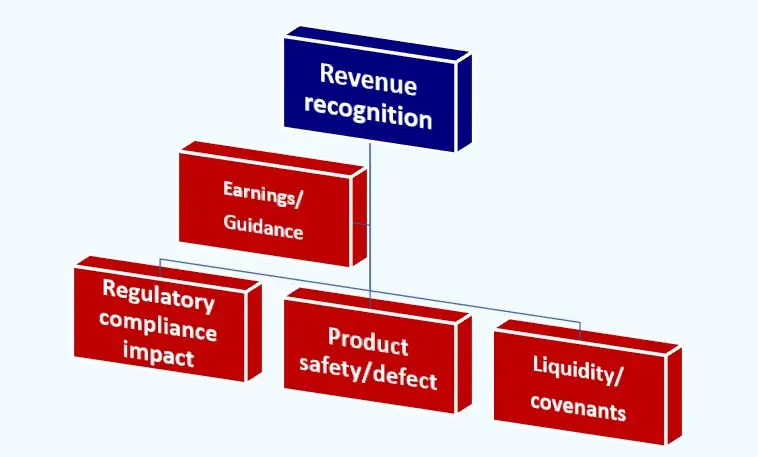

Show that the statement was the kind the market prices

Examples:

- revenue recognition

- guidance/earnings

- regulatory compliance impacting business ability

- product safety/defects

- liquidity/covenants

What to build into your record

- For class cert strategy, start collecting:

- analyst notes

- earnings call Q&A focus

- peer comps

- volatility context

- trading volume anomalies

When you’re analyzing these aspects, it’s essential to be aware of potential class action lawsuits that could impact stock performance. For instance, if you’re looking into Perrigo or Blue Owl, understanding the specifics of these cases can provide valuable insights.

7) “Truth-on-the-market: the risk was already disclosed”

What the defense will argue

- The alleged truth was already public through:

- prior filings

- industry reports

- media

- short seller publications

- Therefore:

- no material misrepresentation

- no reliance

- no loss causation

In cases where weight loss drugs have been linked to serious side effects, such as vision loss, the defense may argue that these risks were already disclosed in prior filings and industry reports. This could potentially strengthen their case for no material misrepresentation or reliance.

Moreover, if the drug in question is Saxenda, hiring a Saxenda vision loss lawyer could provide valuable insights into the medication’s mechanism of action and the scientific evidence linking it to vision loss. Such knowledge can be crucial in arguing against claims of loss causation.

Why courts sometimes accept it

- If public information is specific, widely disseminated, and clearly corrective, courts may find:

- the market already knew

How to counter it

- Don’t treat “some risk disclosure” as fatal—attack specificity

-

- A generic risk factor rarely equals:

- a disclosure of present fact

- Distinguish “risk” from “realized failure”

-

- “We may face supply constraints” is not the same as:

- “We are already unable to fulfill orders.”

- Address the alleged public sources directly

-

- If you know the defense will cite:

- an article

- a report

- a prior 10-K

- Explain why it didn’t reveal the fraud with clarity or credibility.

- Consider medical risks associated with certain drugs

-

- For example, medications like Trulicity have been linked to serious side effects such as Macular Edema, especially when combined with insulin.

- Similarly, drugs like Dupixent have faced lawsuits due to failure to warn about potential cancer risks associated with their use.

What to build into the complaint

- Side-by-side comparisons:

- what defendants said

- what the public sources actually said

- what was missing (timing, magnitude, confirmation)

When addressing medical complaints related to prescription medications, it’s crucial to highlight the discrepancies between the defendants’ statements and the actual experiences of patients as reported in public sources. For instance, Trulicity has been associated with some severe side effects, particularly concerning vision loss. Similarly, Zepbound and Saxenda have also been reported to cause debilitating vision problems. It’s essential to compare these documented side effects with what was communicated by the defendants at the time of prescription.

Moreover, if a patient has been prescribed Dupixent and later diagnosed with T-Cell Lymphoma or experienced other serious side effects, this could indicate a larger issue. Such serious implications are outlined in our analysis of Dupixent and its potential link to cancer. Furthermore, for those who have experienced blurry vision as a result of Saxenda usage, it is important to document these experiences thoroughly.

8) “PSLRA forward-looking + caution language + no duty to disclose = no omission claim”

What the defense will argue

- There is:

- no general duty to disclose all internal problems

- no duty to disclose mere trends unless required

- no duty to disclose uncharged wrongdoing

- Therefore omissions aren’t actionable.

Why courts sometimes accept it

- Plaintiffs sometimes argue that something was left out without connecting it to:

- a misleading affirmative statement

- a specific duty to disclose (such as trends in Management’s Discussion and Analysis, risk factors, or accounting rules)

How to counter it

- Frame omissions as half-truths: The cleanest omission claim is: “Once you spoke, you had to tell the whole truth.”

