Introduction to How Securities Class Action Lawsuits Work

If you have ever seen a headline like “Investors File Class Action Lawsuit Against XYZ Corp,” you were probably looking at a securities class action.

A securities class action lawsuit is a type of legal case where a group of investors (the “class”) sues a company (and sometimes its executives, directors, auditors, or underwriters) for alleged wrongdoing that affected the price of a security—most commonly a publicly traded stock. These cases usually claim the company misled investors through false statements, misleading omissions, or other deceptive conduct, and that investors suffered losses when the truth came out and the stock price dropped.

The purpose isn’t just to punish bad actors. In practice, securities class actions are designed to:

- Compensate investors who were harmed by alleged fraud or misrepresentations.

- Deter misconduct by encouraging accurate corporate disclosures and transparency.

- Support market integrity by reinforcing rules that keep capital markets fair.

Key takeaway: Understanding the basics of securities class actions is crucial for investors because these cases are highly technical, time-sensitive (especially around the “class period”), and can directly affect your ability to recover losses or assert your rights.

THE SECURITIES LITIGATION PROCESS

| Filing the Complaint | A lead plaintiff files a lawsuit on behalf of similarly affected shareholders, detailing the allegations against the company. |

| Motion to Dismiss | Defendants typically file a motion to dismiss the securities class action lawsuits, arguing that the complaint lacks sufficient claims. |

| Discovery | If the motion to dismiss is denied, both parties gather evidence, documents, emails, and witness testimonies. This phase of securities litigation can be extensive. |

| Motion for Class Certification | Plaintiffs request that the court to certify the securities litigation as a class action. The court assesses factors like the number of plaintiffs, commonality of claims, typicality of claims, and the adequacy of the proposed class representation. |

| Summary Judgment and Trial | Once the class is certified, the parties may file motions for summary judgment. If the case is not settled, it proceeds to trial, which is rare for securities class actions. |

| Settlement Negotiations and Approval | Most securities litigation cases are resolved through settlements, negotiated between the parties, often with the help of a mediator. The court must review and grant preliminary approval to ensure the settlement is fair, adequate, and reasonable. |

| Class Notice | If the court grants preliminary approval, notice of the settlement is sent to all class members in the securities litigation, often by mail, informing them about the terms and how to file a claim. |

| Final Approval Hearing | The court conducts a final hearing to review any objections and grant final approval of the settlement of the securities litigation. |

| Claims Administration and Distribution | A court-appointed claims administrator manages the process of sending notices, processing claims from eligible class members, and distributing the settlement funds. The distribution is typically on a pro-rata basis based on recognized losses. |

Understanding Securities Class Actions

At a high level, securities class actions are usually built around the idea that investors relied on a company’s public statements (press releases, SEC filings, earnings calls, investor presentations) and that those statements were materially false or misleading. When corrective information or a corrective disclosure becomes public, the stock price can fall—sometimes sharply—causing losses for people who bought at inflated prices.

What is the “class period” (and why it matters)?

One of the most important concepts in a securities class action is the class period.

The class period is the time window during which the alleged misconduct occurred and during which investors may be included in the “class” if they bought (or sometimes held) the security.

Think of it like this:

- The lawsuit claims the market price was artificially inflated (or otherwise distorted) because of misinformation.

- The class period begins when the alleged misleading statements (or omissions) started affecting the market.

- The class period ends when the truth is revealed (often through a corrective disclosure), and the market price adjusts.

Why it matters:

- Eligibility: If you purchased the stock during the class period, you may be eligible to participate in a settlement or recovery.

- Damages calculations: Losses are not calculated simply by “I lost money.” Courts and settlement administrators often use formulas tied to purchase dates, sale dates, and price movement after corrective disclosures.

- Deadlines: Important dates (like the deadline to seek lead plaintiff status) often relate to the filing of the complaint and the definition of the class period.

If you are an investor, you don’t need to memorize the legal mechanics—but you should understand that the dates you bought and sold can change whether you’re part of the class and how any recovery is computed.

Federal vs. state securities laws: what applies?

Securities class actions can involve federal law, state law, or both—but most large investor class actions involving public companies are primarily federal.

