Introduction to Enhancing Financial Internal Controls

- Enhancing Financial Internal Controls: Involves implementing stronger segregation of duties, using technology for automation, culture through training and clear documentation. Regularly monitoring and auditing processes provides objective feedback to identify and address weaknesses, ensuring controls remain effective and compliant over time.

- Financial Internal Controls: Are essential mechanisms that organizations implement to safeguard assets, ensure accuracy in financial reporting, and promote operational efficiency. These controls form the backbone of any financial management system, providing a structured approach to risk management and compliance. By establishing robust internal controls, you can effectively monitor financial activities and mitigate potential risks that may lead to financial discrepancies or regulatory violations.

- Implementation: Implementing financial internal controls is not merely a regulatory requirement; it is a strategic necessity. They serve as the first line of defense against accounting fraud and financial misstatements, which can severely damage an organization’s reputation and financial health. In today’s complex financial landscape, having strong internal controls helps you maintain investor confidence and protect against securities litigation.

- Accurate Financial Data: Moreover, effective financial internal controls contribute to improved decision-making. By ensuring the accuracy and reliability of financial data, you enable better forecasting and strategic planning. This, in turn, enhances your organization’s ability to achieve its financial objectives, providing a competitive edge in the market.

Key Strategies for Enhancement

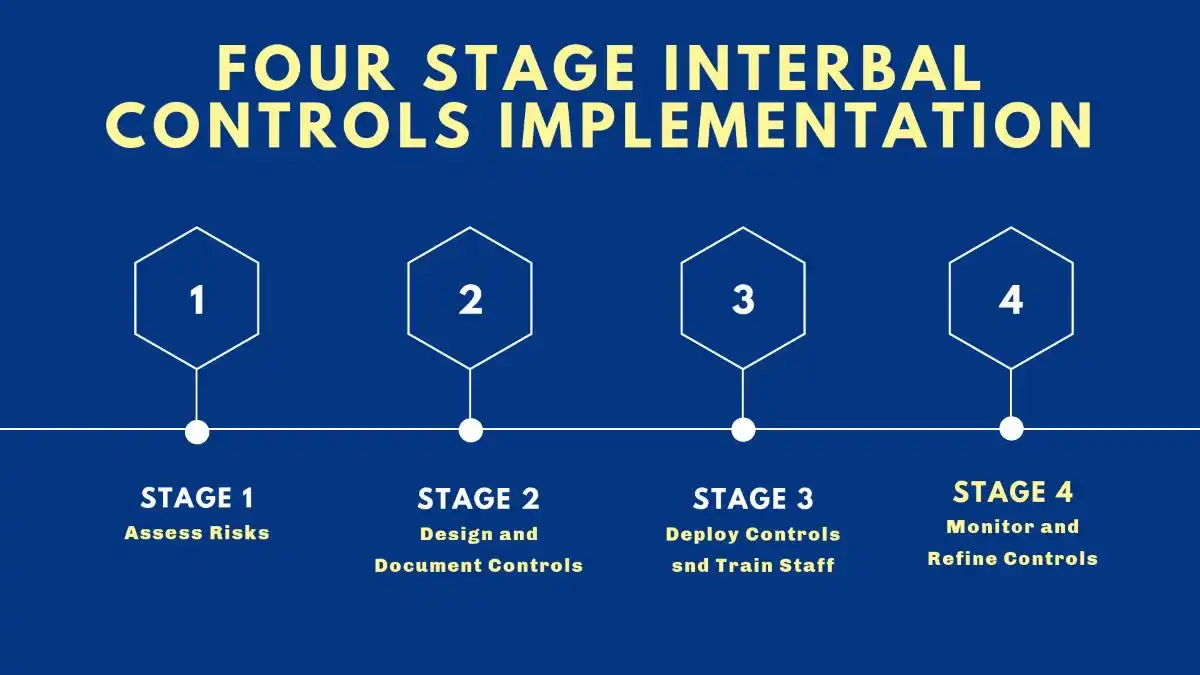

- Financial Internal Controls: Are essential mechanisms that organizations implement to safeguard assets, ensure accuracy in financial reporting, and promote operational efficiency. These controls form the backbone of any financial management system, providing a structured approach to risk management and compliance. By establishing robust internal controls, you can effectively monitor financial activities and mitigate potential risks that may lead to financial discrepancies or regulatory violations. Ensure no single person has control over an entire transaction from start to finish to prevent fraud and errors. This includes separating authorization from payment functions.

