Introduction to the Pleading Standards in Securities Litigation

Securities litigation has some of the toughest pleading rules in U.S. civil law. As we move into 2026, the landscape remains shaped by the same reality: if you cannot plead it with particularity, you do not get discovery—and your case likely ends before it starts. That is the resounding effect of the Private Securities Litigation Reform Act of 1995 (PSLRA).

This guide breaks down the pleading standards that actually decide most cases at the motion-to-dismiss stage, especially under:

- Rule 9(b) (fraud must be pleaded with particularity),

- the PSLRA (Private Securities Litigation Reform Act), and

- modern Supreme Court and circuit case law (including Tellabs, Dura, Omnicare, and Halliburton).

I’ll keep this practical and complaint-drafting focused—because that’s where these standards matter.

In a related note, recent reports have emerged about potential side effects from certain medications like Wegovy, Zepbound, and Mounjaro, which include serious vision-related complications such as blindness or blurry vision. If you or someone you know has suffered from these side effects after using these medications, it may be worth consulting with a lawyer who specializes in such cases, like a Wegovy Blindness Lawyer or someone knowledgeable about Zepbound and eye floaters.

Why pleading standards matter more in securities litigation than almost anywhere else

In most civil cases, a plaintiff can plead generally, get into discovery, and refine the theory later.

In federal securities fraud cases, Congress did the opposite.

The PSLRA was built to front-load specificity requirements so that plaintiffs must show they have a serious claim before they gain access to discovery (which is expensive, intrusive, and can pressure settlements even in weak cases).

So the motion to dismiss is not a speed bump—it’s often the main event.

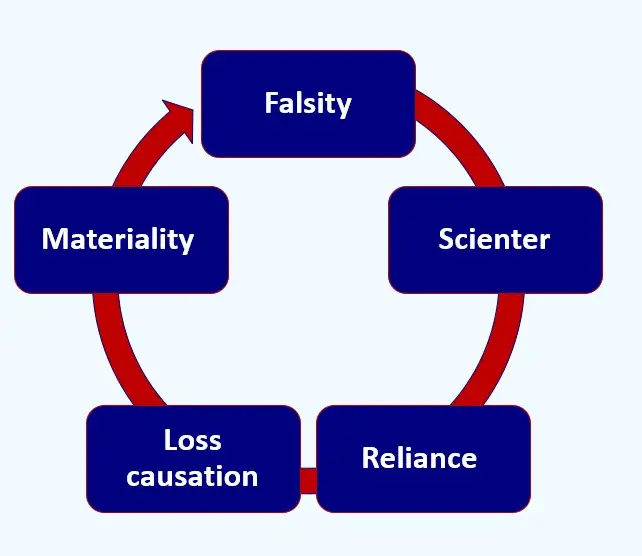

The core pleading framework (the “stack” you must satisfy)

A typical Section 10(b)/Rule 10b-5 securities fraud complaint must plead:

- A material misstatement or omission

- Scienter (intent to deceive, manipulate, or defraud, or severe recklessness in most circuits)

- Connection with the purchase or sale of a security

- Reliance (often via fraud-on-the-market in class actions)

- Economic loss

- Loss causation (the misstatement caused the loss)

At the pleading stage, the big killers are usually:

- Falsity (what exactly was false, and why),

- Scienter (a strong inference), and

- Loss causation (a plausible causal link between truth and drop).

Case Studies: Vision Loss from Medications

In recent years, certain medications have been linked to severe side effects, including vision loss. For instance, if you’re dealing with potential lawsuits related to Mounjaro and its associated vision loss, it’s essential to have a skilled attorney who specializes in such cases.

Similarly, Trulicity has been reported to cause debilitating vision side effects for some users. If you or a loved one has experienced such issues, understanding your legal options is crucial.

Moreover, there have also been reports about Zepbound causing severe vision-related side effects. Such information is vital for individuals considering legal action against these pharmaceutical companies.

