Introduction to a A Magisterial Elucidation on Securities Litigation

Securities litigation occupies a crucial yet uncomfortable space in today’s capital markets.

On one side, no prudent investor desires a market where every earnings miss leads to securities litigation. Conversely, it is equally problematic for markets to function when issuers can raise capital through half-truths, obscure risks in footnotes, or inflate financial results long enough for insiders to cash out.

This inherent tension is precisely why securities litigation exists: to deter fraudulent activities, partially compensate harmed investors, and reinforce the disclosure-based bargain that forms the foundation of U.S. securities regulation.

This comprehensive 2025 guide dives deep into the complex arena of securities litigation, covering essential federal statutes that govern it, legal concepts that drive real cases, the ongoing impact of the Private Securities Litigation Reform Act (PSLRA), and strategic choices faced by investors and counsel today.

For instance, in recent years we have seen significant instances like the Alexandria Real Estate Class Action Lawsuit, where investors suffered losses due to misleading information. Such cases underline the importance of securities litigation in holding issuers accountable.

Similarly, there are emerging concerns linking certain medications to severe side effects, as seen in the case of Zepbound and its documented side effect of causing eye floaters. This highlights another facet of securities litigation – protecting investor rights in sectors beyond traditional finance.

Moreover, recent scientific investigations have raised alarms about a potential connection between Dupixent and cancer development. This situation exemplifies how securities litigation can serve as a vital tool for investors seeking justice and accountability from corporations that misrepresent their products or financial health.

The Role of Securities Litigation in Protecting Investors

The Role of Securities Litigation in Protecting Investors

Securities litigation broadly refers to civil lawsuits arising from alleged violations of securities laws—most commonly, claims that investors bought or sold securities based on materially false or misleading information (or unlawful omissions), market manipulation, or other deceptive conduct.

Why it matters (beyond the headline settlements)

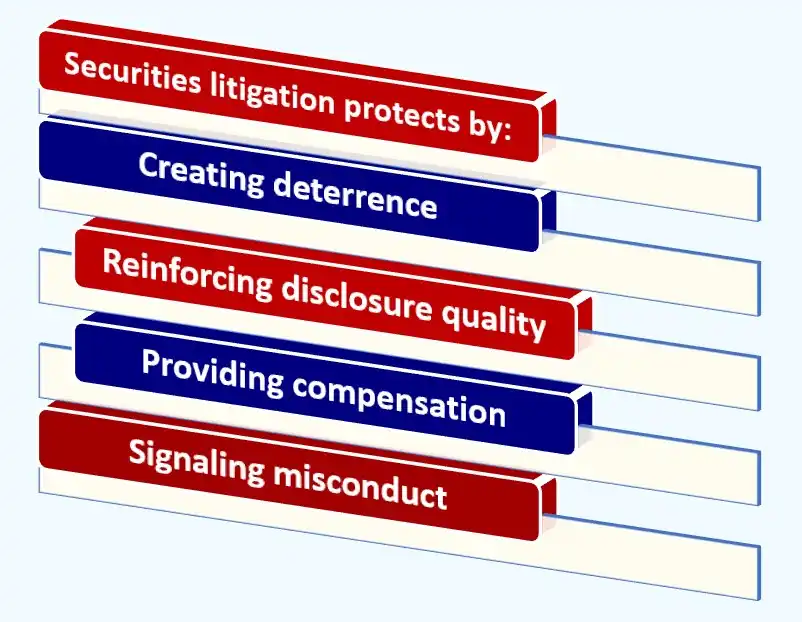

At a practical level, securities litigation helps protect investors by:

- Creating deterrence: Companies, executives, underwriters, auditors, and other gatekeepers face real exposure if disclosures are materially wrong.

- Reinforcing disclosure quality: The U.S. securities system relies heavily on accurate, complete, timely information. Litigation is one mechanism (alongside SEC enforcement) that pressures issuers to comply.

- Providing compensation: Recoveries rarely make investors “whole,” but they can meaningfully offset losses—especially for institutions managing retirement or public funds.