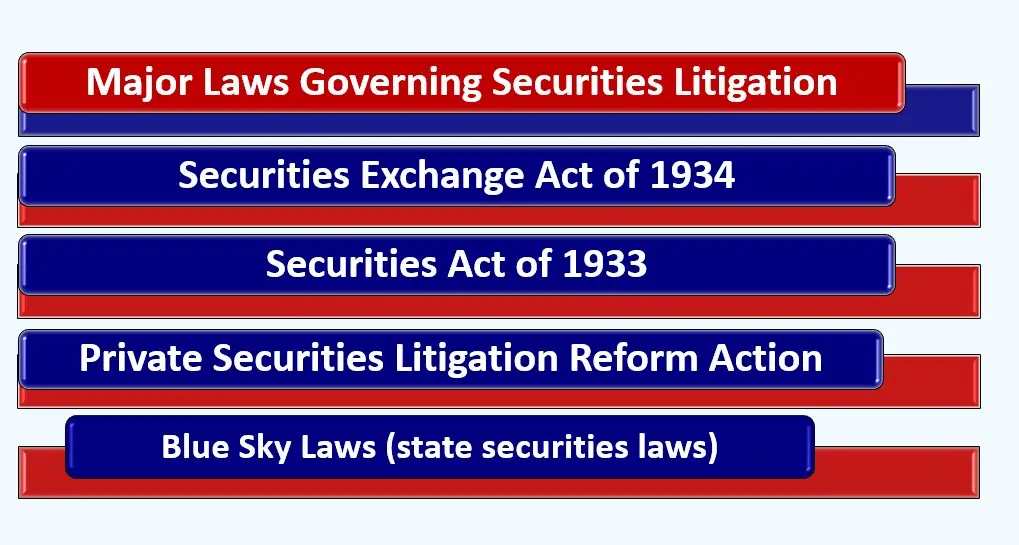

Federal securities laws (most common in major class actions)

Many securities class actions are filed under:

- Section 10(b) of the and SEC Rule 10b‑5 (the “workhorse” antifraud provisions of Securities Exchange Act of 1934)

- Section 11 of the Securities Act of 1933 (often involving misstatements in registration statements, such as those used in IPOs or secondary offerings).

- Section 12(a)(2) of the Securities Act of 1933 (often involving misstatements in offering materials).

- Section 20(a) “control person” claims (often asserted against executives/directors who allegedly controlled the primary violator).

Federal cases typically proceed in federal court and are influenced heavily by the Private Securities Litigation Reform Act (PSLRA), which adds specialized procedures and heightened pleading standards for many securities fraud claims.

State securities laws (“blue sky” laws)

States also have securities statutes—often called blue sky laws—and state consumer protection laws that can sometimes be used in investment-related disputes. However, broad state-law securities class actions involving nationally traded securities are often limited by federal statutes that aim to keep certain large securities class actions in federal court.

In practical terms:

- Large public-company fraud cases usually proceed under federal law.

- Certain localized offerings, private placements, or broker-related claims may involve state securities laws more prominently.

Common Causes of Securities Fraud Leading to Class Actions

Securities class actions usually don’t come from minor mistakes or normal business disappointments. They tend to arise when investors allege that a company materially misrepresented its business or financial condition—or hid significant risks—in a way that distorted the market price.

Below are some of the most common allegations that trigger securities litigation.

