Introduction to Documentation and Internal Controls

- Documentation of internal controls creates a roadmap that outlines an organization’s policies, procedures, and mechanisms to minimize risk, ensure financial reliability, promote operational efficiency, and maintain compliance with laws and regulations.

- This detailed record-keeping provides transparency, facilitates audits by acting as evidence of control performance, supports consistency in operations, and helps preserve institutional knowledge during staff changes.

- Common documentation methods include flowcharts, narratives, policy and procedure manuals, and risk/control matrices.

- Clarity and Consistency: Documentation ensures that internal control procedures are clearly understood and consistently applied across the organization, which is crucial for preventing errors and fraud.

- Accountability: It establishes clear lines of responsibility and accountability, ensuring that personnel understand their roles in the control process.

- Risk Mitigation: By clearly defining risks and the corresponding control activities, documentation helps organizations proactively manage and reduce financial, operational, and other business risks.

- Compliance: Documented controls provide evidence to regulators and auditors that the organization is adhering to relevant laws and industry standards.

- Audit Readiness: Comprehensive documentation enables auditors to assess the effectiveness of internal controls, making the audit process smoother and more efficient.

- Knowledge Preservation: Documentation serves as a repository for institutional knowledge, ensuring that critical information and procedures are not lost when employees leave.

- Flowcharts: Visual representations of processes and their control points.

- Policies and Procedures: Formal documents outlining organizational standards and step-by-step instructions for specific tasks.

- Risk and Control Matrices: Tools that map identified risks to the specific controls designed to mitigate them.

- Internal Control Questionnaires: Questionnaires used to assess the design and operational effectiveness of controls.

- Flowcharts: Visual representations of processes and their control points.

- Define Scope: Identify key processes and areas that materially affect financial reporting or other critical objectives.

- Map Processes: Document the input, activities, and outputs of each subprocess.

- Identify Risks: For each subprocess, identify potential process risks and control gaps.

- Document Controls: Record the specific policies and procedures that are in place to address identified risks.

- Maintain Version Control: Use clear formats and version control to ensure that documentation is kept up-to-date and accurate.

- Centralize and Secure: Store documents in a centralized, secure location with stringent access controls to protect sensitive information.

- Train Staff: Ensure that all relevant personnel understand the documented controls and their roles in maintaining them.

- Conduct Regular Reviews: Periodically review and update documentation to maintain its accuracy and relevance as the organization evolves.

The relationship between documentation and internal controls

- Documentation formalizes controls: It defines and communicates internal control policies and procedures to all employees, establishing a clear framework for guidance and compliance.

- Controls require evidence: Documentation creates the necessary audit trail to prove that controls have been followed. An auditor reviewing a bank reconciliation, for example, needs to see the signed document as evidence that the detective control was performed.

- It ensures consistency: Proper documentation standardizes practices and procedures, minimizing variances and human error.

- It preserves knowledge: Documenting controls preserves institutional knowledge, which is critical for business continuity during staff turnover.

- It aids in monitoring: Written procedures provide a baseline for monitoring control effectiveness over time and identifying weaknesses.

Key types of internal control documentation

- Policies:Broad statements of intent (e.g., “The company requires segregation of duties for all cash disbursements”).

- Procedures: The detailed, step-by-step instructions for how to carry out a specific task (e.g., “Step 1: Obtain an invoice. Step 2: Compare the invoice to the purchase order…”).

Process flowcharts and narratives

- Flowcharts: Diagrams that visually represent each step and decision point in a process.

- Narratives: Written descriptions of a process from beginning to end.

Organizational charts

Evidence of control performance

- Authorization forms: A manager’s signature or a system-enforced approval showing that a transaction was authorized.

- Reconciliations: A bank reconciliation report or a comparison of inventory counts to system records.

- Exception reports: A log of control failures and the resulting remedial actions.

- Testing documentation: A record of control testing, including the testing frequency, methods, and results.

The five components of the COSO framework

- Control Environment: The “tone at the top” that promotes integrity and ethical values. Documentation includes a code of conduct, human resource policies, and clear employee roles and responsibilities.

- Risk Assessment: The process of identifying and analyzing relevant risks. Documentation includes risk assessment reports and risk tolerance statements.

- Control Activities: The policies and procedures that mitigate risks. Documentation includes detailed manuals, process flowcharts, and evidence of execution.

- Information and Communication: The system that ensures information is captured and exchanged effectively. Documentation includes all manuals, reports, and communication logs.

- Monitoring Activities: The ongoing and separate evaluations of the internal control system. Documentation includes audit findings, management review reports, and documentation of remediation efforts.