- Signaling misconduct: Litigation can uncover facts (through investigations, whistleblowers, and discovery where available) that the market didn’t have at the time of the fraud.

Different forms of securities litigation (and why class actions dominate)

Securities litigation comes in several forms, including:

- Securities class actions (often the most visible): Typically brought on behalf of purchasers during a defined “class period,” alleging inflation of the security price due to misstatements/omissions and losses when the truth emerges. For instance, the recent Firefly Aerospace class action lawsuit seeks to represent purchasers or acquirers of Firefly Aerospace Inc., illustrating how these lawsuits function in real-world scenarios.

- Individual investor actions: More common where losses are large enough to justify independent litigation (or where the investor’s reliance story is unique).

- Derivative suits: Brought on behalf of the corporation against officers/directors for breach of fiduciary duty (often parallel to securities class actions, but legally distinct).

- M&A litigation with securities components: Claims tied to proxy disclosures, tender offers, or deal-related statements.

- State law claims with securities overlap: For example, certain common law fraud claims, though many are preempted or constrained by federal law depending on structure.

Securities class actions remain a prevalent mechanism because they aggregate many investors’ claims that would be impractical to litigate individually, and because public-company fraud often affects thousands of investors simultaneously through the market price. A prime example is the Baxter Class Action Lawsuit, which seeks to represent purchasers or acquirers of Baxter International, Inc. common stock.

The Law Offices of Timothy L. Miles, a top-rated class action and mass torts law firm, practices handling such securities class actions and mass torts, helping to ensure that affected investors have their voices heard and their claims addressed.

Why legal framework literacy matters—for everyone

Understanding securities litigation is not just for plaintiffs’ lawyers. It matters for:

- Investors deciding whether to seek lead-plaintiff status, opt out, or file individually.

- Public companies and boards managing disclosure controls, risk factors, and crisis responses.

- Underwriters, auditors, and advisors evaluating diligence processes and liability exposure.

- Insurers pricing D&O risk and structuring coverage.

- Compliance and finance teams living with the reality that a disclosure mistake can become a legal theory.

In 2025, the story is less about whether securities litigation exists, and more about how it works under modern pleading standards, evolving case law, and increasingly complex financial reporting.

Key Federal Statutes Regulating Securities Litigation

Two federal statutes form the backbone of most U.S. securities litigation:

- The Securities Act of 1933 (the “Securities Act”)

- The Securities Exchange Act of 1934 (the “Exchange Act”)

They overlap in purpose—protecting investors through disclosure and anti-fraud rules—but differ sharply in when they apply and what plaintiffs must prove.

Securities Act vs. Exchange Act (scope and posture)

At a high level:

- The Securities Act of 1933 primarily governs offerings—especially initial public offerings (IPOs) and other public issuances—focusing on the accuracy of registration statements and prospectuses at the time securities are sold.

- The Exchange Act of 1934 primarily governs secondary market trading and ongoing reporting for public companies, and includes the most litigated anti-fraud provision in modern practice: Section 10(b) and SEC Rule 10b-5.

A simplified way to think about it:

- The 1933 Act is about truth in selling securities (particularly at issuance).

- The 1934 Act is about truth in trading and reporting over time (and policing manipulation and deception in the market).

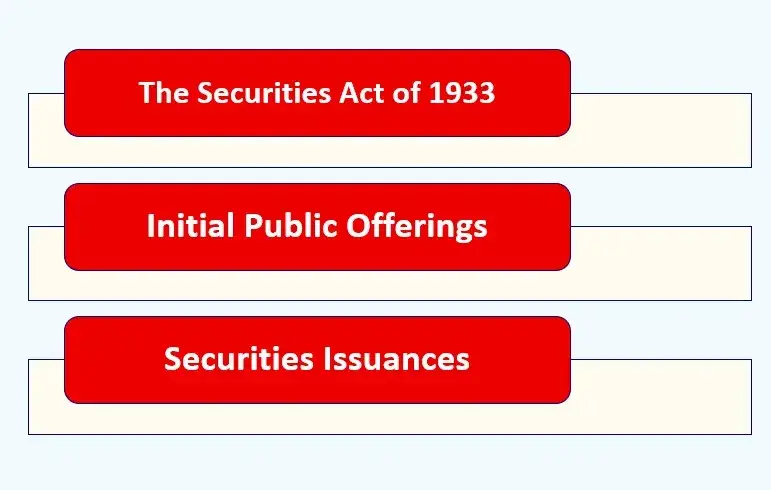

The Securities Act of 1933: Governing Initial Public Offerings and Securities Issuances