- Implement and document procedures: Clearly define and document all policies and procedures for consistency. Require employees to read and sign off on these policies annually.

- Automate and use technology: Use modern technologies like (ERP) systems and automated monitoring tools to reduce manual errors, increase efficiency, and provide real-time oversight.

- Conduct regular monitoring and audits: Perform periodic audits to identify control gaps and inconsistencies. Use technology to analyze 100% of transactions instead of just samples to find anomalies.

- Enhance employee training and culture: Foster a culture of integrity and train employees to recognize and report issues. Communication across departments is also crucial for a comprehensive control environment.

- Improve access controls: Limit access to sensitive financial data and system functions to only those with a job-related need.

- Regularly assess and adapt: Internal controls should evolve with the business. Perform regular risk assessments to identify new vulnerabilities and adapt controls accordingly.

- Secure assets: Implement controls to secure physical and digital assets to prevent theft or misuse.

Ensure compliance: Make sure all new and existing controls comply with relevant legal requirements and industry standards.

Common Financial Statement Fraud Schemes

| Scheme Type | Description | Example |

| Fictitious Revenue | Recording non-existent sales through false documentation and phantom customers | Creating counterfeit sales contracts or engaging in fraudulent bill-and-hold arrangements that lack economic substance |

| Premature Revenue Recognition | Recognizing revenue before satisfying essential accounting criteria | Accelerating revenue recognition before completing contracted service obligations or product delivery requirements |

| Channel Stuffing | Forcing excessive inventory into distribution channels to artificially inflate sales | Providing unusual incentives to distributors to accept unnecessary inventory levels that exceed reasonable demand |

| Asset Overstatement | Deliberately inflating reported asset values through accounting manipulation | Recording phantom inventory or applying inadequate depreciation to overstate asset carrying values |

| Liability Concealment | Hiding financial obligations through improper accounting treatments | Deliberately understating debt levels or warranty obligations through accounting manipulation |

| Material Omissions | Withholding critical information required for informed investment decisions | Failing to disclose significant related party transactions or contingent liabilities |

| Journal Entry Manipulation | Falsifying accounting records through improper manual adjustments | Making unsupported last-minute entries near reporting deadlines to manipulate results |

The Role of Internal Controls in Preventing Accounting Fraud

- Internal controls play a pivotal role in preventing accounting fraud by establishing checks and balances within financial operations. These controls are designed to detect and prevent errors and fraudulent activities before they can cause significant harm. For instance, segregation of duties ensures that no single individual has control over all aspects of a financial transaction, reducing the likelihood of fraudulent behavior.

- To combat accounting fraud effectively, you must implement a comprehensive system of internal controls that includes preventive, detective, and corrective measures. Preventive controls, such as authorization procedures and access restrictions, deter fraudulent activities. Detective controls, like audits and reconciliations, help identify discrepancies and potential fraud. Corrective controls ensure that any identified issues are promptly addressed and resolved.

- By fostering a culture of accountability and transparency, internal controls also deter fraudulent activities by setting clear expectations for ethical behavior. Training programs and regular communication about your organization’s commitment to integrity further reinforce the importance of adhering to established controls and ethical standards.

Key Components of Effective Internal Controls

An effective internal control system is built on several key components that work together to safeguard financial integrity. These components include:

- Control Environment: Establishing a strong control environment is crucial for setting the tone at the top. This involves leadership commitment to ethical values, a clear organizational structure, and a culture that supports risk management.

- Risk Assessment: Regular risk assessments help identify potential threats to financial processes. By analyzing these risks, you can prioritize and implement appropriate control measures to mitigate them effectively.

- Control Activities: These are the policies and procedures put in place to ensure that management directives are carried out. Control activities include reconciliations, verifications, approvals, and authorization processes.

- Information and Communication: Effective communication channels ensure that relevant information is disseminated throughout the organization. This includes sharing updates on internal controls, reporting mechanisms, and compliance requirements.

- Monitoring: Continuous monitoring of internal controls is essential to ensure their effectiveness. This involves regular evaluations, audits, and updates to control systems to address emerging risks and challenges.

By integrating these components into your internal control framework, you enhance your organization’s ability to prevent, detect, and respond to financial irregularities.

Corporate Governance and Its Impact on Financial Internal Controls

- Corporate governance refers to the system of rules, practices, and processes by which a company is directed and controlled. It plays a significant role in shaping financial internal controls, as effective governance ensures that an organization is managed in the best interests of its stakeholders. Strong corporate governance frameworks promote transparency, accountability, and integrity within financial operations.