Class Action Lawsuits

In instances of widespread harm caused by a company’s product, class action lawsuits can be an effective legal strategy. For example, the Baxter Class Action Lawsuit seeks to represent purchasers of Baxter International’s common stock who may have suffered due to misleading statements made by the company.

Similarly, the Firefly Aerospace Class Action Lawsuit aims to represent investors who have faced losses due to alleged fraudulent activities within the company.

These cases underscore the importance of establishing a clear connection between the misstatement and the resulting economic loss as outlined in our core pleading framework.

The “baseline” standard: Rule 8 and Twombly/Iqbal

Even before you hit Rule 9(b) and the PSLRA, every federal complaint must satisfy Rule 8(a) and the plausibility standard from:

- Bell Atl. Corp. v. Twombly

- Ashcroft v. Iqbal

That means you need more than labels and conclusions. Courts disregard legal conclusions and ask whether the facts plausibly support the elements.

But in securities fraud, Rule 8 is just the floor.

Rule 9(b): pleading fraud “with particularity”

The basic requirement

Federal Rule of Civil Procedure 9(b) requires that fraud be pleaded with particularity—typically described as the “who, what, when, where, and how” of the misconduct.

In securities class actions, courts often look for:

- Who made the statement (speaker identity)

- What was said (exact statement or close paraphrase)

- When it was said (date/time frame)

- Where it appeared (10-K, earnings call, press release, investor deck)

- Why/How it was false or misleading at the time

A practical way to draft this section

For each challenged statement, plaintiffs should usually include:

- Quote (or precise description)

- Date and source

- Speaker

- Why misleading at that time

- Supporting facts (documents, witnesses, metrics, admissions, later restatement, etc.)

Common failure: complaints that rely on hindsight (“the company later missed targets, therefore earlier optimism was false”) without contemporaneous facts.

PRE- AND POST-PSLRA STANDARDS FOR SECURITIES FRAUD LITIGATION

| Feature | Pre-PSLRA Standard | Post-PSLRA Standard |

| Motion to dismiss | Based on “notice pleading” (Federal Rule of Civil Procedure 8(a)), making it easier for plaintiffs to survive motions to dismiss. This often led to settlements to avoid costly litigation. | Requires satisfying PSLRA’s heightened pleading standards and the “plausibility” standard from Twombly and Iqbal. Failure to plead with particularity on any element can result in dismissal. |

| Pleading | “Notice pleading” was generally sufficient, though fraud claims under Federal Rule of Civil Procedure 9(b) required particularity for the circumstances of fraud, but intent could be alleged generally. | Each misleading statement must be stated with particularity, explaining why it was misleading. Facts supporting beliefs in claims based on “information and belief” must also be stated with particularity. |

| Scienter | Pleaded broadly; the “motive and opportunity” test was often sufficient to infer intent. | Requires alleging facts creating a “strong inference” of fraudulent intent, which must be at least as compelling as any opposing inference of non-fraudulent intent, as clarified in Tellabs, Inc. v. Makor Issues & Rights, Ltd.. |

| Loss causation | Not a significant pleading hurdle, often assumed if a plaintiff bought at an inflated price. | Requires pleading facts showing the fraud caused the economic loss, often by linking a corrective disclosure to a stock price drop. Dura Pharmaceuticals, Inc. v. Broudo affirmed this. |

| Discovery | Could proceed while a motion to dismiss was pending. | Automatically stayed during a motion to dismiss. |

| Safe harbor for forward-looking statements | No statutory protection. | Protects certain forward-looking statements if accompanied by “meaningful cautionary statements”. |

| Lead plaintiff selection | Often the first investor to file. | Court selects based on a “rebuttable presumption” that the investor with the largest financial interest is the most adequate. |

| Liability standard | For non-knowing violations, liability was joint and several. | For non-knowing violations, liability is proportionate; joint and several liability applies only if a jury finds knowing violation. |

| Mandatory sanctions | Available under Federal Rule of Civil Procedure 11, but judges were often reluctant to impose them. | Requires judges to review for abusive conduct |

The PSLRA: the real gatekeeper

The PSLRA adds two major pleading burdens on top of Rule 9(b):

- Particularity of falsity (what was misleading and why), and

- Strong inference of scienter for each act/statement.