The Securities Act of 1933: Governing Initial Public Offerings and Securities Issuances

The Securities Act was designed around a simple idea: if you’re going to raise money from the public, you must provide full and fair disclosure. In an IPO or registered offering, that disclosure is largely packaged into the registration statement (and its prospectus).

When that document is materially wrong, the Securities Act provides plaintiffs with powerful causes of action—most notably Section 11 and Section 12.

Section 11: Civil liability for false registration statements (and why it’s so feared)

Section 11 imposes liability for material misstatements or omissions in a registration statement.

What makes Section 11 distinctive—and, from a defense perspective, dangerous—is that it is often described as a near-strict-liability statute for the issuer:

- Issuer liability: The issuer is typically liable if the registration statement was materially misleading—without plaintiffs needing to prove intent (scienter) and often without proving individual reliance.

- Other defendants: Underwriters, directors, certain officers, and experts (e.g., auditors for portions they “expertise”) may also be liable, though they often can assert due diligence or reasonable investigation defenses not available to the issuer in the same way.

In plain English: if the registration statement contained a material lie (or hid a material fact), Section 11 can be an efficient route to recovery.

Why materiality matters: Not every error triggers liability. The misstatement or omission must be material—i.e., there must be a substantial likelihood a reasonable investor would view it as having significantly altered the “total mix” of information.

An example of how a material misstatement could occur is seen in the case of Mounjaro, where patients have reported experiencing blurry vision as a side effect. If such serious side effects were not disclosed in a registration statement related to Mounjaro, it could potentially lead to a Section 11 claim due to the materiality of the omitted information.

Why investors like Section 11 claims: They can be comparatively less burdensome than Exchange Act fraud claims because the fight often centers on what the document said, what was omitted, and whether it mattered—rather than what executives secretly believed.

Section 12: Liability tied to the offer or sale—unregistered offerings and false prospectuses

Section 12 (commonly discussed as Section 12(a)(1) and 12(a)(2)) targets misconduct in the offer or sale process.

Two core theories often appear:

- Offering unregistered securities: Section 12 can impose liability for selling securities in violation of registration requirements (subject to exemptions and complex transactional structures). For instance, the ongoing Freeport-McMoRan class action lawsuit, which seeks to represent purchasers of Freeport-McMoRan Inc.’s publicly traded securities, is a prime example of this.

- False statements in prospectuses or oral communications: Section 12(a)(2) is frequently invoked when offering materials contain material misstatements or omissions. A recent instance highlighting this issue is the Skye Bioscience class action lawsuit, where the class action lawsuit represents purchasers or acquirers of Skye Bioscience, Inc. securities due to misleading information provided during the offering.

Where Section 11 targets the registration statement, Section 12 is often framed around selling and solicitation conduct and the communications used to market the offering.

The practical takeaway for 1933 Act claims

In modern practice, Securities Act claims often arise after:

- An IPO followed by a price drop and revelations that key risks were understated (demand, churn, regulatory exposure, customer concentration, margin sustainability, etc.).

- A follow-on offering where the market later learns of adverse facts that arguably should have been disclosed in offering documents.

- A SPAC-era transaction structure (still relevant in 2025 as courts work through standards), where offering-like disclosure obligations are litigated under evolving theories depending on the instrument and filings.