- A robust governance structure supports internal controls by clearly defining roles and responsibilities. The board of directors, audit committees, and executive management are integral to overseeing the implementation and effectiveness of internal controls. By establishing clear lines of authority and accountability, corporate governance helps prevent conflicts of interest and ensures compliance with regulatory requirements.

- Moreover, corporate governance enhances the credibility of financial reporting. By aligning internal controls with governance principles, you create a reliable and transparent financial reporting process that fosters investor trust. This alignment is crucial in protecting your organization from securities litigation, as it demonstrates a commitment to ethical practices and regulatory compliance.

Segregation of duties

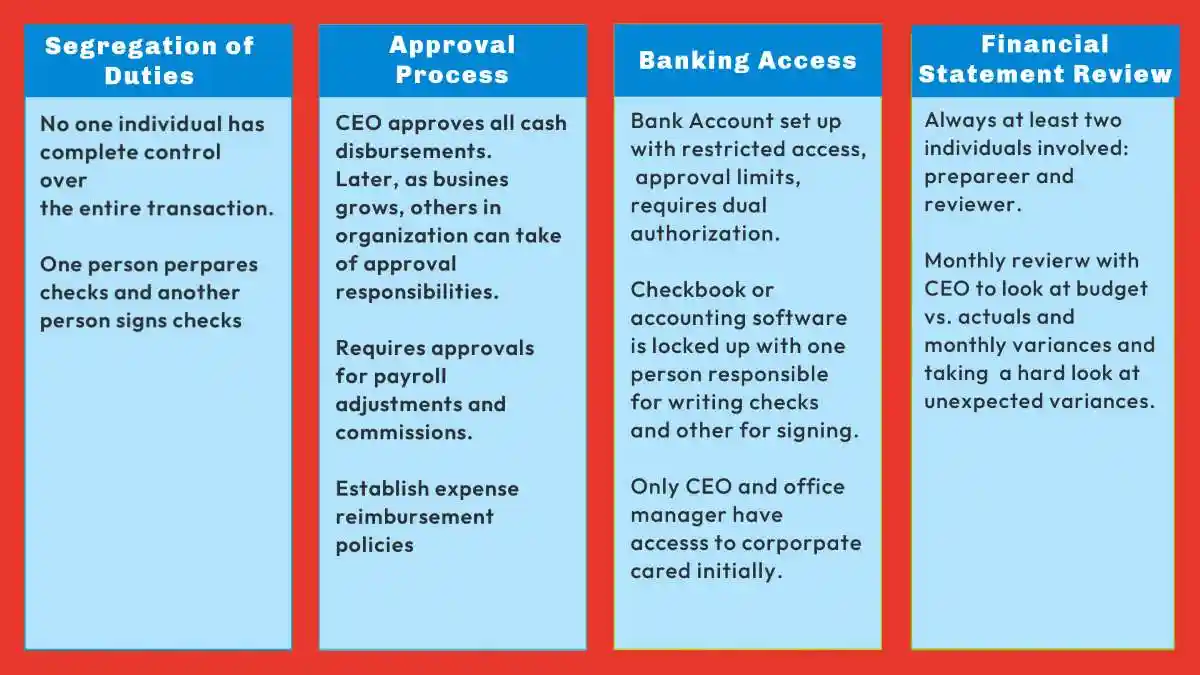

- A critical component of internal controls, proper segregation of duties prevents any single employee from having excessive control over financial processes. This fundamental control mechanism requires dividing key responsibilities among multiple individuals to create a system of checks and balances.

- For instance, the employee responsible for cash receipts should not also handle bank reconciliations, and those who approve purchases should not process vendor payments. This separation helps prevent and detect fraudulent activities by ensuring that no individual can both perpetrate and conceal improper transactions.

- Organizations must carefully evaluate their operational structure to identify critical functions that require separation. Key areas demanding segregation include:

- Authorization of transactions

- Custody of assets

- Recording of transactions

- Reconciliation of accounts

- Review and approval processes

- When proper segregation cannot be achieved due to limited staff, compensating controls like increased supervision, mandatory vacations, and regular rotation of duties become essential safeguards against fraud.

