Introduction to How Securities Litigation is Vital for Investor Protection

Make no mistake, the securities litigation is absolutely vital for investor protection, transparency and market integrity. If you have ever wondered what actually protects everyday investors when a public company lies (or “massages” the truth), securities litigation is one of the biggest answers.

At a high level, securities litigation is the legal process investors use to hold companies, executives, auditors, and other market participants accountable when misleading statements, omissions, or fraudulent conduct distort the price of a stock or other security. And in practice, the workhorse of modern investor protection is the securities class action—a lawsuit brought on behalf of many investors who were harmed in the same way.

The key takeaway is simple: securities litigation, especially class actions, helps enforce honesty in the market. It creates real consequences for misconduct like accounting fraud, forces corrective information into the open, and helps recover losses when investors are harmed. In a world where markets run on trust, that combination is not optional—it’s essential.

However, securities litigation isn’t just limited to financial misconduct. It also extends to cases where certain products lead to unforeseen health issues, as seen in Mounjaro Vision Loss lawsuits. Such instances highlight the importance of having experienced legal representation to navigate these complex cases.

Moreover, investor rights are often at stake in real estate ventures, leading to situations like the Alexandria Real Estate Class Action Lawsuit for those who suffered losses in that sector.

Similarly, pharmaceutical companies can also face class action lawsuits due to adverse effects of their drugs, such as the ongoing Dupixent Cancer lawsuits which allege a potential link between Dupixent and cancer development.

In another instance, there are ongoing legal proceedings like the MoonLake class action lawsuit, which seeks to represent purchasers who have faced issues with MoonLake Immunotherapeutics.

These examples underscore how securities litigation plays a crucial role not just in maintaining market integrity but also in safeguarding investor rights and holding corporations accountable for their actions.

Understanding Securities Litigation and Class Actions

What securities litigation is (and why it matters)

Securities litigation refers to lawsuits involving the purchase or sale of securities—stocks, bonds, options, and similar financial instruments—where investors allege they were misled or harmed by unlawful conduct. For a deeper understanding of this complex field, you might want to explore the fundamentals of securities litigation, which covers the basics such as the different stages of the litigation and the key players involved.

That unlawful conduct can include:

- Misrepresenting revenue, profits, or key operating metrics

- Hiding major risks (like liquidity problems, regulatory investigations, or customer concentration)

- Insider trading or misleading disclosures around mergers, projections, or guidance

- Market manipulation and other deceptive practices

The reason this matters goes beyond any one company. Securities laws are designed to promote fair, orderly, and efficient markets. But laws on paper don’t enforce themselves. Regulators like the Securities and Exchange Commission (SEC) can (and do) bring enforcement actions, but they have limited resources and must prioritize. Securities litigation helps fill that gap by enabling investors to act when they have been harmed.

In other words, securities litigation helps maintain market integrity because it reinforces the core promise of public markets: that investors are making decisions based on reasonably accurate, complete information.

In some instances, such as with certain pharmaceutical products like Zepbound, these legal issues can also intersect with health concerns. If individuals experience adverse effects like vision problems after using such products, they might consider pursuing a Zepbound vision loss lawsuit to seek justice for their suffering.

Individual lawsuits vs. class actions (and why class actions are so common)

Investors can sue individually, but in many securities fraud situations, individual lawsuits are impractical.

Here’s why:

- Losses are often widespread but uneven. One investor may lose $2,000, another may lose $200,000—but the misconduct is the same.

- Litigation is expensive. Expert witnesses, forensic accounting, discovery, and motion practice can cost millions.

- Information is asymmetrical. Companies and executives control most of the relevant documents and internal context.

That’s where class actions come in.