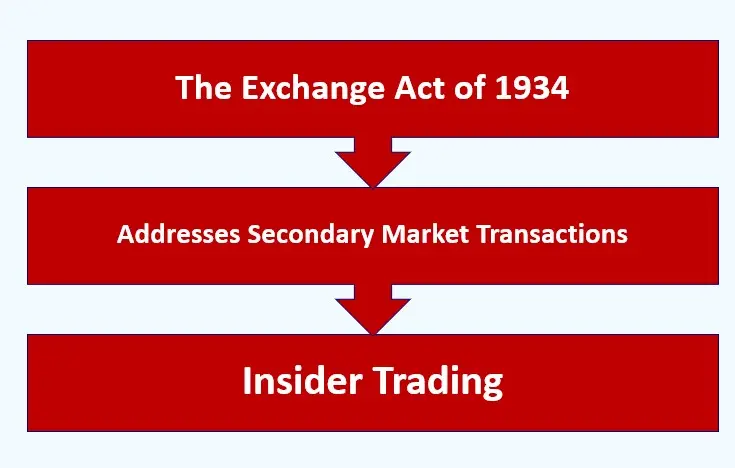

The Exchange Act of 1934: Addressing Secondary Market Transactions and Insider Trading

The Exchange Act regulates the public-company lifecycle after going public: periodic reporting, disclosures, and market integrity. It is also the statute most associated with secondary market fraud—the classic “company said X, truth was Y, stock dropped” case.

Ongoing reporting obligations and the disclosure ecosystem

Public companies must file periodic reports (e.g., annual and quarterly reports) and furnish certain current reports. These filings, plus earnings calls, press releases, investor presentations, and other communications, create an ongoing disclosure record.

When that record is alleged to be false or misleading, plaintiffs typically look to Section 10(b) and Rule 10b-5.

Section 10(b) and Rule 10b-5: The workhorse anti-fraud claim (with a higher burden)

Section 10(b) prohibits manipulative and deceptive practices in connection with the purchase or sale of securities. Rule 10b-5 operationalizes that prohibition, and together they cover a wide range of alleged misconduct, including:

- Misstatements or omissions about revenue, margins, growth, guidance, backlog, or risk exposure

- Misleading statements about product readiness, regulatory compliance, cybersecurity posture, or internal controls

- Market manipulation schemes

- Insider trading (often in parallel with SEC enforcement; private actions exist but are complex and fact-dependent)

However, compared with Sections 11 and 12, Section 10(b) claims typically impose a higher burden on plaintiffs. A central reason is scienter.

Plaintiffs generally must plead and ultimately prove that defendants acted with the required wrongful mental state—often described as intent to deceive or deliberate recklessness, depending on jurisdictional standards.

That scienter requirement is one reason Exchange Act cases often turn on internal documents, witness accounts, restatements, unusual insider sales, and evidence that executives “knew or must have known” their public statements were misleading.

Understanding Key Legal Concepts in Securities Litigation Claims

Securities cases are won and lost on a handful of recurring concepts. Two matter especially across modern dockets: scienter and accounting/iinternal control failures.

Scienter: the mental state at the center of fraud litigation

In the securities context, scienter refers to the defendant’s mental state—roughly, whether they acted with fraudulent intent or reckless disregard for the truth.

Why it matters:

- Under Section 10(b), scienter is typically a required element.

- Under Sections 11 and 12, scienter is often not required in the same way (which is a major reason plaintiffs prefer those theories when available).

In real cases, scienter is rarely established by a single “smoking gun.” Instead, courts often evaluate whether the pleaded facts collectively support a strong inference that defendants acted with the requisite state of mind.

Common scienter allegations include:

- Executives had access to contradictory internal reports

- The misstatement concerned the company’s “core operations”

- The company engaged in suspicious accounting practices

- There were significant insider stock sales timed before a corrective disclosure

- Whistleblower allegations or regulator inquiries were ignored or concealed

- Statements were inconsistent with contemporaneous metrics (e.g., churn, returns, delinquency, usage)

A relevant case that underscores these issues is the Dupixent lawsuit, where numerous lawsuits have been filed against Sanofi and Regeneron. These lawsuits allege that the companies failed to adequately warn patients about potential side effects of Dupixent, highlighting how a lack of transparency can lead to significant legal repercussions.