Strengthening Internal Controls

Robust internal controls serve as the foundation for preventing asset misappropriation. Organizations should implement comprehensive control policies that include:

- Regular internal audits conducted by independent personnel

- Detailed documentation requirements for all financial transactions

- Strict authorization protocols for accessing sensitive systems and data

- Mandatory dual approval for transactions above specified thresholds

- Regular reconciliation of accounts by independent reviewers

- Comprehensive audit trails for all system activities

- Periodic risk assessments to identify control weaknesses

- Regular employee training on fraud prevention and detection

- Clear policies regarding conflicts of interest and ethical conduct

- Whistleblower protection programs encouraging reporting of suspicious activities

Physical and Digital Access Controls

- Modern organizations must maintain stringent access controls across both physical and digital domains:

- Physical Controls:

-

- Restricted access to valuable inventory areas

- Secure storage for sensitive documents

- Video surveillance of critical areas

- Key card access systems

- Regular inventory counts

- Visitor logging and escort requirements

Digital Controls:

- Multi-factor authentication for system access

- Role-based access restrictions

- Regular password changes

- Audit logging of system activities

- Encryption of sensitive data

- Network segmentation

- Regular security assessments

- Prevention Through Strong Internal Controls

- Effective prevention requires a multi-layered approach:

- Policy Framework:

-

- Clear procedures for all financial processes

- Documented approval requirements

- Regular policy reviews and updates

- Employee acknowledgment procedures

- Consequence management protocols

- Monitoring Systems:

-

- Regular control testing

- Independent oversight

- Continuous monitoring programs

- Exception reporting

- Performance metrics

- Training and Awareness:

-

- Regular fraud awareness training

- Ethics education programs

- Policy communication

- Case study reviews

- Updates on new fraud schemes

By implementing these comprehensive controls and detection methods, organizations can significantly reduce their vulnerability to asset misappropriation while protecting shareholder value and maintaining market confidence.

- Incompatible duties represent a critical weakness in internal controls that creates significant fraud risk. These occur when a single employee maintains responsibility for multiple key financial functions that should be separated to prevent fraud. The core functions that require separation include:

-

- Authorization: The power to approve financial transactions and expenditures. This includes approving purchase orders, expense reports, vendor payments, and other financial commitments that impact company assets. Proper authorization controls ensure transactions are legitimate and align with business needs.

-

- Custody: Direct physical control or access to company assets, including cash, inventory, equipment, and other valuable property. Custody also extends to digital assets like bank account access, investment accounts, and payment systems. Strong custody controls prevent unauthorized access and protect assets from misappropriation.

-

- Record-keeping: The ability to enter, modify, or delete transaction records in the accounting system. This encompasses journal entries, ledger updates, and financial statement preparation. Proper record-keeping controls maintain accurate documentation and prevent fraudulent alterations.

-

- Reconciliation: The responsibility for comparing and verifying different sets of records, such as bank statements to internal records, or physical inventory counts to system records. Effective reconciliation serves as a critical detective control to identify discrepancies and potential fraud.

-

- Example: A classic case of incompatible duties occurs when a single employee handles multiple financial functions. For instance, if one person receives customer payments, records those transactions in the accounting system, and performs bank reconciliations, they could easily commit fraud by stealing incoming cash and manipulating records to cover their tracks. This scenario eliminates the checks and balances that proper segregation provides.

Management and oversight

- Inadequate supervision creates significant opportunities for asset misappropriation when management fails to properly monitor employee activities and business processes. This risk becomes particularly acute in remote locations or satellite offices where direct oversight is limited. Without proper supervision, fraudulent schemes can persist undetected for extended periods, leading to substantial losses that impact shareholder value.

- Ineffective management review represents another critical control weakness that enables fraud. When managers do not thoroughly review transactions, supporting documentation, and account reconciliations, employees can more easily process fraudulent transactions or manipulate records. Regular management review serves as a crucial detective control that helps identify suspicious patterns or unauthorized activities before they result in significant losses.

- Management override of controls poses a particularly serious threat to organizational integrity. When senior leaders bypass established internal controls for operational expediency or personal gain, it sends a devastating message throughout the organization that controls are optional. This behavior erodes the control environment and creates an atmosphere where fraud can flourish. Additionally, management override often involves complex schemes that are difficult to detect through normal control procedures.

