Introduction to Asset Misappropriation and Accounting Fraud

- Asset misappropriation and accounting fraud are intertwined complex schemes that cause devastation to companies and their shareholders.

- Asset misappropriation, a term that may sound technical, is essentially the theft or misuse of an organization’s resources.

- It represents the most common type of occupational fraud, characterized by employees or executives embezzling company funds, manipulating expense reports, or siphoning off assets for personal gain.

- Despite its prevalence, asset misappropriation is often challenging to detect, especially in large organizations where assets are abundant and oversight can be spread thin.

- The subtlety with which these frauds are carried out makes them particularly insidious, as they often go unnoticed until significant damage has occurred.

- In essence, asset misappropriation can be seen as a breach of trust.

- Employees or executives who engage in such activities exploit the confidence placed in them to manage and protect the company’s resources.

Damages Go Beyond Money and can Ruin a Company’s Reputation

- This betrayal not only results in financial loss but also damages the organizational culture and morale.

- When colleagues who were trusted are revealed to be fraudsters, it creates an atmosphere of suspicion and undermines teamwork and cooperation, which are crucial for business success.

- Moreover, the financial implications of asset misappropriation extend beyond the immediate loss of assets. Companies must invest considerable resources in investigations, legal proceedings, and implementing corrective measures.

- These activities, while necessary, can divert attention and resources from core business operations, impacting overall productivity and profitability.

- Thus, understanding the nature and consequences of asset misappropriation is the first step in safeguarding an organization against this pervasive threat.

The Intersection of Asset Misappropriation and Accounting Fraud

Asset Misappropriation and Accounting Fraud often intertwine in complex schemes that can devastate organizations and their stakeholders.

When executives manipulate financial records to conceal stolen assets, they create a dual threat that extends far beyond simple theft.

Accounting fraud typically involves the deliberate falsification of financial statements to hide misappropriated assets, creating inflated revenue figures or understated expenses that mislead investors about the company’s true financial position.

These sophisticated schemes frequently involve multiple layers of deception.

For instance, executives might establish shell companies to funnel corporate funds, then manipulate accounting records to disguise these transactions as legitimate business expenses.

Such activities not only constitute asset misappropriation but also trigger serious regulatory compliance violations under federal securities laws.

The consequences of these intertwined frauds are particularly severe because they directly impact investor confidence and market integrity.

When companies fail to maintain accurate financial records due to asset misappropriation schemes, they violate fundamental principles of corporate governance that require transparency and accountability to shareholders.

Securities Litigation: The Legal Reckoning

- When asset misappropriation schemes involving accounting fraud come to light, they frequently trigger securities litigation that can span years and cost millions in legal fees and settlements.

- Securities Class Action Lawsuits represent a powerful mechanism for investors to seek compensation when corporate misconduct results in financial losses.

- These legal proceedings typically arise when:

- Material misstatements in financial reports conceal asset misappropriation schemes

- Omissions of material facts prevent investors from understanding the true extent of corporate theft

- Insider trading occurs as executives profit from knowledge of undisclosed fraud

- Market manipulation results from artificially inflated financial performance

- The legal framework governing these cases requires plaintiffs to demonstrate that asset misappropriation schemes directly caused their investment losses.

- This connection between corporate theft and investor harm forms the foundation of successful securities litigation.

Corporate Scandals and Their Lasting Impact

- History provides numerous examples of how asset misappropriation has evolved into major corporate scandals that reshape entire industries.

- The Enron collapse, WorldCom fraud, and more recent cases like Wells Fargo’s fake accounts scandal demonstrate how seemingly isolated instances of asset misappropriation can metastasize into company-wide corruption.

Common Characteristicsof Scandals

- These scandals share common characteristics:

- Systematic compliance failures that allow fraud to flourish unchecked

- Weak internal controls that fail to detect ongoing asset misappropriation

- Cultural problems that prioritize short-term profits over ethical behavior

- Board oversight failures that enable executive misconduct

- The ripple effects of these scandals extend far beyond the companies involved, often triggering industry-wide regulatory reforms and increased scrutiny from federal agencies.

Compliance Failures: The Root of Systemic Problems

- Compliance failures represent perhaps the most dangerous aspect of asset misappropriation schemes because they indicate systemic weaknesses in corporate governance structures.