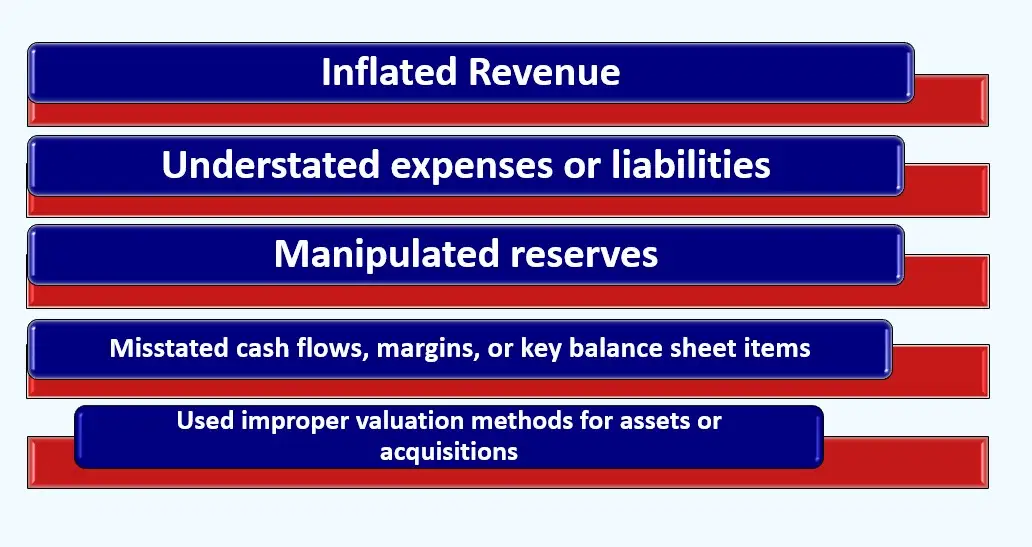

1) Accounting fraud and financial misstatements

This is one of the most common drivers of major securities class actions.

Examples include allegations that a company:

- Inflated revenue (fake sales, channel stuffing, recognizing revenue too early)

- Understated expenses or liabilities

- Manipulated reserves (e.g., bad debt reserves) to smooth earnings

- Misstated cash flows, margins, or key balance sheet items

- Used improper valuation methods for assets or acquisitions

These cases often erupt after:

- A restatement of financial statements

- A whistleblower report

- An auditor resignation or adverse opinion

- A regulatory investigation becoming public

When investors learn that reported earnings were unreliable, the market often reassesses the company rapidly—sometimes wiping out billions in market capitalization.

2) Misleading guidance and “too-good-to-be-true” growth stories

Public companies often give forward-looking statements: revenue targets, margin expectations, subscriber growth projections, or demand forecasts. These statements can become securities claims if investors allege the company:

- Had contrary internal data (e.g., sales pipeline collapsing)

- Ignored known operational problems

- Presented aspirational goals as if they were realistic, current expectations

Not every missed forecast equals fraud. The issue is usually whether the company allegedly knew (or was reckless in not knowing) that its public narrative didn’t match reality.

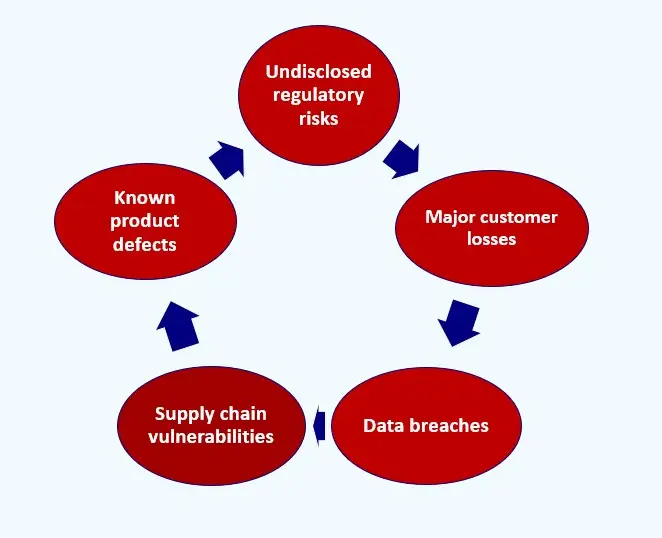

3) Hidden risks and inadequate disclosures: Lack of internal controls

Sometimes the allegation isn’t “they lied,” but “they didn’t disclose something they were required to disclose.” Common examples include:

- Undisclosed regulatory risks or ongoing government investigations

- Known product defects or safety issues

- Major customer losses or concentration risks

- Supply chain vulnerabilities that were already materialized internally

- Data breaches or cybersecurity incidents not properly disclosed

4) Insider trading and conflicts (often alongside misstatements)

Insider trading allegations sometimes appear in complaints as supporting facts—especially when executives allegedly sold stock while the company was making overly positive statements.