Enhanced Legal Framework and the Fraud on the Market Theory

The legal framework governing securities class actions has evolved significantly, particularly regarding the Fraud on the Market Theory, which serves as a cornerstone for modern securities litigation. This theory, established in Basic Inc. v. Levinson (1988), allows investors to rely on market efficiency rather than proving individual reliance on specific misstatements.

Recent Developments in Fraud on the Market Theory

Key 2024 Judicial Changes:

- Enhanced Materiality Standards: Courts now require more rigorous proof that alleged misstatements actually moved market prices

- Stricter Market Efficiency Tests: Plaintiffs must demonstrate that the relevant market was truly efficient during the class period

- Heightened Causation Requirements: Recent decisions demand clearer connections between corporate disclosures and stock price movements

- The theory operates on several fundamental assumptions that have been refined through recent case law.

Core Elements of Market Efficiency:

- Information Transmission: Material information must flow quickly to market participants

- Price Incorporation: Stock prices must reflect available public information within reasonable timeframes

Trading Volume Adequacy: Sufficient trading activity to support price discovery mechanisms - Market Maker Participation: Active institutional involvement in price-setting processes

Strengthened Documentation Requirements

Recent developments have elevated the importance of comprehensive internal controls and documentation practices. Companies now face increased scrutiny regarding:

Critical Documentation Areas:

- Risk Assessment Protocols: Detailed records of how material risks are identified and communicated

- Disclosure Committee Minutes: Comprehensive documentation of materiality determinations and disclosure decisions

- Internal Audit Reports: Regular assessments of financial reporting accuracy and control effectiveness Management Certifications: Enhanced documentation supporting CEO and CFO certifications under the Sarbanes-Oxley Act

Practical Implications for Corporate Defense

The evolving legal landscape creates both challenges and opportunities for corporate defendants. Proactive documentation strategies can significantly impact litigation outcomes:

Defensive Documentation Best Practices:

- Real-Time Risk Monitoring: Implement systems that capture risk assessments as they occur, not retroactively

- Cross-Functional Communication Records: Document how material information flows between departments

- External Advisor Consultations: Maintain detailed records of legal and accounting advice received

- Board-Level Oversight Documentation: Comprehensive minutes showing director engagement with material issues

Market Impact Analysis and Economic Evidence

Recent court decisions emphasize the critical role of economic analysis in securities class actions. Plaintiffs must now provide more sophisticated evidence of market impact:

Enhanced Economic Requirements:

- Event Study Analysis: Statistical proof that alleged misstatements caused measurable stock price movements Market Model Validation: Demonstration that chosen economic models accurately reflect market conditions Alternative Causation Analysis: Examination of other factors that might explain price movements

- Damages Calculation Precision: More rigorous methodologies for calculating investor losses

Strategic Considerations for 2025

As we advance into 2025, several trends are reshaping securities class action defense strategies:

Emerging Defense Strategies:

- Preemptive Disclosure Programs: Implementing robust disclosure frameworks before issues arise

- Technology-Enhanced Monitoring: Using AI and data analytics to identify potential disclosure issues early

- Stakeholder Communication Plans: Developing clear protocols for communicating with investors during crises

- Regulatory Relationship Management: Building strong relationships with SEC staff and other regulators

The intersection of documentation excellence and legal strategy has never been more critical. Companies that invest in comprehensive internal controls and documentation practices position themselves advantageously against securities class action challenges.