- When companies fail to implement adequate internal controls, they create environments where fraud can flourish undetected for extended periods.

Key Compliance Failures

- Key compliance failures that enable asset misappropriation include:

- Inadequate segregation of duties that allows individuals to both authorize and execute financial transactions Weak monitoring systems that fail to detect unusual patterns in financial activity

- Insufficient background checks for employees in positions of financial responsibility

- Poor documentation requirements that make it difficult to trace asset movements

- These failures often compound over time, creating increasingly sophisticated fraud schemes that can ultimately trigger securities litigation and regulatory enforcement actions.

Financial Impacts and Market Consequences

- The financial impacts of asset misappropriation extend far beyond the immediate theft of corporate assets.

- When these schemes involve accounting fraud, they can artificially inflate stock prices, creating market bubbles that eventually burst when the truth emerges.

- The resulting corrective disclosures often trigger dramatic stock price declines that harm innocent investors who relied on fraudulent financial statements.

The True Cost of Asset Misappropriation

- Economic experts analyzing these cases typically find that the true cost of asset misappropriation includes:

- Direct asset losses from theft and embezzlement

- Legal and investigation costs that can reach tens of millions of dollars

- Regulatory fines and penalties imposed by federal agencies

- Settlement payments to resolve securities class action lawsuits

- Reputational damage that affects future business relationships and market valuation

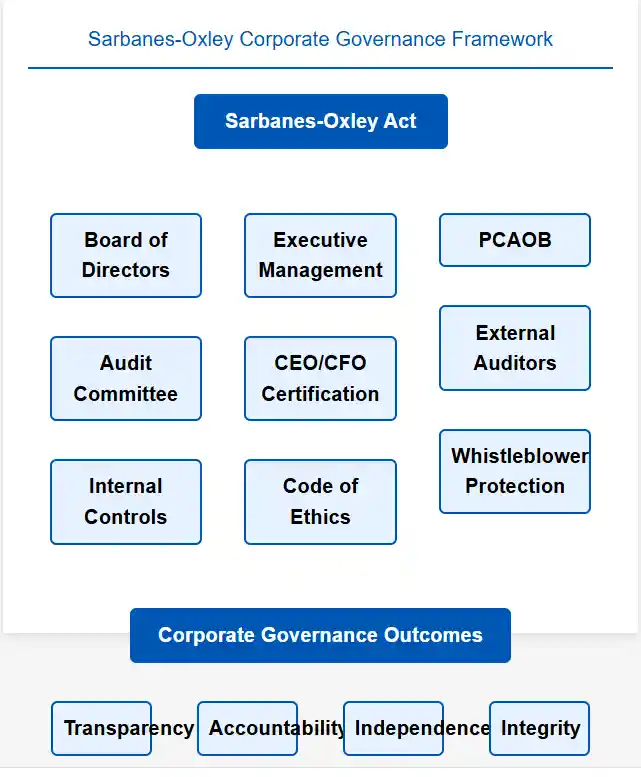

Regulatory Changes and Enhanced Oversight

- In response to major corporate scandals involving asset misappropriation, regulatory agencies have implemented increasingly stringent oversight requirements.

- The Sarbanes-Oxley Act of 2002, Dodd-Frank Wall Street Reform and Consumer Protection Act, and other federal legislation have created new compliance obligations designed to prevent and detect corporate fraud.

- These regulatory changes include:

- Enhanced internal control requirements that mandate regular testing and certification

- Whistleblower protection programs that encourage reporting of suspected fraud

- Increased penalties for executives who engage in securities fraud

- Expanded disclosure requirements that provide investors with more detailed information about corporate risks

- Companies that fail to adapt to these evolving regulatory requirements face increased exposure to both enforcement actions and private securities litigation.

- The intricate relationship between accounting fraud and securities litigation represents one of the most significant challenges facing modern capital markets.

- When corporations manipulate their financial statements, they set in motion a cascade of legal consequences that can devastate investor confidence and trigger extensive litigation proceedings.

The Securities Litigation Response Mechanism

- Securities litigation serves as the primary legal remedy available to investors who have suffered financial harm due to corporate deception.

- This sophisticated legal framework operates on multiple levels, providing both individual and collective remedies through various procedural mechanisms.

- Securities class action lawsuits represent the most powerful tool in this arsenal, allowing groups of similarly situated investors to pool their resources and pursue claims against corporations, executives, and auditors who participated in or facilitated fraudulent schemes.