Insider selling alone doesn’t prove fraud. But unusually timed or unusually large sales can become part of a narrative that investors were kept in the dark while insiders reduced exposure.

5) Stock manipulation schemes (less common for large issuers, but still relevant)

In some cases—especially involving smaller issuers, thinly traded stocks, or microcap markets—investors may allege manipulation such as:

- Pump-and-dump promotion campaigns

- Coordinated trading to create artificial volume

- Misleading PR campaigns designed to inflate price before insiders sell

How fraudulent stock manipulation affects investors financially

Most investors feel the harm from securities fraud in a specific pattern:

- Inflation phase: Misleading statements (or omissions) cause the stock price to trade higher than it otherwise would.

- Purchase/hold decisions: Investors buy at inflated prices or hold when they otherwise would have sold.

- Corrective disclosure: The truth leaks out—earnings miss, restatement, regulatory action, investigative report, or admission.

- Price drop: The stock declines, sometimes over multiple disclosures.

- Losses crystallize: Investors suffer losses when they sell, or when the market value drops.

Securities class actions attempt to address this by seeking damages tied to the alleged inflation and subsequent correction—not simply “the price went down.”

The Litigation Process in Securities Class Action Lawsuits

Securities class actions follow a fairly structured path, especially in federal court. While every case is different, the process usually looks like this.

1) The complaint is filed

A case begins when one or more investors file a class action complaint alleging securities law violations. The complaint typically includes:

- The alleged false or misleading statements

- The time period involved (the proposed class period)

- The corrective disclosures and resulting price drops

- The legal claims (e.g., Rule 10b‑5, Section 11)

- The requested relief (damages, interest, attorneys’ fees, etc.)

2) Notice to investors and lead plaintiff motions

In many federal securities class actions, a notice is published informing potential class members that a case has been filed and that investors may move to be appointed lead plaintiff by a specified deadline (often 60 days from notice, depending on the case structure).

This step matters because the lead plaintiff can significantly influence:

- Strategy and litigation posture

- Choice of counsel

- Settlement approach

3) Appointment of lead plaintiff and lead counsel

The court selects a lead plaintiff (more on this below) and typically approves the lead plaintiff’s selection of lead counsel, assuming the choice is adequate and free of conflicts.

4) Motion to dismiss (a major early battle)

Defendants almost always file a motion to dismiss, arguing that:

- The complaint fails to plead misstatements with required specificity

- The alleged facts don’t support scienter (intent/recklessness), when required

- The alleged statements were opinions, puffery, or protected forward-looking statements

- Loss causation isn’t adequately alleged

This is often one of the most consequential phases. If the motion to dismiss is granted, the case can end early (sometimes with leave to amend, sometimes not).

5) Discovery (where evidence gets unearthed)

If the case survives dismissal, it enters discovery, which is the evidence-gathering phase. This can include:

- Internal emails and documents

- Accounting records

- Board materials

- Text messages or chat logs (where relevant and discoverable)

- Depositions of executives and key employees

- Expert discovery (finance, accounting, damages, market efficiency)

Why discovery matters: Securities fraud is often proven (or disproven) through internal records that show what executives knew, when they knew it, and whether public statements matched internal reality.

Discovery can also be expensive and time-consuming—which is one reason many cases settle after key discovery milestones.

6) Class certification

In a class action, the court must decide whether the case can proceed on behalf of a class. This step—class certification—can involve complex issues such as:

- Whether common issues predominate

- Whether the proposed class is ascertainable

- In market cases, whether reliance can be presumed (often tied to market efficiency concepts)

7) Summary judgment, trial, or (most commonly) settlement

Many securities class actions settle at some point rather than go to trial. Settlement timing varies:

- Some settle after surviving the motion to dismiss

- securities cases settle after discovery

- A smaller number proceed toward summary judgment or trial

If there is a settlement:

- The court reviews and preliminarily approves it

- Class members receive notice and can submit claims

- The court holds a final approval hearing

- Funds are distributed after approval and administration

Role of Lead Plaintiffs in Securities Class Actions

If you have ever wondered why some investor names appear in headlines—often pension funds, asset managers, or large institutions—it’s usually because they’re seeking (or have obtained) the role of lead plaintiff.