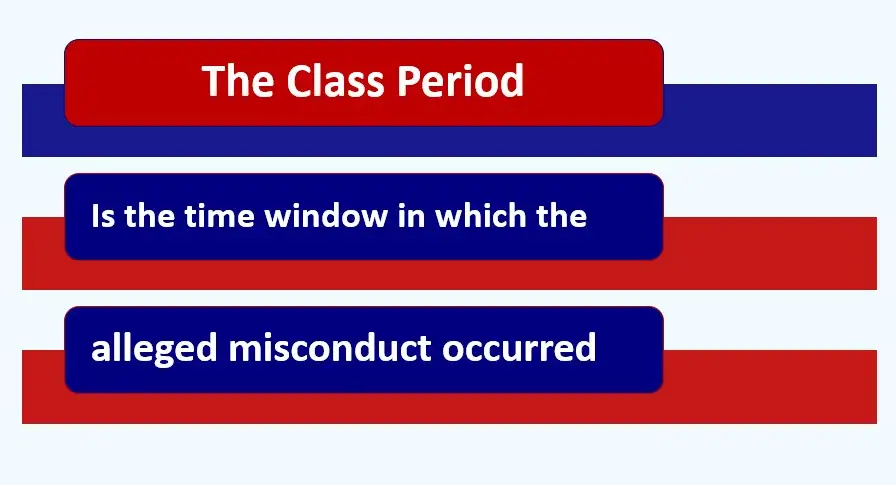

A securities class action aggregates the claims of many investors who purchased the security during a defined “class period” (the period when alleged misinformation inflated the price). A representative plaintiff (often a large institutional investor) acts on behalf of the class, and if the case succeeds or settles, recovery is distributed according to an approved plan. For instance, recent Firefly Aerospace class action lawsuit illustrates this process well.

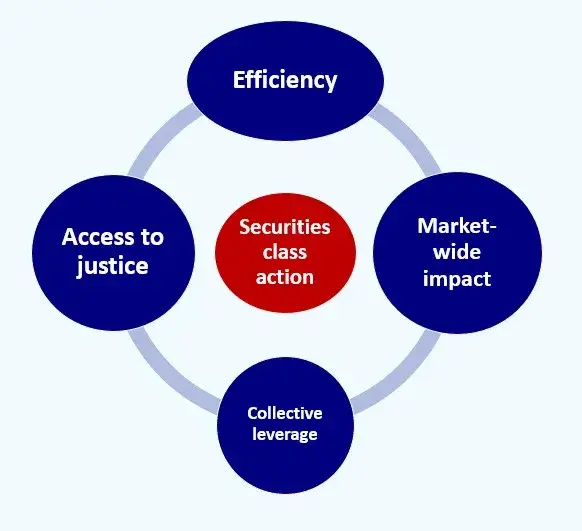

Class actions have several practical advantages:

- Efficiency: One case resolves many similar claims, avoiding hundreds or thousands of duplicative lawsuits.

- Access to justice: Investors with smaller losses can participate in recovery that would be impossible to pursue individually.

- Collective leverage: The class can fund the experts and discovery needed to challenge sophisticated corporate defendants.

- Market-wide impact: A successful case can change behavior across an industry, not just in one company. An example being the Baxter Class Action Lawsuit which sought to represent purchasers or acquirers of Baxter International, Inc.

In short: class actions are often the only realistic mechanism for large-scale investor recovery and accountability. If you are considering pursuing a class action lawsuit, firms like The Law Offices of Timothy L. Miles practice in such cases and can provide valuable assistance.

Common grounds for securities litigation: accounting fraud and scienter

Most major securities class actions involve two recurring themes: accounting fraud and scienter.

1) Accounting fraud (manipulating financial statements)

Accounting fraud is not just “bad accounting” or making an honest mistake. It refers to manipulating financial reporting to present a false picture of a company’s performance or financial condition.

Common patterns include:

- Recognizing revenue too early (booking sales before they are earned)

- Inflating receivables or hiding uncollectible accounts

- Understating expenses (capitalizing costs that should be expensed)

- Improper reserves (releasing reserves to boost earnings)

- Channel stuffing (shipping excess inventory to distributors to book revenue)

- Round-trip transactions (artificial sales that lack real economic substance)

Why it’s so damaging: financial statements are the “language” of public markets. If that language is deliberately distorted, investors can’t price risk properly—and capital gets allocated based on fiction.

A simple illustration: imagine a company reports “record profitability,” but later it turns out those profits depended on aggressive revenue recognition and undisclosed customer returns. Investors who bought based on the reported numbers paid an inflated price. When the truth emerges, the stock can drop sharply, wiping out market value in days.

One notable instance of this is the Perrigo class action lawsuit, where shareholders alleged that false and misleading statements artificially inflated the stock price until the truth was revealed.