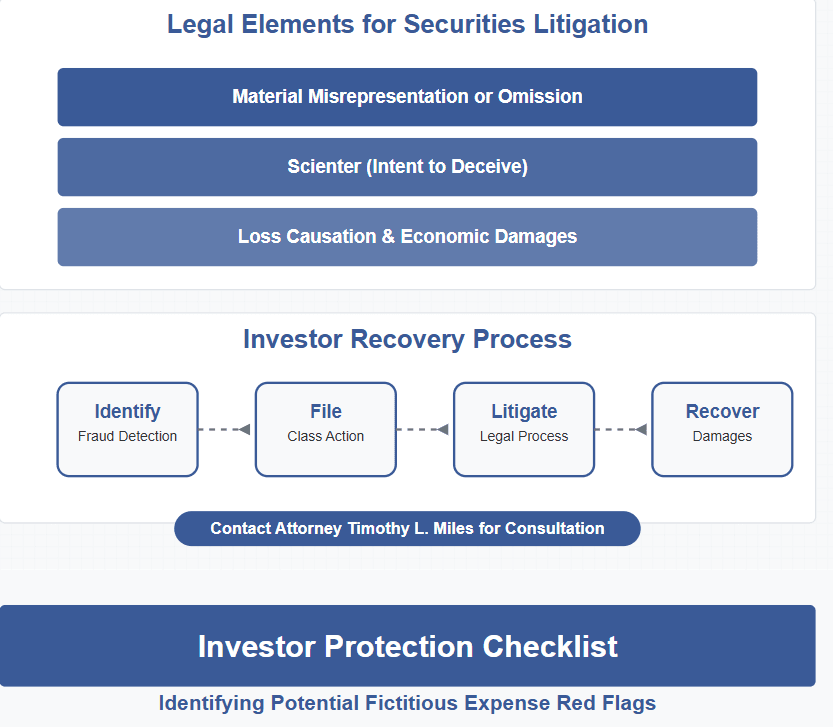

Understanding Securities Class Actions

- Securities class actions represent a significant legal challenge for corporations, often arising when investors claim that a company has engaged in fraudulent activities or has failed to disclose critical financial information, resulting in investment losses.

- Securities litigation can lead to substantial financial penalties, reputational damage, and operational disruptions. As we move into 2025, the complexity and frequency of these actions continue to grow, driven by an increasingly vigilant regulatory environment and sophisticated plaintiffs’ bar eager to pursue any perceived transgression.

- Therefore, understanding the nuances of securities class actions is paramount for any organization seeking to protect itself from securities litigation.

- The anatomy of a securities class action typically begins with an allegation that a company has violated securities laws by making false or misleading statements, or by omitting significant facts that could affect an investor’s decision-making process.

- Plaintiffs, often represented by a class of shareholders, file these claims in federal court, seeking restitution for the financial harm they have allegedly suffered.

The High Stakes of Securities Litigation

- The stakes are particularly high because these cases can result in settlements that reach into the hundreds of millions of dollars, not to mention the legal costs and resources required to mount a defense.

- Moreover, securities class actions can be precipitated by a variety of catalysts, including financial restatements, regulatory bodies investigations, or adverse market reactions to company disclosures.

- The legal landscape is further complicated by evolving judicial standards regarding what constitutes actionable fraud or misrepresentation, making it essential for companies to stay abreast of legal precedents and shifting expectations.

- This section sets the stage for a deeper exploration of how robust documentation and internal controls can serve as a bulwark against such legal challenges.

The Importance of Documentation in Legal Defense

- Documentation serves as the cornerstone of a robust legal defense in securities class actions.

- It is the primary means by which a company can substantiate the accuracy and transparency of its financial disclosures.

- Comprehensive and well-organized documentation can demonstrate that a company acted in good faith and adhered to all regulatory requirements, thereby reducing the risk of adverse judgments in court.

- In an era where plaintiffs meticulously scrutinize every statement and disclosure, the importance of maintaining meticulous records cannot be overstated.

- Effective documentation is not just about recording past transactions; it involves creating a detailed narrative that reflects the decision-making processes and risk assessments undertaken by company executives.

- This includes maintaining minutes of board meetings, records of communication with investors, and internal memos that document the rationale behind key financial decisions.

Creat a Clear Paper Trail

- By establishing a clear and coherent paper trail, companies can more effectively counter allegations of fraud or misrepresentation by showing that they operated with integrity and transparency.

- Furthermore, the digital transformation of business processes has introduced new challenges and opportunities for documentation.

- Companies must now manage vast amounts of data generated by digital communications, transactions, and operations.

- Implementing advanced document management systems that ensure data integrity, confidentiality, and accessibility is crucial.

- These systems not only facilitate compliance with regulatory requirements but also enhance a company’s ability to respond swiftly and effectively to legal inquiries and proceedings.

Key Internal Controls to Implement

- Internal controls are the mechanisms that ensure the accuracy and reliability of financial reporting, safeguard assets, and promote operational efficiency.

- These controls play a vital role in preventing and detecting errors or fraudulent activities, thereby reducing the likelihood of securities class actions.

- A robust internal control framework typically encompasses a range of policies and procedures designed to address various risk areas, from financial reporting to compliance and information security.

- One of the most critical internal controls is the segregation of duties, which involves dividing responsibilities among different employees to reduce the risk of error or fraud.

- By ensuring that no single individual has control over all aspects of a financial transaction, companies can prevent unauthorized access to assets and ensure that checks and balances are in place. This control is particularly important in areas such as cash handling, procurement, and financial reporting.

- In addition to segregation of duties, companies should implement comprehensive risk assessment procedures to identify and evaluate potential threats to their financial operations.

- This involves regularly reviewing internal and external risk factors, such as changes in market conditions, regulatory requirements, and operational processes.