It also imposes an automatic stay of discovery during the pendency of a motion to dismiss (with limited exceptions).

These stringent requirements can significantly impact investors, especially in cases like the Alexandria Real Estate Class Action Lawsuit, where losses have been incurred due to misleading statements or actions.

PSLRA falsity: “specify each statement” and explain “why” it’s misleading

The statutory idea (in plain English)

You must:

- identify each statement alleged to be misleading, and

- state with particularity the facts on which that belief is formed.

This is where complaints often sink if they:

- lump statements together (“Defendants made false statements throughout the class period”),

- fail to identify the precise contradictory facts, or

- plead “fraud by hindsight.”

For instance, in the Perrigo class action lawsuit, the complaint alleges that the defendant made false and misleading statements which artificially inflated the stock price until the truth was revealed. Similarly, the Primo Brands class action lawsuit seeks to represent those who purchased or acquired shares of Primo Brands Corporation under similar circumstances.

What “why misleading” really means

Courts generally want to see one of these:

- The statement contradicted internal facts known at the time

- The statement omitted a fact that made it misleading in context

- The statement was framed as fact but lacked a reasonable basis

- The company said “X is true,” while documents/metrics show “not-X”

But courts also recognize that not every omission is actionable. Which brings us to one of the most misunderstood topics in pleading.

Omissions and half-truths: the Omnicare mindset

Even though Omnicare, Inc. v. Laborers District Council arose in a Section 11 context, its reasoning heavily influences how courts analyze opinions and omissions across securities cases.

Key practical takeaways:

- A statement of opinion is not actionable just because it turned out wrong.

- It can be actionable if:

- the speaker didn’t actually believe it, or

- it omitted facts that made the opinion misleading to a reasonable investor, or

- it implied a basis that didn’t exist (e.g., “we believe reserves are adequate” while ignoring known contrary analyses)

When pleading omissions, plaintiffs need to identify:

- the duty to disclose (why the company had to say more), and

- why the omission made what was actually said misleading.

Forward-looking statements and the PSLRA safe harbor

A lot of securities complaints target guidance, projections, and “we expect…” statements.

But the PSLRA has a safe harbor for forward-looking statements if:

- they are identified as forward-looking and accompanied by meaningful cautionary language, or

- plaintiffs fail to plead actual knowledge of falsity (for certain forward-looking statements)

Pleading tip

If you’re challenging forecasts/guidance, courts often want:

- contemporaneous facts showing the forecast lacked a reasonable basis, and/or

- specific facts showing defendants knew the projection was unattainable when stated.

Common failure: complaining about a missed forecast without pleading internal data, pipeline deterioration, cancellations, inventory build, margin compression, regulatory blocks, etc., that existed when the forecast was made.

Puffery, corporate optimism, and why courts dismiss “vibes”

Courts regularly dismiss claims based on:

- vague optimism (“we’re well-positioned,” “strong demand,” “world-class team”),

- generalized ethical statements (“we value integrity,” “we comply with all laws”),

- aspirational ESG language with no concrete misrepresentation

This is often called puffery—immaterial statements that no reasonable investor relies on as hard fact.

The line that matters (in practice)

Optimism becomes actionable when it is:

- tied to specific facts (“our backlog increased 25%”),

- presented as verifiable reality, or

- made misleading by omission of known contradictory facts (“demand is strong” while the company is seeing mass cancellations)

Scienter: the PSLRA “strong inference” requirement (the hardest part)

The standard from Tellabs

Under Tellabs, Inc. v. Makor Issues & Rights, courts must consider whether the alleged facts give rise to an inference of scienter that is:

cogent and at least as compelling as any opposing innocent inference.