2) Scienter (intent to deceive)

In many securities fraud cases (particularly those brought under Rule 10b-5 in the U.S.), plaintiffs must plausibly allege scienter, meaning an intent to deceive, manipulate, or defraud (or, depending on the jurisdiction and claim, a sufficiently reckless disregard for the truth).

Scienter matters because it draws the line between:

- legitimate business optimism that turned out wrong, and

- fraud dressed up as confidence

Proving intent is rarely straightforward. Companies do not usually write emails saying, “Let’s lie to investors.” Instead, scienter is often inferred from circumstantial evidence such as:

- internal reports contradicting public statements

- executive stock sales timed before bad news

- auditor warnings or restatement red flags

- whistleblower allegations

- sudden resignations of key finance leaders

- patterns of repeated, specific false statements on core metrics

This highlights the crucial role of whistleblowers, who often provide key evidence in these cases. Their insider knowledge can expose fraudulent practices that would otherwise remain hidden. This is one reason securities litigation is both challenging and important: it forces the legal system to scrutinize what companies knew, when they knew it, and whether investors were intentionally misled.

The Role of Corrective Disclosures and Deterrent Effects in Investor Protection

In the realm of investor protection, corrective disclosures play a crucial role. These disclosures serve to rectify misleading information that may have influenced an investor’s decision. For instance, if a pharmaceutical company fails to disclose the debilitating vision side effects of Trulicity, it can lead to significant financial losses for investors who were unaware of the potential risks associated with the drug.

Similarly, the lack of transparency regarding the worst vision side effects of Zepbound can also have detrimental effects not only on patients but also on investors. Therefore, it’s imperative for companies to provide accurate and comprehensive information about their products to safeguard investor interests.

Deterrent effects come into play when these corrective disclosures are made. They serve as a warning to other companies about the potential consequences of misleading their investors. This not only helps in maintaining transparency but also fosters a sense of accountability among corporations, ultimately leading to better investor protection.

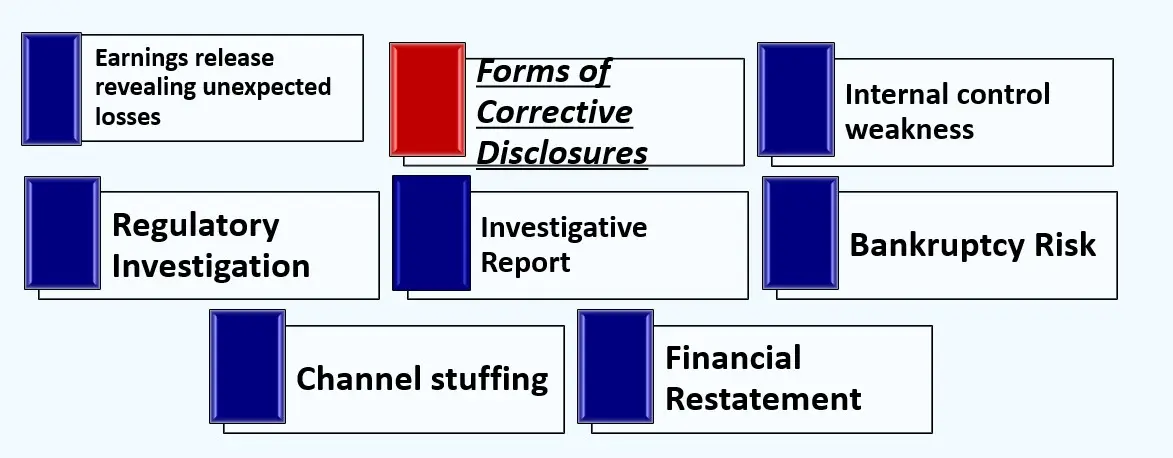

Corrective disclosures: how the truth reaches the market

A key concept in securities class actions is the corrective disclosure—a public revelation that corrects prior misleading statements or exposes previously concealed information.

Corrective disclosures can take many forms:

- an earnings release revealing unexpected losses

- a financial restatement

- a public admission of internal control weaknesses

- a regulatory investigation announcement

- a credible investigative report that triggers company confirmation

- a major customer termination disclosure

- bankruptcy risk disclosures that contradict prior “strong liquidity” claims

Why this matters for investor protection:

- They reduce information asymmetry. Investors can’t react to risks they don’t know exist.