- Poor hiring practices significantly increase fraud risk when organizations fail to conduct thorough background checks and screening procedures for employees who will have access to assets or financial systems. Critical screening elements should include:

-

- Criminal background checks

- Credit history review

- Employment verification

- Education confirmation

- Professional reference checks

- Drug testing where appropriate

- Physical and information safeguards

- Inadequate physical controls create direct opportunities for asset misappropriation. Common weaknesses include:

-

- Unsecured cash storage areas

- Poor inventory warehouse security

- Unrestricted access to equipment and supplies

- Inadequate surveillance systems

- Weak key control procedures

- Poor perimeter security

- Insufficient access restrictions

- Weak access controls over information systems and data represent a growing fraud risk in today’s digital environment. Organizations must implement robust controls including:

-

- Strong password requirements

- Multi-factor authentication

- Role-based access restrictions

- Regular access reviews

- System activity monitoring

- Data encryption

- Network segmentation

- Recording and documentation

- Poor record keeping severely compromises an organization’s ability to prevent and detect fraud. Inadequate documentation creates gaps in the audit trail that fraudsters can exploit. Critical documentation that must be maintained includes:

-

- Original invoices and receipts

- Purchase orders and contracts

- Shipping and receiving records

- Employee expense reports

- Journal entry support

- Account reconciliations

- Approval documentation

- Lack of independent checks removes a crucial detective control that helps identify fraudulent activity. Regular independent verification should include:

-

- Bank reconciliations

- Inventory counts

- Asset verifications

- Account reviews

- Transaction testing

- System access audits

- Control assessments

- Failure to enforce mandatory vacations eliminates an important fraud detection mechanism. When employees engaging in fraud must take time off, their schemes often become apparent as other workers temporarily assume their duties. Organizations should require:

-

- Minimum vacation periods

- Cross-training of duties

- Rotation of responsibilities

- Backup personnel assignment

- Transaction review during absences

Technology and automation

- Insufficient use of automation increases fraud risk by relying too heavily on manual processes that are more susceptible to manipulation and error. Organizations should leverage technology to:

-

- Automate transaction processing

- Implement system controls

- Generate exception reports

- Monitor user activity

- Enforce segregation of duties

- Maintain audit trails

- Detect anomalies

- Failure to update technology leaves organizations vulnerable to both internal fraud and external threats. Outdated systems often lack:

- Modern security features

- Automated controls

- Audit capabilities

- Integration capabilities

- Detection tools

- Monitoring functions

- Reporting capabilities

- Poorly integrated systems create control gaps that fraudsters can exploit. When systems don’t properly communicate, organizations face:

- Duplicate data entry

- Reconciliation challenges

- Limited visibility

- Control weaknesses

- Detection delays

- Reporting issues

- Compliance risks

- A poor “tone at the top” fundamentally undermines an organization’s control environment and creates conditions where asset misappropriation can flourish. When senior leadership fails to demonstrate commitment to internal controls and ethical behavior, it erodes organizational integrity and increases fraud risk through multiple mechanisms.

Common Weaknesses in Internal Controls and How to Address Them

- Even with a well-designed internal control system, weaknesses may arise that can compromise financial integrity. Common weaknesses include inadequate segregation of duties, lack of regular monitoring, and insufficient documentation of procedures. Addressing these weaknesses promptly is essential to maintain the effectiveness of your internal controls.

-

- Segregation of Duties: To address this weakness, ensure that financial responsibilities are divided among multiple individuals. This prevents any single employee from having excessive control over financial transactions, reducing the risk of fraud and errors.

- Regular Monitoring: Implementing continuous monitoring practices helps identify control weaknesses early. Regular audits, reviews, and assessments are essential to ensure that internal controls remain effective and relevant in a changing business environment.

- Documentation and Communication: Clear documentation of control procedures and regular communication about their importance are vital. This ensures that all employees understand their roles in maintaining internal controls and are aware of any updates or changes.

- By proactively addressing these common weaknesses, you strengthen your internal control framework and enhance overall financial resilience.

The Consequences of Poor Internal Controls in Securities Litigation

- The absence of effective internal controls can have severe consequences, particularly in the context of securities litigation. Poor controls increase the likelihood of financial misstatements, fraud, and regulatory non-compliance, all of which can lead to costly legal proceedings and damage to your organization’s reputation.

- Securities litigation often arises when investors believe they have been misled by inaccurate financial reporting or fraudulent activities. In such cases, organizations with weak internal controls may face significant legal liabilities, including fines, penalties, and restitution payments. Additionally, the reputational damage associated with litigation can result in a loss of investor confidence and market value.

- To mitigate these risks, it is essential to establish and maintain a robust internal control framework. By demonstrating a commitment to transparency, accountability, and ethical practices, you can reduce the likelihood of securities litigation and protect your organization’s financial stability and reputation.