- Use MD&A / trend theory where supported: If there was a known trend/uncertainty reasonably likely to impact results, plead why it was known, why it was likely, and how it impacted operations.

What to include in the complaint

- A “duty map” for each omission:

- statement that triggered duty, or rule/reg requiring disclosure

- withheld fact

- why material

9) “It’s not material—no reasonable investor would care”

What the defense will argue

- The alleged misstatements were:

- too vague

- too small in magnitude

- offset by other disclosures

- Or the market didn’t care (no immediate price movement).

Why courts sometimes buy it

- Materiality is context-dependent and judges dislike speculative claims.

- If the statement is soft, courts may dismiss early.

How to counter it

- Prove materiality through market behavior and company emphasis

- Use:

- management focus (earnings scripts, investor days)

- analyst questions

- KPI prominence

- competitor benchmarking

- Use magnitude and sensitivity

- Show how the concealed fact affected:

- guidance feasibility

- margins

- unit economics

- regulatory ability to operate

- Don’t oversell

- Courts punish exaggerated “everything was fraudulent” narratives.

In cases like the Dupixent lawsuit, it’s crucial to present a clear picture of how the undisclosed information affected various aspects of the business. This includes demonstrating the impact on guidance feasibility, margins, and unit economics. These lawsuits often stem from allegations that companies failed to adequately warn about potential risks, such as in the case of Dupixent-related cancer lawsuits. Therefore, when navigating such complex legal landscapes, it’s essential not to oversell the narrative, as courts tend to respond negatively to exaggerated claims.

What to include in the complaint

- Materiality support:

- where the company repeated the point

- why investors tracked it

- how analysts modeled it

10) “No standing / no traceability / Section 11-style arguments bleeding into 10b”

What the defense will argue

- Plaintiffs can’t trace purchases to the challenged offering (more common in Section 11)

- Plaintiffs lack standing for certain securities or time periods

- Plaintiffs bought after corrective disclosures (no reliance/injury)

Why courts sometimes buy it

- Sloppy class period definitions and unclear purchase timing can create avoidable problems.

How to counter it

- Define the class period with discipline

- Anchor start: first actionable misstatement

- Anchor end: final corrective disclosure (or last inflation-maintaining statement before truth emerged)

- Use representative plaintiffs strategically

- Ensure the lead plaintiff(s) purchased during inflation and held through at least one corrective disclosure (when relevant)

- Clean transaction history

- Fix standing gaps before appointment battles escalate.

What to build into the record

- A simple timeline exhibit (internal to the team) mapping:

- statement dates

- purchase dates

- disclosure dates

- price reactions

11) “Class certification: individualized issues predominate (reliance, damages, etc.)”

What the defense will argue

The defense will present several arguments in response to the claims made by the plaintiffs:

Reliance isn’t common because:

- The market is not efficient

- The statements made were not public

- Any price impact caused by the statements has been rebutted

Damages are individualized due to:

- Different timing of purchases and sales

- Different investment strategies employed by each plaintiff

Additionally, the defense may also challenge the adequacy and typicality of the representative plaintiff.

Why courts sometimes buy it

- Weak market efficiency showing.

- Underdeveloped expert plan.

- Representative plaintiff issues.

How to counter it

Market efficiency: build a practical record

Typical evidence:

- high trading volume

- analyst coverage

- market makers/arbitrage

- eligibility for major indices

- narrow bid-ask spreads

- rapid incorporation of news

Anticipate price impact rebuttal

Be prepared to explain:

- why the event study window is appropriate

- why “no statistically significant reaction” isn’t dispositive in context

Damages: keep it formulaic

Securities class damages are typically handled with:

- common methodologies (inflation ribbon, event study)

Individual calculation doesn’t defeat predominance if methodology is common.

However, it’s important to note that various companies have faced class action lawsuits due to market inefficiencies or other related issues. For instance, the Perrigo Class Action Lawsuit seeks to represent purchasers or acquirers of Perrigo Company plc securities. Similarly, the WPP Class Action Lawsuit targets investors in WPP plc common stock, while the Stride Class Action Lawsuit focuses on Stride, Inc. securities. Moreover, the Freeport-McMoRan Class Action Lawsuit aims to represent purchasers of Freeport-McMoRan Inc. publicly traded securities. These examples illustrate the importance of understanding market dynamics and legal implications when navigating securities trading.

What to build into class cert

- A clear expert plan:

- what data is needed

- what event study will be tested

- how inflation and dissipation will be modeled

12) “Negative causation / alternative causation (your losses are from something else)”

What the defense will argue

- Losses were caused by:

- macroeconomic changes

- sector downturn

- competitor news

- interest rate changes

- commodity prices

- unrelated bad earnings

- Not by revelation of the alleged fraud.