- They support price correction. When material truth enters the market, the stock price can adjust to reflect reality.

- They create a public record. Litigation often uncovers facts that make future concealment harder.

In many cases, the corrective disclosure is what finally forces accountability. It’s the moment where the gap between “story” and “reality” becomes impossible to ignore.

From a market perspective, corrective disclosures are painful—but necessary. They help restore accurate pricing and prevent ongoing harm to new investors who might otherwise buy at an artificially inflated price.

FORMS OF CORRECTIVE DISCLOSURES

The deterrent effect: why the threat of liability changes behavior

Securities class actions don’t just compensate investors after a fraud. They also create a deterrent effect—a pressure system that influences corporate behavior before misconduct happens.

When executives and boards know that misleading disclosures can lead to:

- massive discovery obligations

- reputational damage

- executive time drain

- insurance impacts (D&O insurance)

- personal liability in certain circumstances

- large settlements or judgments

…they have stronger incentives to:

- invest in compliance and internal controls

- take disclosure obligations seriously

- avoid aggressive accounting “games”

- correct issues earlier rather than later

- document decisions more carefully

Deterrence works best when it’s credible. If fraud is low-risk and high-reward, some actors will take the gamble. Securities litigation raises the cost of gambling with investor trust.

And importantly, deterrence protects more than the plaintiffs in any one case. It protects the next investors, in the next company, in the next reporting cycle—because it shapes what corporate leadership teams view as “safe” or “worth it.”

This principle of deterrence is not limited to financial misconduct alone. For instance, recent research has highlighted potential eye issues linked to certain medications like Zepbound, which while effective in lowering blood sugar, have been associated with serious side effects such as eye floaters. This serves as a reminder that transparency and accountability should extend beyond financial disclosures to include all aspects of corporate responsibility, including those related to product safety and health implications.

The Importance of Strong Corporate Governance and Internal Controls in Preventing Securities Violations

It’s easy to talk about litigation as the solution, but the deeper goal is preventing the underlying misconduct in the first place. That’s where corporate governance and internal controls come in.

Corporate governance: oversight that actually functions

Corporate governance is the system of rules, practices, and oversight structures that guide how a company is run. In public markets, corporate governance is one of the strongest predictors of whether bad news gets surfaced early—or buried until it becomes catastrophic.

Key governance mechanisms that reduce securities fraud risk include:

- Independent board oversight: Directors who can challenge management, not rubber-stamp it.

- Strong audit committees: Financially literate members who ask hard questions and demand clear answers.

- Ethical leadership and tone at the top: When leadership rewards “hitting numbers at any cost,” fraud risk spikes.

- Whistleblower protections: Systems that allow employees to report issues without retaliation.

- Transparent disclosure culture: A habit of reporting risks, not just marketing the upside.

When governance fails, it often fails in predictable ways:

- boards rely too heavily on management narratives

- audit committees meet but do not investigate deeply

- internal warnings get ignored until external pressure forces action

- executives treat disclosure as PR rather than a legal duty

Securities litigation often shines a harsh light on governance failures—board minutes, committee oversight, known red flags—because those documents and decisions become relevant to the question of what the company knew and how it responded.

A notable example of how poor corporate governance can lead to severe consequences is seen in the case of certain pharmaceutical companies. For instance, Mounjaro, a medication that has been linked to serious side effects like blurry vision due to potential negligence in reporting these risks.

Internal controls: the first line of defense against manipulation

Internal controls are the processes designed to ensure financial reporting is accurate, transactions are properly authorized, and risks are monitored.

Effective controls help prevent:

- improper revenue recognition

- fictitious or unsupported journal entries

- off-book arrangements

- weak segregation of duties (where one person can both create and approve transactions)

- inadequate review of estimates (reserves, impairments, valuation assumptions)

Controls matter because a lot of accounting fraud isn’t cinematic. It can be incremental: small manipulations that compound quarter after quarter. Weak controls give those manipulations room to grow.

And when companies disclose “material weaknesses” in internal controls—especially after years of strong-sounding statements—investors often react sharply. Those disclosures can also become central in securities litigation because they raise questions like:

- Were prior statements about financial health misleading?