So you don’t just plead a plausible inference of intent—you plead one that can compete with non-fraud explanations.

This standard can be particularly relevant in cases involving serious allegations, such as those related to medical issues caused by pharmaceutical products. For instance, the Zepbound eye issues have been linked to GLP-1 receptor agonists, which raises significant concerns about the responsibility of pharmaceutical companies in ensuring the safety of their products. In such scenarios, proving intent or knowledge of potential harm becomes crucial and may require meeting the stringent standards set by the Tellabs decision.

What facts typically support scienter (at pleading stage)

Courts commonly find scienter more plausible when complaints allege:

- motive + opportunity (less persuasive alone in many circuits)

- suspicious insider trading (ttiming, amount, deviation from plan/history)

- internal reports or metrics contradicting public statements

- admissions (post-class period statements, whistleblower accounts, restatements)

- “core operations” allegations (varies by circuit; stronger with specific internal facts)

- accounting violations plus red flags (more than GAAP error alone)

- contemporaneous emails, meeting notes, or internal forecasts

What usually fails

- “They must have known” because the issue was important

- generalized motives (wanting to keep stock price high, wanting bonuses)

- negligence or poor management dressed up as fraud

Confidential witnesses (CWs): still useful, but only if done right

Many complaints rely on former employees. Courts scrutinize CW allegations for:

- job title and responsibilities

- basis of knowledge

- time period of employment

- proximity to the events

- corroboration across multiple sources

Drafting tip: treat each CW like a mini affidavit—without actually calling it that. Vague CWs (“a former employee said…”) are easy to attack.

Group pleading and attribution: who said what?

A recurring pleading problem is attribution.

- For Exchange Act/Rule 10b-5, plaintiffs usually must connect statements to specific defendants.

- Some circuits are skeptical of broad “group pleading” (attributing all corporate statements to senior leadership) post-PSLRA.

- For control person claims (Section 20(a)), plaintiffs must plead:

- a primary violation, and

- control (and sometimes culpable participation, depending on circuit law)

Practical implication: if you’re suing individuals, you need a clean map of which exec signed, spoke, reviewed, approved, or controlled the challenged disclosures.

Loss causation: Dura and what courts actually want

The rule from Dura Pharmaceuticals v. Broudo

It’s not enough to plead that you bought at an inflated price.

You must plead that the revelation of the truth (or materialization of the concealed risk) caused an economic loss.

Common acceptable pleading theories

- Corrective disclosure: a disclosure revealed the truth, stock drops

- Materialization of the risk: the concealed risk event occurs, stock drops, and the event is tied to the alleged fraud

- Partial disclosures / leak-out: truth emerges over time through a series of disclosures

What courts often reject

- a price drop tied to broader market decline with no link to corrective truth

- “the stock dropped after bad news” without connecting the bad news to the alleged misstatements

- pleading loss causation with conclusory language (“as the truth was revealed…”)

Drafting tip: include an event timeline:

- statement → inflation theory

- disclosure (or risk event) → why it revealed/corrected/matched the concealed truth

- price reaction → loss tie-in

Even without expert-level event study details, plead a coherent causal narrative.

In some cases, such as with certain medications like Trulicity or Zepbound, patients have experienced severe side effects, including vision loss or Zepbound related vision problems. If these issues arise, it’s crucial to connect the adverse effects and subsequent financial implications to the misstatements made by the companies. This forms part of the coherent causal narrative that can be pleaded in court.