Why courts sometimes buy it

- If the “corrective event” is noisy, courts may find causation too speculative.

How to counter it

1. Acknowledge and isolate

Treat alternative causation like a math problem:

- what else happened

- what portion of the move is attributable

2. Use peer/sector controls

Even at pleading stage, you can reference:

- sector ETF movement

- peer reactions

3. Focus on fraud-specific language in the disclosure

Courts care whether the market learned:

- something new

- something tied to the alleged misstatement

What to build into the complaint

On key disclosure dates, include:

- peer performance snapshots (even descriptive)

- analyst attribution quotes

- identification of fraud-specific revelations

13) “Section 20(a) fails because there’s no primary violation / no control / no culpable participation”

What the defense will argue

- If 10(b) fails, 20(a) fails.

- Even if 10(b) stands, plaintiffs did not plead control or culpable participation (where required).

How to counter it

- Treat 20(a) as more than boilerplate: Plead:

- reporting lines

- committee membership

- signature authority

- involvement in disclosures (earnings calls, filings, investor days)

- Use role-specific facts: CFO: accounting policies, controls, guidance, liquidity; CEO: strategic narratives, operational KPIs, investor communications

What to include in the complaint

For each person in control:

- Specify their actual authority and direct participation

- Avoid relying solely on their job title

When dealing with complex cases that involve multiple parties or jurisdictions, it may be beneficial to consider the Judicial Panel on Multidistrict Litigation. This panel transfers cases with common factual questions to a federal judge for coordinated proceedings, which can streamline the legal process significantly.

The “plaintiff-side” playbook that prevents most dismissal problems

If you want a simple structure that naturally counters most defense arguments, build your case around:

- A tight theory of the fraud

- one business problem

- one set of misleading statements

- one clear truth that was concealed

- A disclosure timeline that reads like cause-and-effect

- what the market believed

- what changed that belief

- what happened to the price

- Contemporaneous facts

- documents, metrics, witnesses, regulators, auditors, customers

- Selectivity

- fewer statements, stronger proof, clearer story

In cases involving pharmaceutical products like Zepbound, which has been linked to serious side effects such as eye floaters and vision problems, or Mounjaro which can cause blurry vision, it’s crucial to have a robust case. These medications have been associated with significant health issues when not properly disclosed. For instance, if a patient suffers from Zepbound vision problems after taking the medication as prescribed, it could lead to a strong claim against the prescribing entity. Similarly, if someone experiences Zepbound and other vision problems, it highlights the need for transparency in medical disclosures.

A practical checklist (use this before filing)

Use this as a pre-filing defense-argument audit:

- Falsity

- Do we explain why misleading at the time for each statement?

- Do we tie it to data, internal reporting, or real-world contradictions?

- Scienter

- Do we plead who knew what, when, and how?

- Do we confront innocent explanations?

- Safe harbor

- Did we separate present facts from projections?

- Do we plead “risk already materialized” where relevant?

- Loss causation

- Do we show what the market learned and why the drop matches that learning?

- Do we address confounders?

- Class cert

- Can we defend market efficiency and price impact with a coherent plan?

- Are the class rep’s trades clean and typical?

In situations where investors have suffered losses due to misleading statements or other malpractices, class action lawsuits can be an effective recourse. For instance, if you’ve incurred losses in Alexandria Real Estate, you might want to explore the Alexandria Real Estate Class Action Lawsuit. Similarly, if you’re a shareholder of Firefly Aerospace and facing similar issues, the Firefly Aerospace Class Action Lawsuit could provide you with necessary legal support.

Moreover, if you have invested in Primo Brands Corporation and are seeking justice for your losses, consider looking into the Primo Brands Class Action Lawsuit. Lastly, for those who have invested in Skye Bioscience and are dealing with potential losses due to misleading practices, there are ongoing Skye Bioscience Class Action Lawsuits that aim to represent affected shareholders.

Conclusion

Defense arguments in securities class actions don’t usually win because they’re brilliant. They win because they exploit gaps: vague falsity, thin scienter, noisy corrective disclosures, and undercooked price impact strategy.

If you build your complaint and litigation plan around:

- specific, contemporaneous contradictions

- a disciplined disclosure timeline

- a scienter mosaic grounded in reporting reality

- and a class certification record that anticipates price impact fights

…you’ll be countering the “common” arguments before they ever feel dangerous.

This approach is particularly relevant in the context of ongoing class action lawsuits like the MoonLake, Baxter, Freeport-McMoRan, and Skye Bioscience cases, where these strategies could significantly influence the outcome.