- By proactively identifying and mitigating risks, companies can strengthen their internal control environment and reduce the likelihood of facing securities class actions.

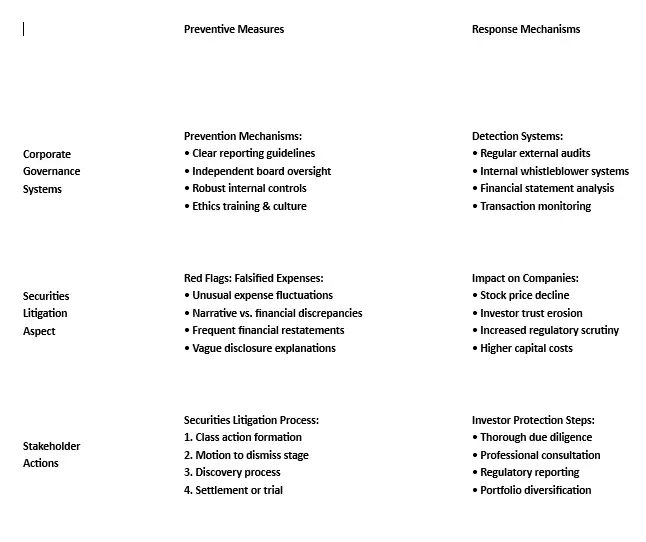

PREVENTATIVE MEASURES AND RESPONSE MECHANISMS

Best Practices for Effective Documentation

- To maximize the effectiveness of documentation in legal defense, companies must adopt best practices that ensure consistency, accuracy, and accessibility.

- One fundamental practice is the establishment of a centralized document management system that allows for the secure storage and retrieval of records.

- This system should be designed to accommodate both physical and digital documents, with robust search and retrieval capabilities to facilitate quick access to relevant information.

- Another key practice is the development of comprehensive documentation policies and procedures that outline the types of records to be maintained, the retention periods, and the responsibilities of employees in managing and preserving documents.

- These policies should be regularly reviewed and updated to reflect changes in regulatory requirements and business practices.

- Providing training and guidance to employees on these policies can enhance compliance and ensure that documentation practices are consistently followed across the organization.

- Moreover, companies should implement regular audits and reviews of their documentation practices to identify areas for improvement and ensure adherence to established policies.

- These audits can help uncover gaps or deficiencies in record-keeping, allowing companies to take corrective actions before potential issues escalate into legal challenges.

- By fostering a culture of accountability and continuous improvement, companies can strengthen their documentation practices and enhance their ability to defend against securities class actions.

Risk Assessment and Management Strategies

- Effective risk assessment and management are integral components of a company’s defense strategy against securities class actions.

- By systematically identifying, evaluating, and mitigating risks, companies can reduce their exposure to legal challenges and enhance their overall resilience.

- The risk management process should be an ongoing effort that involves collaboration across all levels of the organization, from executive leadership to frontline employees.

- A comprehensive risk assessment begins with the identification of potential risks, including those related to financial reporting, compliance, and operational processes.

Consider Risk Factors and Regulatory Requirements

- Companies should also consider external risk factors, such as changes in regulatory environments, economic conditions, and industry trends.

- Once risks have been identified, they should be evaluated based on their likelihood and potential impact on the organization.

- This evaluation enables companies to prioritize risks and allocate resources effectively to mitigate them.

- Risk management strategies should be tailored to address the specific risks identified during the assessment process.

- These strategies may include implementing additional internal controls, enhancing employee training programs, or investing in technology solutions that improve data security and accuracy.

- By adopting a proactive and strategic approach to risk management, companies can minimize their vulnerability to securities class actions and ensure long-term success.

The Role of Audits in Strengthening Internal Controls

- Audits play a crucial role in strengthening internal controls and enhancing a company’s ability to deflect securities class actions.

- By providing an independent and objective assessment of a company’s financial reporting and internal control environment, audits can identify weaknesses and areas for improvement.

- Regular audits, whether conducted internally or by external auditors, help ensure that internal controls are functioning effectively and that financial statements are accurate and reliable.

- Internal audits are an essential component of a company’s risk management strategy. They involve a systematic review of financial operations, compliance with regulatory requirements, and the effectiveness of internal controls.

- By identifying potential issues before they escalate, internal audits can help companies take corrective actions and prevent future problems.

- Furthermore, internal audits provide valuable insights into the company’s operations, enabling management to make informed decisions that enhance overall performance.

- External audits, on the other hand, provide an independent verification of a company’s financial statements and internal controls.

- These audits are typically conducted by certified public accountants who adhere to strict professional standards.