The Value of Transparency in Corporate Governance

- Building Trust Through Transparency: Transparency serves as a cornerstone of effective corporate governance by ensuring stakeholders have comprehensive access to material information. This enables:

-

- Informed decision-making through detailed disclosure of financial data, operational metrics, and strategic initiatives

- Clear visibility into management’s actions and organizational performance

- Regular communication of both positive developments and potential challenges

- Timely updates on internal control effectiveness and compliance matters

- Detailed reporting on risk management activities and mitigation strategies

- Comprehensive disclosure of governance practices and board oversight

- Strengthening Stakeholder Relationships: When organizations prioritize transparency, they create stronger bonds with key stakeholders by:

-

- Demonstrating respect for shareholders’ right to material information

- Building credibility through consistent and honest communication

- Fostering trust through proactive disclosure practices

- Enabling effective dialogue between management and stakeholders

- Supporting collaborative problem-solving through shared understanding

- Maintaining open channels for feedback and engagement

- Providing context for strategic decisions and organizational changes

- Ensuring equitable access to relevant information

- Ethical Leadership and Accountability: Transparent practices reinforce organizational commitment to:

-

- Maintaining high ethical standards in all business activities

- Taking responsibility for both successes and setbacks

- Creating a culture of integrity throughout the organization

- Setting clear expectations for employee conduct

- Demonstrating leadership accountability at all levels

- Supporting effective internal controls through visibility

- Preventing potential securities litigation through disclosure

- Building sustainable stakeholder relationships

- Promoting Stakeholder Engagement: Transparency enables meaningful engagement by:

-

- Creating an environment where stakeholders feel valued and respected

- Encouraging active participation in governance processes

- Supporting informed dialogue on important issues

- Building confidence in management’s decision-making

- Facilitating constructive feedback mechanisms

- Strengthening corporate governance practices

- Enhancing overall organizational effectiveness

- Maintaining market confidence and trust

The Primary Objective of Securities Litigation

- Primary Objective: The fundamental purpose of securities litigation is to enforce accountability for fraudulent activities that harm investors and undermine market integrity. These legal proceedings serve as a powerful deterrent by imposing severe financial and reputational consequences on companies and executives who engage in deceptive practices.

- Accountability: Securities litigation creates accountability through:

-

- Financial penalties and damages

- Individual liability for executives

- Mandatory control improvements

- Enhanced oversight requirements

- Public disclosure of misconduct

- Reputational consequences

- Industry-wide deterrence

- This accountability mechanism helps prevent future fraud by demonstrating that deceptive practices carry serious consequences.

- Compensation: Securities litigation provides an avenue for defrauded investors to recover losses through:

-

- Class action settlements

- Disgorgement of illegal profits

- Restitution payments

- Civil monetary penalties

- Asset recovery

- Prejudgment interest

- Attorney fee awards

- These financial remedies help make investors whole while removing the profit motive from fraudulent schemes.

Understanding the Role of Securities Litigation

- Securities Litigation Objective: Understanding how securities litigation functions is crucial for:

-

- Corporate executives and directors

- Compliance professionals

- Internal audit teams

- Legal counsel

- Risk managers

- Board members

- Investors

- This knowledge helps organizations implement effective controls and avoid behaviors that could trigger costly litigation.

- Companies: For organizations, securities litigation emphasizes the critical importance of:

-

- Maintaining robust internal controls

- Ensuring accurate financial reporting

- Implementing compliance programs

- Fostering ethical culture

- Protecting whistleblowers

- Conducting thorough investigations

- Providing transparent disclosure

- These measures help prevent fraud while demonstrating the company’s commitment to regulatory compliance and shareholder protection.

- Investors

- For investors, understanding the implications of securities litigation is paramount in safeguarding their investments and contributing to market integrity. Vigilant investors who recognize warning signs of potential accounting fraud and understand the legal framework can significantly reduce their exposure while supporting transparent markets. Through active participation in securities litigation, investors play a crucial role in:

-

- Deterring future misconduct through financial consequences

- Recovering losses from fraudulent activities

- Encouraging stronger corporate governance

- Promoting market transparency and integrity

- Supporting regulatory enforcement efforts

- Protecting other shareholders’ interests

- Strengthening accountability mechanisms

THE SECURITIES LITIGATION PROCESS

- Filing the Complaint: The securities litigation process begins when a lead plaintiff files a detailed complaint on behalf of similarly affected shareholders. This complaint must specifically outline:

-

- The alleged fraudulent conduct

- Material misstatements or omissions

- Evidence of scienter (intent to deceive)