Accounting fraud and internal controls: frequent engines of litigation

Many securities class action lawsuits—especially large ones—are built on alleged accounting fraud or serious deficiencies in internal controls over financial reporting. These issues trigger litigation so often due to the following reasons:

- Accounting is where narrative meets numbers; when numbers are wrong, the market impact tends to be immediate and measurable.

- Restatements, auditor resignations, material weaknesses, or delayed filings can function as powerful “corrective disclosures.”

- Internal control failures can support an inference that executives were at least reckless in certifying financial statements, depending on the facts.

Recurring accounting-related themes include:

- Revenue recognition disputes (timing, collectability, channel stuffing)

- Understated reserves (returns, chargebacks, warranty, credit losses)

- Capitalization versus expense manipulation

- Inventory accounting distortions

- Related-party transactions not properly disclosed

- Non-GAAP metrics portrayed in misleading ways

- Weak controls that allow aggressive accounting to persist

In 2025, cases also increasingly involve complex operational data—platform metrics, engagement numbers, cohort retention, AI-driven product claims, cybersecurity risk representations—that function like “financial reporting” in the eyes of investors even when not strictly GAAP.

In such scenarios, whistleblowers often play a crucial role in uncovering fraudulent activities. The significance of protecting these individuals cannot be overstated and has become a key aspect of whistleblower law in Nashville and beyond.

Furthermore, it’s essential to note that the repercussions of certain corporate practices extend beyond financial misreporting. For instance, recent research has established a concerning association between certain pharmaceutical treatments and Zepbound eye issues, highlighting the need for transparency and accountability in all corporate disclosures.

Impactful Reforms: The Private Securities Litigation Reform Act (PSLRA) and Its Effect on Securities Class Actions

The Private Securities Litigation Reform Act of 1995 (PSLRA) reshaped the landscape of securities class actions. Enacted amid concerns—fairly or not—that these lawsuits were too easily filed after stock drops and were being used to extract settlements disconnected from actual fraud, the PSLRA aimed to address these issues.

Whether one views the PSLRA as a necessary correction or an overcorrection, the practical reality is simple: it made securities fraud class actions harder to plead and prosecute. This reform has significantly impacted the fundamentals of securities litigation, making it more challenging for plaintiffs to successfully navigate through the different stages of litigation.

However, despite these challenges, some class action lawsuits have emerged as notable examples in recent years. For instance, the MoonLake class action lawsuit seeks to represent purchasers or acquirers of MoonLake Immunotherapeutics, reflecting the ongoing relevance of class actions in today’s financial landscape.

Similarly, the Baxter class action lawsuit represents another significant case, aiming to represent purchasers or acquirers of Baxter International, Inc. common stock. This lawsuit underscores the complexities and challenges that have arisen post-PSLRA.

In another instance, the Perrigo class action lawsuit alleges that false and misleading statements by the defendant drove the stock price artificially up until the truth emerged. Such cases highlight how the PSLRA has not entirely deterred legitimate claims of securities fraud.

Lastly, it’s worth noting that even companies in emerging sectors like space technology are not immune from such legal challenges. The Firefly Aerospace class action lawsuit serves as an instructive guide for investors navigating this complex landscape.

The PSLRA’s core move: raise the pleading bar

One of the most significant PSLRA reforms is its heightened pleading standard, especially for scienter-based claims.

For many Exchange Act claims, plaintiffs must plead facts giving rise to a strong inference of scienter. This standard forces plaintiffs to do more than allege motive and opportunity or to rely on generalized accusations.

In practice, this has driven:

- Heavier reliance on confidential witnesses (former employees, consultants)

- Intensive pre-filing investigation of industry conditions, competitors, customers, and supply chain indicators

- Greater focus on restatements, internal control admissions, and regulator actions

- More sophisticated event studies and loss causation theories (though those are typically proven later)