- By obtaining an unqualified audit opinion, companies can demonstrate to investors and regulators that their financial reporting is accurate and that their internal controls are robust.

- This can enhance investor confidence and reduce the likelihood of securities class actions.

Case Studies: Successful Defenses Against Class Actions

- Examining case studies of companies that have successfully defended against securities class actions can provide valuable insights into effective strategies and best practices.

- One notable example is the defense mounted by a major technology firm accused of misleading investors about its financial performance.

- By presenting comprehensive documentation and demonstrating the effectiveness of its internal controls, the company was able to refute the allegations and secure a favorable outcome in court.

- In another case, a pharmaceutical company faced allegations of failing to disclose critical information about a drug’s safety profile.

- The company’s defense strategy hinged on its robust risk management framework, which included thorough documentation of clinical trial data and communications with regulatory authorities.

- By demonstrating that it had acted in accordance with industry standards and regulatory requirements, the company was able to successfully defend against the class action and avoid significant financial penalties.

- These case studies highlight the importance of maintaining accurate documentation, implementing effective internal controls, and adopting proactive risk management strategies.

- By learning from these examples, companies can enhance their own compliance frameworks and improve their ability to defend against securities class actions.

- Moreover, these cases underscore the value of a strong legal defense team that can effectively advocate for the company’s interests in court.

Regulatory Compliance and Its Impact on Internal Controls

- Regulatory compliance is a critical factor influencing the design and effectiveness of internal controls.

- As regulatory requirements continue to evolve, companies must remain vigilant in ensuring that their internal controls are aligned with applicable laws and standards.

- Failure to comply with regulatory requirements can result in significant legal and financial consequences, including securities class actions.

- To maintain compliance, companies should establish comprehensive compliance programs that address all relevant regulatory requirements.

- These programs should include policies and procedures for monitoring compliance, conducting regular audits, and providing training to employees.

- By fostering a culture of compliance and accountability, companies can reduce their risk of regulatory violations and enhance the effectiveness of their internal controls.

- In addition to regulatory compliance, companies should be aware of emerging trends and developments in the legal and regulatory landscape.

- This includes staying informed about changes in securities laws, accounting standards, and industry-specific regulations.

- By proactively adapting to these changes, companies can ensure that their internal controls remain effective and that they are well-prepared to address potential legal challenges.

Future Trends in Securities Litigation and Internal Controls

- As we look to the future, several trends are likely to shape the landscape of securities litigation and internal controls.

- One notable trend is the increasing use of technology and data analytics in both securities litigation and internal controls.

- Companies are leveraging advanced analytics to identify potential risks, monitor compliance, and enhance the accuracy of financial reporting.

- This trend is likely to continue as technology becomes increasingly integrated into business processes.

- Another emerging trend is the growing focus on environmental, social, and governance (ESG) factors in securities litigation.

- Investors and regulators are placing greater emphasis on ESG disclosures, and companies are facing increased scrutiny regarding their ESG practices.

- As a result, companies must ensure that their internal controls address ESG-related risks and that their disclosures are accurate and transparent.

- Finally, the globalization of financial markets is likely to influence securities litigation and internal controls.

- As companies operate in multiple jurisdictions, they must navigate a complex web of regulatory requirements and legal standards.

- This requires a robust compliance framework that can adapt to different regulatory environments and mitigate cross-border risks.

- By staying ahead of these trends, companies can enhance their internal controls and reduce their exposure to securities litigation.

Conclusion: Building a Robust Defense Strategy

- Building a robust defense strategy against securities class actions requires a comprehensive approach that integrates effective documentation, strong internal controls, and proactive risk management.

- By maintaining accurate and transparent records, companies can substantiate their financial disclosures and demonstrate compliance with regulatory requirements.

- mplementing robust internal controls and conducting regular audits can help prevent and detect errors or fraudulent activities, reducing the likelihood of legal challenges.

- Furthermore, companies must adopt proactive risk management strategies that identify and mitigate potential risks.

- This includes staying informed about regulatory changes, emerging trends, and best practices in compliance and internal controls.

- By fostering a culture of accountability and continuous improvement, companies can enhance their ability to defend against securities class actions and ensure long-term success.

- In an increasingly complex and dynamic financial landscape, companies must remain vigilant and adaptable.

- By embracing the principles outlined in this guide, organizations can build a strong defense strategy that protects their interests, enhances investor confidence, and supports sustainable growth.

- As we move into 2026 and beyond, the importance of documentation and internal controls in deflecting securities class actions will only continue to grow.

- By prioritizing these elements, companies can navigate the challenges ahead and thrive in a rapidly changing environment.