- Resulting investor damages

- Connection between fraud and losses

- Class period timeline

- Individual defendant roles

- Motion to Dismiss: Defendants typically challenge securities class action lawsuits through motions to dismiss, arguing:

-

- Insufficient pleading of fraud claims

- Lack of materiality in statements

- Absence of scienter evidence

- Missing loss causation elements

- Statute of limitations issues

- Jurisdictional challenges

- Technical pleading defects

- Discovery: Upon survival of the motion to dismiss, the discovery phase begins, involving:

- Document collection and review

- Electronic data preservation

- Witness depositions

- Expert testimony

- Financial record analysis

- Email communications review

- Internal control documentation

- Motion for Class Certification: The court evaluates class certification requests based on:

-

- Numerosity of affected investors

- Common questions of law/fact

- Typicality of lead plaintiff claims

- Adequacy of representation

- Predominance of common issues

- Superiority of class resolution

- Definable class membership

- Summary Judgment and Trial: If not settled, the case may proceed through:

-

- Summary judgment motions

- Pre-trial preparations

- Jury selection process

- Opening statements

- Witness testimony

- Expert evidence

- Closing arguments

- Settlement Negotiations and Approval: Most securities litigation resolves through settlements requiring:

-

- Mediator facilitation

- Damage calculations

- Insurance coverage analysis

- Corporate governance reforms

- Distribution methodology

- Notice procedures

- Court approval process

- Class Notice: Court-approved settlement notices must provide:

- Clear settlement terms

- Distribution procedures

- Opt-out rights

- Claim filing deadlines

- Attorney fee information

- Objection procedures

- Contact information

- Final Approval Hearing: The court conducts a fairness hearing to:

-

- Review settlement terms

- Consider objections

- Evaluate fee requests

- Assess distribution plans

- Confirm notice adequacy

- Grant final approval

- Enter judgment order

- Claims Administration and Distribution: The claims process involves:

-

- Notice dissemination

- Claim form processing

- Loss calculation verification

- Pro-rata determinations

- Payment distributions

- Tax reporting

- Reconciliation procedures

REPUTATIONAL AND FINANCIAL CONSEQUENCES OF FRAUD

- The devastating impact of financial statement fraud extends far beyond immediate monetary losses, creating long-lasting damage to organizational value, stakeholder trust, and market confidence.

- Companies engaging in accounting fraud face severe multi-dimensional consequences that can permanently impair their ability to operate effectively.

Impact Assessment of Financial Statement Fraud

| Impact Category | Measurement | Severity |

| Stock Value Loss | 12.3-20.6% average decline | High |

| Reputational Damage | Up to 100x direct financial loss | Severe |

| Employee Impact | 50% loss in cumulative wages | Severe |

| Legal Penalties | $750M+ in major cases | High |

| Bankruptcy Risk | 3x higher than non-fraud firms | High |

| Market Recovery | Years to decades, if ever | Variable |

| Customer Trust | Immediate and often permanent loss | Severe |

| Investment Access | Permanently impaired in many cases | High |

- The table above illustrates the catastrophic consequences that typically follow the discovery of fraudulent financial reporting. Stock value deterioration represents just the beginning of a complex cascade of negative outcomes that can ultimately lead to organizational failure. The reputational damage often exceeds direct financial losses by orders of magnitude, as stakeholders lose confidence in management’s integrity and the reliability of corporate disclosures.

- Employee impact proves particularly severe, with workers often experiencing substantial wage losses through reduced hours, eliminated positions, or complete job loss following fraud discovery. Legal penalties frequently reach hundreds of millions of dollars in major cases, while bankruptcy risk triples compared to companies without fraud incidents. Market recovery, when possible, typically requires years or decades of rebuilding trust and demonstrating renewed commitment to transparency and ethical conduct.

- Customer trust, once lost through fraudulent activities, proves extremely difficult to regain. Many organizations never fully recover their market position after serious fraud incidents come to light. Access to investment capital becomes permanently impaired in numerous cases as institutional investors implement strict exclusion policies for companies with histories of accounting fraud.