Who can be a lead plaintiff?

A lead plaintiff is a class member appointed by the court to represent the interests of the entire class. Lead plaintiffs can include:

- Institutional investors (public pension funds, union funds, endowments)

- Asset managers

- High-net-worth individual investors

- Sometimes groups of investors (depending on the court’s view)

The lead plaintiff is not “the only victim.” They’re the representative who helps steer the case.

Why the lead plaintiff role matters

The lead plaintiff typically:

- Oversees the litigation with counsel

- Helps set strategy and major decisions

- Reviews settlement proposals

- Can influence how aggressively the case is pursued

- Serves as a check on attorneys (at least in theory) to ensure the case is run in the class’s best interests

In other words, the lead plaintiff can shape the outcome far more than an average class member who simply files a claim at the end.

How courts select the lead plaintiff (financial interest is key)

While exact standards vary by jurisdiction and case type, courts often consider:

- Largest financial interest in the relief sought (often a primary factor)

- Whether the candidate is an “adequate” representative (no major conflicts)

- Typicality of claims (their claims align with the class)

- Ability to supervise counsel (institutions often viewed favorably here)

“Largest financial interest” is not always just net loss. Courts may evaluate multiple metrics, such as:

- Total shares purchased during the class period

- Net shares purchased (purchases minus sales)

- Approximate losses attributable to the alleged fraud

- Timing of purchases relative to disclosures

The theory is straightforward: the investor with the most at stake may have the greatest incentive to pursue the case seriously and negotiate responsibly.

Financial Recovery in Securities Class Action Cases

A lot of investors only engage with securities class actions at the end, when they receive a settlement notice. The key questions then become: How much money is available? How do I get my share? What do lawyers take?

How settlement funds are distributed among class members

If a case settles (or results in a monetary judgment), the money generally goes into a settlement fund. Distribution typically works like this:

- Court approval of settlement terms

- The judge must approve the settlement as fair, reasonable, and adequate.

- Notice and claims process

- Eligible investors are notified (directly if identifiable, and through publication). Investors submit a claim form with proof of transactions (broker statements, trade confirmations).

- Plan of allocation

- The settlement includes a formula—often called a plan of allocation—that determines each investor’s recognized loss and proportional share.

- Deductions before payouts

- The fund is reduced by:

- Court-approved attorneys’ fees

- Litigation expenses

- Settlement administration costs

- (and sometimes other court-approved costs)

- Payments to class members

- Investors receive payments based on their calculated share. In many cases, payouts are partial recovery, not full reimbursement of losses.

Important practical point: two investors with the same “total loss” may receive different recognized losses depending on purchase dates, sale dates, and how the corrective disclosures unfolded.

Typical attorney fee structures (including contingency fees)

Securities class actions are usually handled on a contingency fee basis. That means:

- Attorneys typically advance litigation costs (experts, discovery, depositions).

- They get paid only if there is a settlement or judgment.

- Fees are typically requested as a percentage of the recovery and must be approved by the court.

While the percentage varies by case and court, the key concept is that fees are not simply set by the lawyers—they’re subject to judicial oversight, objections, and review of the work performed.

Also, class counsel usually seeks reimbursement of out-of-pocket litigation expenses, again subject to court approval.

Importance of Internal Controls and Corporate Accountability

Behind a large percentage of securities class actions is the same underlying issue: a gap between what a company told the market and what was happening internally. The lack of internal controls leads to many securities class actions.

Role of strong internal controls in preventing fraud and violations

Internal controls are the policies and procedures companies use to ensure:

- Financial reporting is accurate

- Transactions are properly authorized and recorded

- Fraud risks are identified and mitigated

- Compliance issues are detected early

- Management receives reliable internal reporting

Weak internal controls can lead to:

- Unreliable financial statements

- Undetected revenue recognition problems

- Improper expense capitalization

- Inadequate oversight of subsidiaries or foreign operations

- Poor documentation around key estimates and assumptions

Even when fraud isn’t proven, disclosures about material weaknesses in internal controls can trigger market concern—and sometimes litigation—because they suggest financial reporting may not be trustworthy.