- These collective actions level the playing field between individual investors and well-funded corporate defendants.

The Litigation Process

- The litigation process typically unfolds through several critical phases:

- Discovery of fraud through whistleblowers, regulatory investigations, or market anomalies

- Corrective disclosure that reveals the true extent of the deceptive practices

- Stock price decline as markets react to the revelation of fraud

- Class certification to establish the group of affected investors

- Settlement negotiations or trial proceedings to determine damages

Regulatory Compliance and Corporate Governance Failures

- Regulatory compliance failures often serve as both a catalyst for accounting fraud and a basis for securities litigation.

- When companies fail to maintain adequate internal controls or ignore established accounting standards, they create environments where fraudulent activities can flourish unchecked.

- Corporate governance breakdowns frequently accompany these compliance failures, as boards of directors and audit committees fail in their oversight responsibilities.

- The interconnected nature of these failures means that securities litigation often targets multiple parties within the corporate structure, from individual executives to independent auditors who failed to detect or report suspicious activities.

Modeern Corporate Compliance Frameworks

- Modern regulatory frameworks, including the Sarbanes-Oxley Act and Dodd-Frank provisions, have strengthened the tools available to prosecutors and civil litigants pursuing accountability for these governance failures.

- However, compliance failures continue to plague corporations across industries, particularly in sectors experiencing rapid technological change or regulatory evolution.

The Anatomy of Corporate Scandals

- Corporate scandals involving accounting fraud follow predictable patterns that securities litigation has helped to expose and address.

- These scandals typically begin with pressure to meet earnings expectations, leading to increasingly aggressive accounting practices that eventually cross the line into outright fraud.

Common Characteristics of Scandals

- The most devastating scandals share common characteristics:

- Management override of internal controls to facilitate fraudulent reporting

- Auditor complicity or negligence in failing to detect obvious red flags

- Board dysfunction that prevents effective oversight of financial reporting

- Regulatory capture that delays detection and enforcement actions

- When these scandals emerge, they trigger not only immediate securities litigation but also broader regulatory reforms designed to prevent similar future occurrences.

- The cyclical nature of this process demonstrates the ongoing tension between market innovation and regulatory oversight.

Legal Precedents Shaping Future Litigation

- Legal precedents established through decades of securities litigation continue to evolve, providing increasingly sophisticated tools for investors seeking redress for accounting fraud.

- Recent court decisions have clarified standards for proving materiality, loss causation, and scienter in complex fraud cases.

- These precedents have particular significance for cases involving:

- Emerging technologies where traditional accounting standards may be inadequate

- Cross-border transactions that complicate jurisdictional and enforcement issues

- Complex financial instruments that obscure the true nature of corporate obligations

- Regulatory gray areas where compliance standards remain unclear

The Deterrent Effect and Market Integrity

- The relationship between accounting fraud and securities litigation ultimately serves a broader purpose in maintaining market integrity.

- By providing meaningful consequences for fraudulent behavior, securities litigation creates powerful incentives for corporate transparency and accountability.

- This deterrent effect operates on multiple levels:

- Individual accountability through personal liability for executives and professionals

- Corporate consequences including financial penalties and reputational damage

- Systemic improvements in internal controls and governance practices

- Regulatory evolution that addresses emerging fraud schemes

Oversight and Accountability

- The ongoing evolution of this relationship reflects the dynamic nature of capital markets and the persistent challenge of balancing innovation with investor protection.

- As accounting practices become increasingly complex and global, securities litigation continues to adapt, providing essential oversight and accountability mechanisms.

- The interconnected nature of accounting fraud and securities litigation underscores the critical importance of maintaining robust financial reporting standards and effective legal remedies.

- For investors, understanding these relationships provides essential insight into both the risks they face and the protections available when corporate misconduct occurs.

Understanding Asset Misappropriation: The Gateway to Corporate Scandals and Securities Litigation

- Asset misappropriation represents one of the most pervasive forms of accounting fraud plaguing modern corporations, serving as a catalyst for corporate scandals that ultimately trigger securities class action lawsuits and expose critical compliance failures.

- When employees or executives systematically steal or misuse company resources, they create a domino effect that can devastate shareholder value and undermine corporate governance structures designed to protect investor interests.