Circuit Court Standards for Pleading Loss Causation in Securities Fraud Actions

| Circuit | Summary of pleading standard | Key cases | Notes and circuit splits |

| First Circuit | Applies a relatively lenient standard under Rule 8(a), requiring only plausible allegations that connect the corrective disclosure to the preceding misrepresentation. | Massachusetts Retirement Systems v. CVS Caremark Corp. (2013). | Stands with circuits requiring only “plausible” allegations rather than particularity. |

| Second Circuit | Requires plaintiffs to allege that the subject of the fraudulent statement was the cause of the actual loss suffered. Does not require particularized pleading. | Lentell v. Merrill Lynch & Co. (2005); Emergent Capital Inv. Mgmt., LLC v. Stonepath Grp., Inc. (2003). | Focuses on “zone of risk” analysis and requires that the misstatement concerns the very facts that caused the loss. |

| Third Circuit | Follows a moderate approach under Rule 8(a), requiring a causal connection between the misrepresentation and the loss that is more than merely possible or speculative. | McCabe v. Ernst & Young, LLP (2007); EP Medsystems, Inc. v. EchoCath, Inc. (2000). | Requires plaintiffs to demonstrate that the revelation of fraudulent information was a “substantial factor” in causing the decline in stock value. |

| Fourth Circuit | Applies the heightened Rule 9(b) pleading standard to loss causation, requiring plaintiffs to plead with particularity how the corrective disclosure relates to the prior misrepresentation. | Katyle v. Penn National Gaming, Inc. (2011); Teachers’ Ret. Sys. of LA v. Hunter (2007). | Stands with the Seventh and Ninth Circuits in requiring particularized pleading of loss causation. |

| Fifth Circuit | Requires that plaintiffs allege both that the corrective disclosure specifically revealed the fraud and that the revelation of the fraud caused the loss. | Pub. Emps. Ret. Sys. of Miss. v. Amedisys, Inc. (2014); Lormand v. US Unwired, Inc. (2009). | Particularly stringent about the connection between corrective disclosure and prior misrepresentation. |

| Sixth Circuit | Follows a moderate approach, requiring plaintiffs to demonstrate a causal connection between the misrepresentation and the loss, but not requiring the heightened particularity of Rule 9(b). | Ohio Pub. Emps. Ret. Sys. v. Federal Home Loan Mortgage Corp. (2016); IBEW Local 58 v. Royal Bank of Scotland (2013). | Focuses on whether the disclosure revealed “some aspect” of the prior misrepresentation. |

| Seventh Circuit | Applies the heightened Rule 9(b) pleading standard to all elements of securities fraud, including loss causation. | Tricontinental Industries v. PricewaterhouseCoopers (2007); Ray v. Citigroup Global Markets (2007). | Stands with the Fourth and Ninth Circuits in requiring particularized pleading of loss causation. |

| Eighth Circuit | Applies a relatively lenient standard, requiring only that the complaint provide the defendant with notice of the plaintiff’s claim that the misrepresentation caused the loss. | In re Cerner Corp. Sec. Litig. (2005); Schaaf v. Residential Funding Corp. (2008). | Tends to analyze loss causation under the more permissive Rule 8(a) standard. |

| Ninth Circuit | Applies the heightened Rule 9(b) pleading standard to all elements of securities fraud, including loss causation. | Oregon Public Employees Retirement Fund v. Apollo Group Inc. (2014); Metzler Inv. GMBH v. Corinthian Colleges, Inc. (2008). | Previously inconsistent but firmly established Rule 9(b) standard in Oregon Public Employees v. Apollo (2014). |

| Tenth Circuit | Applies a moderate approach that requires a logical link between the misrepresentation and the economic loss, but does not explicitly require Rule 9(b) particularity. | In re Williams Sec. Litig. (2007); Nakkhumpun v. Taylor (2015). | Focuses on whether the disclosure revealed “some aspect” of the prior misrepresentation. |

| Eleventh Circuit | Requires plaintiffs to plead that the misrepresentation was the “substantial or significant contributing factor” in the loss, but generally follows Rule 8(a). | Hubbard v. BankAtlantic Bancorp, Inc. (2012); FindWhat Investor Group v. FindWhat.com (2011). | Emphasizes proximate causation principles in loss causation analysis. |

| D.C. Circuit | Has limited securities fraud jurisprudence but generally follows a more lenient approach aligned with Rule 8(a). | Plumbers & Steamfitters Local 773 Pension Fund v. Danske Bank (2020). | Generally follows the Supreme Court’s guidance in Dura Pharmaceuticals without imposing heightened pleading requirements. |

Reliance: fraud-on-the-market and class action realities

Reliance is often presumed in class actions through the fraud-on-the-market doctrine (Basic v. Levinson), if the security traded in an efficient market.