- Did leadership know controls were failing earlier?

- Were the company’s certifications and risk disclosures accurate?

Healthy governance and strong controls reduce the likelihood of fraud. But when they don’t exist—or when they’re treated as a compliance checkbox—securities litigation becomes a critical backstop for accountability.

Class Action Settlements: Restoring Trust Through Financial Recovery and Transparency

Most securities class actions end in settlement rather than trial. And while settlements are sometimes criticized as “just paying to make it go away,” they play a major role in investor protection when designed and supervised properly.

For instance, the Baxter class action lawsuit, which seeks to represent purchasers or acquirers of Baxter International, Inc. common stock, is a prime example of how these settlements can provide financial recovery for affected investors.

Similarly, the Freeport-McMoRan class action lawsuit aims to represent those who have purchased or acquired publicly traded securities of Freeport-McMoRan Inc., further illustrating the protective role of such legal actions.

In another instance, the Primo Brands class action lawsuit seeks to protect the rights of shareholders who have invested in Primo Brands Corporation, demonstrating that these settlements can also serve to uphold shareholder rights.

Lastly, the Skye Bioscience class action lawsuit represents yet another case where a class action settlement is being pursued for the benefit of investors. Each of these cases underscores the importance of properly managed class action settlements in restoring trust and providing financial recovery for investors.

Financial recovery: making harmed investors whole (at least partially)

When a stock drops after a corrective disclosure, investors who purchased at inflated prices can suffer real losses. A settlement can’t always restore everything—markets are complex, and losses may involve other factors—but it can:

- compensate investors for a portion of inflation-related losses

- return value to pension funds and retirement accounts

- signal that misconduct has consequences

This is not abstract. Many class members are ordinary investors indirectly—through mutual funds, index funds, 401(k)s, and pension plans. Securities fraud isn’t just a “Wall Street problem.” It can directly hit retirement security.

Trust restoration: the market needs closure

Beyond money, settlements can help restore trust by creating a structured resolution that includes:

- court oversight

- documented allegations and defenses

- transparency around the nature of claimed misconduct

- reforms in some cases (though not always)

Even when a company does not admit wrongdoing (common in many settlements), the process itself still matters because it forces disclosure, imposes financial consequences, and provides a public record for investors and future governance.

Why transparency and integrity in settlements matter

Settlement fairness is a real issue. Because class actions resolve claims for large groups, the process needs checks to ensure outcomes aren’t skewed by information imbalances.

Key principles that support fairness include:

- Clear notice to class members explaining rights and options

- Court review of settlement terms to evaluate adequacy and reasonableness

- Transparent attorney fee processes subject to judicial approval

- Fair allocation plans that reflect how damages are calculated

- Claims administration integrity so eligible investors can actually recover

When settlement negotiations and approvals are handled with seriousness, settlements can do what they’re meant to do: compensate investors, reinforce truthful disclosure norms, and reduce the chance that similar misconduct repeats.

The Evolving Landscape of Securities Class Actions: Regulatory Changes and Global Trends

Securities litigation isn’t static. It evolves with markets, regulation, and investor behavior.

Regulatory updates and shifting pleading/disclosure expectations

In many jurisdictions, changes in pleading standards, disclosure rules, and enforcement priorities can influence:

- how hard it is for plaintiffs to survive early motions to dismiss

- what must be disclosed by public companies (risk factors, forward-looking statements, internal controls)

- the types of cases that are viable (and how they’re framed)

For investors, these changes matter because they shape whether litigation can function as an effective accountability tool. When pleading standards become stricter, weaker cases may be filtered out—but there’s also a risk that meritorious cases become harder to bring without early access to evidence that is controlled by defendants.

At the same time, disclosure expectations tend to grow over time. Markets demand more clarity about risk, and regulators often respond to new crises with new rules. That pushes public companies toward more robust compliance—at least in theory. Litigation pressure often helps ensure those expectations are taken seriously in practice.

A case in point is the Trulicity and Macular Edema situation. Trulicity, a GLP-1 medication, has been associated with an increased risk of macular edema when combined with insulin. This scenario underscores the importance of stringent disclosure rules and compliance, particularly when it comes to disclosing potential risks associated with medications.