How securities class actions promote accountability and transparency

Securities class actions are not the only enforcement tool (regulators and criminal authorities may also act), but they create a private mechanism that can:

- Push companies to correct public statements

- Encourage stronger disclosure practices

- Incentivize boards and audit committees to take oversight seriously

- Deter future misconduct by increasing the cost of misleading the market

They also force uncomfortable questions into the open—about governance, risk management, executive incentives, and whether leadership prioritized short-term market optics over accuracy.

In that sense, even when investors recover only a fraction of losses, the broader function can be improving how companies communicate with the market.

Reputational and Financial Consequences of Fraud

Impact Assessment of Financial Statement Fraud

| Impact Category | Measurement | Severity |

|---|---|---|

| Stock Value Loss | 12.3-20.6% average decline | High |

| Reputational Damage | Up to 100x direct financial loss | Severe |

| Employee Impact | 50% loss in cumulative wages | Severe |

| Legal Penalties | $750M+ in major cases | High |

| Bankruptcy Risk | 3x higher than non-fraud firms | High |

| Market Recovery | Years to decades, if ever | Variable |

| Customer Trust | Immediate and often permanent loss | Severe |

| Investment Access | Permanently impaired in many cases | High |

Key Components of Strong Internal Controls

Building effective internal controls involves several key components. These components form the backbone of a strong internal control system, ensuring that your organization operates efficiently and ethically.

- Control Environment: This is the foundation of any internal control system. It includes the organization’s values, integrity, and ethical standards. A strong control environment sets the tone for the entire organization, emphasizing the importance of internal controls.

- Risk Assessment: Identifying and assessing risks is crucial to implementing effective internal controls. By understanding potential threats, you can develop strategies to mitigate them, ensuring that your organization is well-prepared to face challenges.

- Control Activities: These are the policies and procedures put in place to address identified risks. Control activities ensure that management directives are carried out effectively, preventing errors and irregularities

- Information and Communication: Effective internal controls rely on timely and accurate information. Ensuring that relevant information is communicated to the right people is vital for decision-making and accountability.

- Monitoring: Continuous monitoring of internal controls is essential to ensure their effectiveness. Regular assessments help identify areas for improvement, ensuring that your internal control system remains relevant and robust.

By focusing on these components, you can implement a comprehensive internal control framework that supports your organizational objectives.

Notable Securities Class Action Cases and Their Impact on Investors

Some securities class actions have produced multi-billion-dollar recoveries, shaping how investors, companies, auditors, and regulators think about disclosure and accountability.

Below are a few widely cited examples and what they taught the market. (These summaries are high-level and intended to illustrate impact rather than cover every legal detail.)

Enron

- The Enron scandal remains the quintessential example of how omissions in financial statements can devastate markets and investors.

- The energy company employed sophisticated accounting fraud schemes, including the use of special purpose entities (SPEs) to hide over $1 billion in debt from its balance sheets.

- These corporate scandals involved deliberate omissions of critical financial information that painted a false picture of the company’s financial health.

- Key Legal Precedents Established:

- Enhanced auditor independence requirements under the Sarbanes-Oxley Act

- Stricter CEO and CFO certification of financial statements

-

- Whistleblower protection provisions that encouraged internal reporting of fraud

- The securities litigation that followed resulted in one of the largest bankruptcy proceedings in U.S. history, with investors losing approximately $74 billion in market value.

- The case established crucial precedents for regulatory compliance, particularly regarding the disclosure of off-balance-sheet transactions and the independence of external auditors.

Valeant Pharmaceuticals (now Bausch Health)

- The scandal: Between 2013 and 2015, Valeant (now Bausch Health) pursued a business model that relied on aggressively hiking drug prices and using a secret network of controlled pharmacies to boost sales. These actions inflated the company’s stock price and created the illusion of robust growth. When this deceptive strategy was exposed, the company’s stock plummeted.