At the pleading stage, plaintiffs typically allege:

- the security traded on a national exchange,

- high volume/analyst coverage/market makers, etc.

Defendants may later try to rebut price impact (Halliburton II), often at class certification—not necessarily on a motion to dismiss.

For instance, in the context of Firefly Aerospace Class Action Lawsuit, plaintiffs are seeking to represent purchasers or acquirers of Firefly Aerospace Inc., indicating reliance on the fraud-on-the-market doctrine. Similarly, the Baxter Class Action Lawsuit also exemplifies how this doctrine is applied in real-world scenarios.

It’s important to consult with experienced legal professionals when navigating these complex issues. The Law Offices of Timothy L. Miles specialize in securities class actions and mass torts, providing top-rated legal assistance in such matters.

Materiality: usually not decided on a motion to dismiss (but sometimes is)

Materiality is often a fact question. Courts may dismiss on materiality grounds where the statements are:

- puffery,

- obviously immaterial,

- too generic to move a reasonable investor

But if the statement is specific and tied to financial performance, risk, compliance, or a key product, courts are more likely to let materiality proceed.

Section 11 and Section 12(a)(2): different pleading posture (often easier than 10b-5)

Not all securities cases are Rule 10b-5 fraud cases.

Section 11 (Securities Act)

- Focuses on material misstatements/omissions in a registration statement

- Does not always require scienter, reliance, or loss causation (varies by posture and defenses)

- But if the claim “sounds in fraud,” Rule 9(b) may apply

Section 12(a)(2)

- Similar, but tied to prospectuses/oral communications in public offerings

Practical drafting issue: plaintiffs sometimes plead Section 11 claims with heavy “fraud” language, triggering Rule 9(b) scrutiny unnecessarily.

The “bespeaks caution” doctrine and risk factors (what courts do with them)

Even outside the PSLRA safe harbor, courts consider whether robust risk disclosures neutralize alleged misstatements.

But risk factors don’t protect you if:

- the risk had already materialized and the company spoke as if it hadn’t, or

- the company presented a known problem as hypothetical (“we may face supply constraints” while already in severe shortage)

So the question is often timing: Was it truly a risk, or was it already happening?

For instance, in the case of the Dupixent lawsuit, plaintiffs argue that Sanofi and Regeneron failed to adequately warn about risks associated with their medication. This highlights how a company’s failure to disclose materialized risks can lead to legal repercussions.

Similarly, with Trulicity, there are claims regarding its association with severe health issues like Macular Edema. If such risks were known but not disclosed adequately, it could also result in significant legal challenges for the manufacturers.

A practical complaint blueprint (what a court expects to see)

If you’re drafting—or evaluating—a securities complaint, this structure tends to align with what courts look for:

- Executive summary (one page): theory of the fraud, the concealment, and the corrective event

- Parties: roles, titles, signature authority, speaking roles

- Regulatory + business context: what matters operationally

- The misstatements: a table-like section with each statement, date, source, speaker, and why false

- The contemporaneous contradictory facts: internal metrics, CWs, reports, red flags

- Scienter allegations: individualized, tied to facts (not just importance)

- Loss causation: timeline of disclosures/risk events and price drops

- Class allegations (if applicable): For instance, in the case of the Skye Bioscience Class Action Lawsuit, which seeks to represent purchasers or acquirers of Skye Bioscience, Inc.