Global trends: more recognition of group proceedings

Historically, U.S.-style securities class actions were more common in the United States than elsewhere. But globally, there’s increasing recognition that group proceedings (collective actions, representative actions, or class-like structures) can improve investor protection.

Internationally, the trend is driven by a few realities:

- public companies raise capital across borders

- investors are global (pension funds, sovereign wealth funds, asset managers)

- misconduct in one market can harm investors worldwide

- regulators alone may not provide full recovery pathways

As more jurisdictions adopt or expand collective redress mechanisms, investor protection becomes less dependent on any one country’s system—and companies face growing expectations that truthful disclosure is not optional anywhere they list or raise capital.

ESG Factors as Emerging Drivers of Securities Litigation: A Call for Responsible Corporate Behavior

One of the most important shifts in securities litigation over the last few years is the growing relevance of ESG—environmental, social, and governance factors.

The basic idea is not that companies must be perfect. It’s that when companies make material ESG-related statements to investors—about emissions, workplace safety, supply chain practices, data privacy, product safety, or governance—and those statements are misleading, investors may claim they were deceived in a way that affected valuation.

Why ESG claims increasingly show up in securities class actions

ESG factors now influence:

- institutional investment decisions and proxy voting

- risk modeling (regulatory, reputational, operational)

- consumer trust and revenue durability

- access to capital and insurance costs

That means ESG statements can move markets—especially when they relate to core business risks.

Examples of ESG-linked litigation themes include:

- Environmental: misleading claims about sustainability practices, emissions exposure, or compliance with environmental regulations

- Social: failure to disclose systemic workplace misconduct, safety failures, discriminatory practices, or supply chain labor risks

- Governance: misleading statements about compliance culture, board oversight, or risk management processes

In many cases, the alleged fraud theory is familiar: investors claim the company painted a reassuring picture (“best-in-class compliance,” “strong safety culture,” “industry-leading sustainability”) while internal facts suggested the opposite. When a scandal, regulatory action, disaster, or investigative report reveals the truth, the stock drops, and litigation follows.

Such scenarios are not limited to traditional sectors. For instance, in the Firefly Aerospace class action lawsuit, investors raised concerns over misleading ESG claims that led to significant financial losses.

Moreover, the healthcare sector has also seen its share of ESG-related litigation. Patients using drugs like Wegovy and Trulicity have reported serious side effects such as vision loss and blindness respectively. These adverse outcomes not only raise ethical questions about corporate governance but also lead to potential lawsuits against the manufacturers for failing to disclose critical safety information related to their products.

![Settlements in Securities Litigation: A Step-By-Step Guide to the Settlement Process [2025] used in Settlements in Securities Litigation](https://classactionlawyertn.com/wp-content/uploads/2025/10/ezgif-6a5f7ee5dbefe0.webp)

The real investor-protection point: “non-financial” doesn’t mean “immaterial”

A decade ago, some companies treated ESG as branding. Today, ESG-related issues can represent:

- direct financial risk (fines, lawsuits, shutdowns)

- operational risk (supply disruptions, labor shortages)

- valuation risk (cost of capital, index exclusion, customer churn)

Securities litigation is one mechanism pushing companies to align public ESG messaging with verifiable reality. Not because courts are setting climate policy or workplace policy—but because markets require truthful, non-misleading disclosure when statements are used to attract investment and support valuation.

Conclusion

Investor protection isn’t just about punishing bad actors after the fact. It’s about maintaining a market where trust is deserved—because accuracy is enforced.

Securities litigation, especially through class actions, is vital because it:

- holds companies accountable when disclosures mislead investors

- forces corrective information into public view

- deters fraud by raising the cost of deception

- provides a pathway for financial recovery

- reinforces governance and internal control expectations

- adapts to new risk areas like ESG and globalized capital markets

But litigation alone is not enough. A robust investor-protection ecosystem also requires proactive regulation, vigilant enforcement, strong corporate governance, and informed investor activism. When those pieces work together, securities litigation becomes what it’s meant to be: not a nuisance, not a headline generator—but a necessary pillar of fair, transparent, functioning public markets

Contact Timothy L. Miles Today for a Free Case Evaluation About Securities Class Action Lawsuits