- The litigation: In the aftermath, investors filed a securities class action lawsuit, leading to a $1.2 billion settlement, one of the largest ever against a pharmaceutical company. The SEC also charged Valeant and former executives with accounting violations, resulting in penalties and reimbursement of incentive compensation.

Under Armour

- The scandal: For several years leading up to 2017, the athletic apparel maker Under Armour used a practice known as “pulling forward” sales from future quarters to meet analysts’ revenue targets. After it became impossible to sustain the practice, the company reported a significant drop in revenue growth in 2017. An SEC investigation revealed that company executives were aware of the practices and misled investors and analysts by attributing revenue growth to other factors.

- The litigation: Following the revelations, Under Armour faced both an SEC enforcement action and a securities class action lawsuit from investors. The company agreed to a $9 million penalty in the SEC case and, in 2024, settled the shareholder suit for a record-setting $434 million.

Sunbeam

- The scandal: During the 1990s, Sunbeam, under the leadership of CEO “Chainsaw Al” Dunlap, engaged in fraudulent accounting practices to meet aggressive financial targets. The company created “cookie-jar” reserves in 1996 and used them to artificially boost income in 1997. It also improperly recognized revenue from “bill and hold sales,” where products were billed to customers but not shipped.

- The litigation: The SEC charged Dunlap and other executives with fraud, and Sunbeam eventually filed for bankruptcy. A securities class action led to a $142 million settlement for investors.

5. Livent

- The scandal: The Canadian theatrical company Livent, founded by Garth Drabinsky and Myron Gottlieb, manipulated its books throughout the 1990s to paint a picture of financial success. The accounting scheme involved capitalizing pre-production costs as long-term fixed assets, erasing expenses from the general ledger, and improperly recognizing revenue. The fraud was designed to secure financing and mislead investors about the company’s true performance.

- The litigation: After the fraud was uncovered, Livent collapsed, and Drabinsky and Gottlieb were criminally convicted of fraud. A lawsuit against the company’s auditor, Deloitte & Touche, found them negligent for failing to catch the extensive fraud.

6. Tyco International

- The scandal: Former CEO L. Dennis Kozlowski and CFO Mark Swartz embezzled hundreds of millions of dollars from the company in the early 2000s, using it to fund lavish personal lifestyles. To conceal the theft and maintain the appearance of strong financial performance, they made false and misleading statements to investors.

- The litigation: Kozlowski and Swartz were convicted of grand larceny, securities fraud, and other crimes. Tyco settled shareholder lawsuits for $3 billion, one of the largest securities class action settlements at the time, and its auditor paid an additional $225 million to settle claims.

The bigger takeaway from landmark cases

Across major cases, the repeating themes are:

- Markets price in trust. When trust collapses, the repricing is violent.

- Disclosure isn’t just about numbers—it’s about risk, controls, and candor.

- Large recoveries can compensate investors, but they also signal to the market that deception has consequences.

Market Impact After Major Corporate Scandals

Stock Price Impact After Fraud Disclosure

| Time Period | Average Stock Price Decline |

|---|---|

| Immediate Impact (1 Day) | 5-10% |

| Short-Term Impact (20 Days) | 12.3% |

| Companies with Settlements | 14.6-20.6% |

| Companies Later Cleared | 7.2% |

| Extreme Cases (e.g., Luckin Coffee) | 80%+ |

Conclusion

Securities class action lawsuits exist because public markets only work when investors can rely on truthful, complete, and timely information. When companies allegedly distort that information—through misstatements, omissions, or fraudulent schemes—class actions give investors a way to seek recovery and push the system back toward fairness.

Participation in these cases isn’t just about getting a check (though that matters). It’s also a way the market enforces standards: accurate reporting, honest risk disclosure, and real accountability when companies fall short.

If you invest in public companies, the most practical habits are simple:

- Pay attention to news about investigations, restatements, and corrective disclosures.

- Keep good records of your trades and statements.

- When you see a case announced, check the class period and your transaction dates.

- Stay informed about your rights and deadlines, especially if you suffered significant losses during the class period.

Capital markets reward transparency over time. Securities class actions are one of the tools investors have to demand it.