- Counts: 10b-5, Section 20(a), Section 11/12 where applicable

What defendants attack first (so you should preempt it)

Defense motions to dismiss usually focus on:

- no actionable misstatement (puffery/opinion/safe harbor)

- no contemporaneous falsity (hindsight pleading)

- no strong inference of scienter (Tellabs)

- no loss causation (Dura)

- PSLRA particularity failures (lumping, vague CWs, missing dates/sources)

If you read enough dismissal opinions, you’ll notice courts reward complaints that behave like they already anticipate the motion.

A recent example of a case that faced such challenges is the MoonLake class action lawsuit. This lawsuit, captioned Peters v. MoonLake Immunotherapeutics, No. 25-cv-08612 (S.D.N.Y.), seeks to represent purchasers or holders of MoonLake securities who suffered losses due to alleged misstatements and omissions by the company.

2025 reality check: what’s trending in pleading fights

A few themes continue to show up in recent pleading battles. One notable trend is the emergence of Dupixent cancer lawsuits, which have been fueled by recent scientific investigations raising concerns about a potential link between Dupixent and cancer development.

1) Courts demand tighter linkage between internal facts and external statements

It’s not enough to say “internal data existed.” You need to plead what it showed and how it contradicts the specific public claim.

2) Risk disclosures are heavily litigated

Especially in product failures, cybersecurity incidents, regulatory investigations, and liquidity crises—where companies sometimes describe current problems as hypotheticals.

3) Scienter is increasingly litigated statement-by-statement

Courts frequently reject “collective scienter” theories unless the pleading ties knowledge to the individuals who made or approved the challenged statements.

4) Loss causation pleadings are more narrative-driven (and courts are skeptical of vague “truth emerged” language)

Complaints that cleanly identify corrective disclosures (or materialization events) and explain the “truth” link tend to survive more often.

Common examples (and how pleading standards apply)

Example A: Revenue recognition + later restatement

What can work:

- Identify the exact revenue line items impacted

- Plead internal warnings, auditor disputes, control failures, or invoice timing issues

- Tie executives to knowledge (certifications, meetings, internal dashboards)

- Use the restatement as part of falsity support (but not as scienter by itself)

What often fails:

- “There was a restatement, therefore fraud”

- No facts showing what management knew when

Example B: Product demand misstatements

What can work:

- Channel checks, cancellation rates, inventory build, ASP declines

- CWs describing weekly sales reports contradicting upbeat demand claims

- Sudden guidance cut tied to previously concealed demand softness

What often fails:

- alleging demand was “weak” with no contemporaneous metrics

Example C: Cybersecurity incident disclosures

What can work:

- Plead what the company said about security posture or incident status

- Show it knew of breaches, intrusions, or vulnerabilities earlier

- Frame as half-truths (“no evidence of exfiltration” while evidence existed)

What often fails:

- treating generic security risk language as a misstatement without a concrete contradictory fact pattern

Quick cheat sheet: pleading standards by element (10b-5)

- Falsity: specify each statement + why misleading + contemporaneous facts

- Scienter: strong inference, at least as compelling as innocent inference (Tellabs)

- Reliance: usually presumed in class actions (fraud-on-the-market)

- Loss causation: tie truth/risk revelation to loss (Dura)

- Materiality: avoid puffery; plead why a reasonable investor would care

Let’s wrap up

Securities cases don’t usually die because the underlying story is impossible. They die because the complaint can’t clear the pleading standards—especially under Rule 9(b) and the PSLRA.

If you want to remember just one thing in 2025, it’s this:

A viable securities complaint reads less like a suspicion and more like a sourced, statement-by-statement reconstruction of what was said, what was known, and how the market learned the truth.

That means:

- quote the statements,

- plead the contemporaneous contradictory facts,

- tie knowledge to the right people,

- and connect the disclosure to the loss.

Do that, and you’ll be arguing the merits. Don’t, and you’ll be arguing whether you’re allowed to proceed at all.

Contact Timothy L. Miles Today for a Free Case Evaluation About Securities Class Action Lawsuits