PRE- AND POST-PSLRA STANDARDS FOR SECURITIES FRAUD LITIGATION

| Feature | Pre-PSLRA Standard | Post-PSLRA Standard |

| Motion to dismiss | Based on “notice pleading” (Federal Rule of Civil Procedure 8(a)), making it easier for plaintiffs to survive motions to dismiss. This often led to settlements to avoid costly litigation. | Requires satisfying PSLRA’s heightened pleading standards and the “plausibility” standard from Twombly and Iqbal. Failure to plead with particularity on any element can result in dismissal. |

| Pleading | “Notice pleading” was generally sufficient, though fraud claims under Federal Rule of Civil Procedure 9(b) required particularity for the circumstances of fraud, but intent could be alleged generally. | Each misleading statement must be stated with particularity, explaining why it was misleading. Facts supporting beliefs in claims based on “information and belief” must also be stated with particularity. |

| Scienter | Pleaded broadly; the “motive and opportunity” test was often sufficient to infer intent. | Requires alleging facts creating a “strong inference” of fraudulent intent, which must be at least as compelling as any opposing inference of non-fraudulent intent, as clarified in Tellabs, Inc. v. Makor Issues & Rights, Ltd.. |

| Loss causation | Not a significant pleading hurdle, often assumed if a plaintiff bought at an inflated price. | Requires pleading facts showing the fraud caused the economic loss, often by linking a corrective disclosure to a stock price drop. Dura Pharmaceuticals, Inc. v. Broudo affirmed this. |

| Discovery | Could proceed while a motion to dismiss was pending. | Automatically stayed during a motion to dismiss. |

| Safe harbor for forward-looking statements | No statutory protection. | Protects certain forward-looking statements if accompanied by “meaningful cautionary statements”. |

| Lead plaintiff selection | Often the first investor to file. | Court selects based on a “rebuttable presumption” that the investor with the largest financial interest is the most adequate. |

| Liability standard | For non-knowing violations, liability was joint and several. | For non-knowing violations, liability is proportionate; joint and several liability applies only if a jury finds knowing violation. |

| Mandatory sanctions | Available under Federal Rule of Civil Procedure 11, but judges were often reluctant to impose them. | Requires judges to review for abusive conduct |

Other PSLRA features that shaped modern cases

While the heightened scienter pleading standard gets the most attention, the PSLRA also influenced the ecosystem by:

- Encouraging institutional investors to seek lead plaintiff roles (to reduce lawyer-driven suits)

- Creating structured processes for appointing lead counsel

- Staying certain discovery during motions to dismiss in many cases (limiting plaintiffs’ ability to “fish” for documents before surviving dismissal)

The combined effect: by 2025, strong securities class actions are often built like investigative projects long before the complaint is filed. This trend is particularly evident in cases involving pharmaceutical products, where patients have suffered severe side effects. For instance, there has been a rise in lawsuits where patients seek representation from a Wegovy Blindness Lawyer due to vision-related complications linked to Wegovy use.

Similarly, another notable area of concern is the vision-related complications associated with Trulicity, leading patients to seek help from a Trulicity Vision Loss Lawyer. These emerging trends highlight the evolving landscape of securities class actions and their connection to patient safety issues in the pharmaceutical industry.

Navigating Challenges: Strategic Considerations for Investors Pursuing Securities Class Actions Today

For investors considering action—especially institutions weighing whether to move for lead plaintiff—strategy starts with a deceptively basic question:

Which legal theory is actually available, and which one gives you the best path through a motion to dismiss?

Understanding the available legal theories is crucial. For instance, in the case of the Primo Brands class action lawsuit, it seeks to represent purchasers or acquirers of Primo Brands Corporation (NYSE: PRMB). This highlights the importance of identifying the right legal strategy that aligns with the specific circumstances of the case at hand.

Choosing between Sections 11/12 and Section 10(b)

The choice often depends on when the alleged misstatements occurred and where they appeared.

- If the alleged misconduct is tied to an IPO or registered offering, Section 11 and/or Section 12 may be available and attractive because they often reduce the need to prove scienter and reliance.

- If the alleged misconduct involves ongoing public statements, periodic reports, earnings calls, and market trading, Section 10(b) is typically the primary vehicle—but it comes with higher pleading burdens, especially around scienter.

Investors and counsel often evaluate:

- Proof burden: Do you need to plead scienter? How hard will that be without discovery?