The Expanding Landscape of Asset Misappropriation

- Asset misappropriation and accounting fraud manifest in increasingly sophisticated forms, each presenting unique challenges for detection and prevention.

- Understanding these common types becomes crucial for organizations seeking to maintain regulatory compliance and avoid the devastating consequences of corporate scandals.

Cash Theft: The Foundation of Financial Deception

- Cash theft remains the most direct and immediately damaging form of asset misappropriation.

- This category extends far beyond simple skimming operations, encompassing complex schemes that manipulate financial reporting systems.

- When employees steal cash before it enters the company’s official records, they create discrepancies that can cascade into broader accounting fraud schemes.

Sophisticated Cash Theft Schemes

- Sophisticated cash theft operations often involve multiple participants who manipulate point-of-sale systems, alter deposit records, or create fictitious refunds.

- These schemes become particularly dangerous when they involve senior management, as executives possess the authority to override internal controls and manipulate financial statements to conceal their activities.

- Such executive-level misconduct frequently triggers securities litigation when investors discover that reported financial performance was artificially inflated through concealed theft.

The Impact Beyond Financial Losses

The impact extends beyond immediate financial losses.

When cash theft schemes are discovered, they often reveal systemic compliance failures that expose organizations to regulatory scrutiny and potential securities class action lawsuits.

Investors who purchased shares based on fraudulent financial statements may seek compensation for their losses, arguing that the company’s failure to prevent or detect the theft constituted a material omission in its public disclosures.

Fraudulent Disbursements: Weaponizing Corporate Payment Systems

- Fraudulent disbursements represent a more sophisticated evolution of asset misappropriation, leveraging legitimate business processes to facilitate theft.

- These schemes exploit the trust inherent in corporate payment systems, creating unauthorized transactions that appear legitimate within normal business operations.

Check Tampering Schemes

- Check tampering schemes involve employees who either forge company checks or alter legitimate checks to redirect funds to their personal accounts.

- More advanced operations create entirely fictitious vendors, complete with false documentation and bank accounts, allowing perpetrators to submit fraudulent invoices and receive payments for goods or services never provided.

Expense Reimbursement Fraud

- Expense reimbursement fraud has evolved significantly in the digital age, with employees submitting fabricated receipts, inflating legitimate expenses, or claiming reimbursement for personal expenditures.

- These schemes often involve collusion between employees and external parties, creating networks of fraudulent activity that can persist for years before detection.

Implications of Corporate Governance

- The corporate governance implications of fraudulent disbursements are particularly severe because they demonstrate failures in multiple control systems simultaneously.

- When these schemes are discovered, they often trigger comprehensive investigations that reveal broader compliance failures and expose organizations to significant securities litigation risk.

- Shareholders may argue that the company’s inability to prevent such systematic abuse of its payment systems constituted a material weakness in internal controls that should have been disclosed.

Inventory Theft: Beyond Physical Asset Loss

- Inventory theft encompasses both physical theft of goods and sophisticated manipulation of inventory records to conceal missing assets.

- This form of asset misappropriation is particularly damaging because it affects multiple aspects of business operations while creating opportunities for extensive accounting fraud.

Pysical Inventory Theft

- Physical inventory theft can range from employees stealing small quantities of goods for personal use to organized schemes involving external parties who facilitate the removal and sale of substantial quantities of merchandise.

- These operations often involve warehouse personnel, shipping clerks, or security staff who possess access to inventory storage areas and transportation systems.

Inventory Record Manipulation

- Inventory record manipulation represents a more complex form of theft that involves altering computer systems to conceal missing inventory.

- Perpetrators may adjust inventory counts, create fictitious sales transactions, or manipulate cost of goods sold calculations to hide their activities.

- These schemes can persist for extended periods because they exploit the natural fluctuations in inventory levels that occur during normal business operations.

Implications of Regulatory Compliance

- The regulatory compliance implications of inventory theft extend beyond immediate financial losses.

- Companies must maintain accurate inventory records for tax purposes, financial reporting, and regulatory filings.

- When inventory theft schemes are discovered, they often reveal that reported financial results were materially misstated, potentially triggering securities class action lawsuits from investors who relied on fraudulent financial statements.

The Securities Litigation Connection

- Asset misappropriation and accounting fraud schemes frequently evolve into securities litigation when their discovery reveals that public companies provided materially false or misleading information to investors.