THE SECURITIES LITIGATION PROCESS

| Step | Description |

| 1. | A lead plaintiff files a lawsuit on behalf of similarly affected shareholders, detailing the allegations against the company. |

| 2. | Defendants typically file a motion to dismiss the class action lawsuits, arguing that the complaint lacks sufficient claims. |

| 3. | If the motion to dismiss is denied, both parties gather evidence, documents, emails, and witness testimonies. This phase of the litigation can be extensive. |

| 4. | Plaintiffs request that the court certify the litigation as a class action. The court assesses factors like the number of plaintiffs, commonality of claims, typicality of claims, and the adequacy of the proposed class representation. |

- |Once a class is certified, parties may file motions for summary judgment, requesting the court to rule in their favor without proceeding to trial. These motions argue that no genuine dispute exists regarding material facts, and the moving party is entitled to judgment as a matter of law.

- Summary judgment motions often focus on whether the evidence demonstrates scienter (intent to deceive) and loss causation. While trials are extremely rare in securities litigation, occurring in less than 1% of cases, the threat of trial often motivates settlement discussions. |

Case Studies: Successful Implementation of Enhanced Internal Controls

- Examining real-world examples of successful internal control enhancements provides valuable insights into the practical application and benefits of these systems. Here are a few case studies that highlight effective implementation:

-

- Company A: Faced with a history of financial discrepancies, Company A undertook a comprehensive review of its internal control systems. By implementing advanced data analytics and automated monitoring tools, the company significantly reduced errors and improved financial accuracy. As a result, it restored investor confidence and avoided potential legal issues.

- Organization B: This organization focused on strengthening its control environment by enhancing corporate governance practices. By establishing clear accountability mechanisms and fostering a culture of transparency, Organization B improved its compliance with regulatory requirements and reduced the risk of securities litigation.

- Enterprise C: Recognizing the need for continuous improvement, Enterprise C conducted regular internal control assessments. By identifying weaknesses and implementing corrective actions, the company maintained a strong control framework that supported its growth and financial stability.

- These case studies demonstrate the positive impact of proactive internal control enhancements on organizational resilience and legal compliance.

Tools and Technologies for Strengthening Internal Controls

- Leveraging the right tools and technologies is essential for strengthening financial internal controls. With advancements in technology, organizations now have access to innovative solutions that enhance control effectiveness and efficiency.

-

- Data Analytics: Advanced data analytics tools enable real-time monitoring and analysis of financial transactions. By identifying patterns and anomalies, these tools help detect potential fraud and errors promptly.

- Automated Workflow Systems: Implementing automated workflow systems streamlines approval and authorization processes. These systems ensure that all transactions adhere to established control procedures, reducing the risk of unauthorized actions.

- Blockchain Technology: Blockchain offers a secure and transparent platform for recording financial transactions. Its decentralized nature ensures data integrity and reduces the risk of tampering, making it a valuable tool for enhancing internal controls.

- Cloud-Based Solutions: Cloud-based platforms provide scalable and accessible solutions for managing internal controls. They offer real-time collaboration, data storage, and security features that enhance control processes.

- By adopting these technologies, you can enhance the effectiveness of your internal controls and ensure they remain relevant in an evolving financial landscape.

Preparing for 2025: Future Trends in Corporate Governance and Internal Controls

- As you look ahead to 2025, it is essential to consider emerging trends in corporate governance and internal controls that will shape the future of financial management. These trends include:

- Increased Focus on ESG: Environmental, Social, and Governance (ESG) factors are becoming integral to corporate governance. Organizations are expected to incorporate ESG considerations into their internal control frameworks to address stakeholder concerns and regulatory requirements.

- Cybersecurity and Data Privacy: With the growing reliance on digital technologies, cybersecurity and data privacy are critical areas of focus. Strengthening internal controls to protect against cyber threats and ensure data integrity will be paramount.

- AI and Machine Learning: The adoption of AI and machine learning technologies will revolutionize internal controls. These technologies can enhance risk assessment, automate processes, and provide predictive insights to improve decision-making.

- Regulatory Changes: Staying abreast of evolving regulations and compliance requirements is crucial. Organizations must adapt their internal control systems to align with new standards and ensure ongoing compliance.

- By preparing for these trends, you can position your organization to meet future challenges and maintain robust internal controls that support sustainable growth.

Conclusion: Building a Strong Defense Against Securities Litigation

- In conclusion, enhancing financial internal controls is your best defense against securities litigation in 2025 and beyond. By understanding the importance of internal controls, addressing common weaknesses, and implementing best practices, you can safeguard your organization against potential legal challenges.

- Investing in the right tools and technologies, fostering a culture of compliance, and staying informed about future trends in corporate governance will further strengthen your internal control framework. By doing so, you not only protect your organization from financial misstatements and fraud but also build trust with stakeholders and secure long-term success.