- Defendant set: Are underwriters or directors potentially in the case (common in Section 11) versus primarily the issuer and executives (common in 10(b))?

- Timing and class period: Was the harm concentrated around an offering window or spread across quarters of reporting?

- Damages theory: How will inflation and corrective disclosures be modeled? Are there multiple partial disclosures?

Importantly, many real-world disputes involve both 1933 Act and 1934 Act claims—especially where an offering is followed by ongoing allegedly misleading reporting.

In some cases, like those involving certain pharmaceuticals such as Trulicity, which may lead to serious health issues like Macular Edema when misrepresented, these legal complexities can become even more pronounced.

The non-negotiable: serious pre-filing investigation

Because pleading standards are demanding and dismissal risk is real, credible securities cases generally require meaningful pre-filing work, such as:

- Mapping the disclosure timeline: what was said, when, and in what forum (filings vs calls vs presentations)

- Identifying the truth plaintiffs claim was concealed, and how/when it emerged (restatement, investigative report, regulator action, earnings miss, leaked customer data, etc.)

- Testing materiality: would a reasonable investor care, and is there a coherent theory of why the statement moved price?

- Building a scienter narrative (for 10(b)): what facts support intent or recklessness—internal contradictions, resignations, insider sales, contemporaneous warnings

- Assessing loss causation: connecting the alleged fraud to the economic loss, not merely to a general market decline

- Vetting standing and traceability for offering claims (especially relevant for Section 11 in modern trading environments)

For investors, this is also the stage where you decide whether participation should be passive (as a class member) or active (as a lead plaintiff or opt-out claimant with individualized strategy). If you are considering an active role due to potential vision-related side effects from medications like Mounjaro or Trulicity which may necessitate legal action due to vision loss or other debilitating conditions that can arise from such medications as outlined in our article on the debilitating vision side effects of Trulicity or Zepbound, it’s crucial to consult with experienced legal professionals. They can provide guidance on navigating these complex situations and help you understand your options better.

The Future Landscape Of Securities Litigation And Investor Protections

Looking forward in 2025, the direction of securities litigation is being shaped by a mix of judicial interpretation, regulatory priorities, and the changing nature of corporate value itself (more intangible assets, more platform metrics, more reliance on forward-looking narratives).

Trends likely to influence securities litigation practice

A few themes that continue to matter:

- Evolving pleading expectations: Courts continue to refine what qualifies as a “strong inference” of scienter, what counts as particularized allegations, and how to treat competing inferences at the motion to dismiss stage.

- Risk factor and forward-looking statement battles: Defendants frequently argue that warnings were adequate or that statements were protected as forward-looking. Plaintiffs increasingly focus on whether warnings were generic, stale, or contradicted by known facts.

- Internal controls and governance as litigation catalysts: Admissions of material weaknesses, auditor issues, or compliance breakdowns remain a common trigger for suits, especially when paired with revenue or margin corrections.

- New disclosure frontiers: Cyber incidents, AI-related product claims, data integrity, and platform metrics are increasingly central to “what the market was told,” and therefore to what can become actionable when wrong.

- Parallel proceedings: Private actions often unfold alongside SEC investigations, DOJ inquiries, or regulatory enforcement, changing settlement dynamics and shaping what facts become public.

Final thoughts: why investor protection still depends on enforcement mechanisms

Securities litigation is not perfect. It can be expensive, slow, and heavily procedural. Some cases deserve skepticism; others reveal conduct that, absent private enforcement, might never be meaningfully addressed.

But the core idea remains durable: investors fund the system, and the system owes investors truthful disclosure.

When that bargain breaks—whether through accounting manipulation, concealed operational deterioration, misleading offering documents, or deceptive market practices—securities litigation remains one of the primary mechanisms that can impose accountability, deter repeat behavior, and return some measure of value to those harmed.

In 2025, “robust investor protection” isn’t about constant litigation. It’s about a credible threat of consequences when disclosure obligations are treated as optional.

Contact Timothy L. Miles Today for a Free Case Evaluation About Securities Class Actiion Lawsuits