- The connection between internal theft and external investor harm creates a complex legal landscape where corporate scandals trigger multiple forms of legal action.

- When asset misappropriation schemes are discovered, companies face immediate pressure to assess the full scope of the fraud and determine whether their previous financial statements require restatement.

- This process often reveals that the theft was more extensive than initially apparent, leading to significant adjustments to reported revenues, expenses, or asset values.

Managements Failure to Dedect the Theft

- Securities class action lawsuits typically emerge when investors argue that the company’s failure to detect or prevent the asset misappropriation constituted a breach of fiduciary duty or a violation of securities laws.

- Plaintiffs may contend that management knew or should have known about the theft and failed to implement adequate internal controls or provide appropriate disclosures to investors.

- The regulatory response to asset misappropriation cases has intensified significantly, with agencies demanding more comprehensive disclosure of internal control weaknesses and more rigorous assessment of fraud risks.

- Companies that experience significant asset misappropriation often face extended regulatory scrutiny that can persist long after the immediate crisis is resolved.

Corporate Governance and Compliance Implications

- Corporate governance failures often create the conditions that enable asset misappropriation schemes to flourish.

- When boards of directors fail to establish appropriate oversight mechanisms or when management overrides established controls, they create opportunities for fraud that can ultimately result in corporate scandals and securities litigation.

- Compliance failures in asset misappropriation cases typically involve multiple systems and processes. Organizations may fail to implement adequate segregation of duties, provide insufficient training on fraud risks, or maintain inadequate monitoring systems.

- These failures become particularly problematic when they involve senior management, as executive-level misconduct can undermine the entire control environment.

- The aftermath of asset misappropriation discoveries often requires comprehensive remediation efforts that extend far beyond addressing the immediate theft.

- Companies must typically strengthen their internal controls, enhance their fraud detection capabilities, and improve their corporate governance structures to prevent future occurrences and satisfy regulatory requirements.

Building Resilient Defense Systems

- Organizations seeking to prevent asset misappropriation must implement comprehensive control systems that address both the technical and human elements of fraud risk.

- Regulatory compliance requirements provide a foundation for these efforts, but truly effective prevention requires a more holistic approach that integrates technology, processes, and culture.

Companies Must Evolve with Technology

- Technology solutions for fraud prevention have evolved significantly, incorporating artificial intelligence and machine learning capabilities that can identify suspicious patterns in transaction data.

- These systems can detect anomalies that might indicate cash theft, identify potentially fictitious vendors, or flag unusual inventory movements that could suggest theft.

Addressing Fundamental Control Weaknesses

- Process improvements must address the fundamental control weaknesses that enable asset misappropriation.

- This includes implementing appropriate segregation of duties, establishing robust approval processes, and creating comprehensive monitoring systems that can detect fraud in its early stages.

Maintaining Strong Reporting Mechanisms and Employee Training

Cultural initiatives play a crucial role in prevention by creating an environment where employees understand the importance of ethical behavior and feel comfortable reporting suspicious activities.

Organizations that successfully prevent asset misappropriation typically maintain strong ethical cultures supported by comprehensive training programs and clear reporting mechanisms.

The Impact of Accounting Fraud on Investors

- The ramifications of accounting fraud on investors can be severe and multifaceted, affecting both their financial standing and trust in the markets.

- When companies engage in fraudulent accounting practices, they present an inaccurate picture of their financial health, leading investors to make decisions based on false information.

- This often results in overvalued stocks and, when the fraud is exposed, a sharp decline in stock prices ensues, causing substantial financial losses for investors resulting in securities litigation.

Beyond the Financial Losses

- Beyond immediate financial losses, accounting fraud can erode investor confidence in the financial markets. When high-profile companies are involved in fraud, it generates skepticism about the reliability of financial reporting and the effectiveness of regulatory compliance.

- This loss of trust can lead to reduced market participation, as investors become more cautious and risk-averse about a companies corporate governance, potentially increasing the cost of capital for businesses and slowing economic growth.

- Moreover, investors affected by accounting fraud often face lengthy and complex legal battles to recover their losses.

- Securities litigation can be a protracted process, involving intricate legal arguments and extensive evidence gathering.

- The uncertainty and stress associated with such proceedings can further deter investors from engaging with the markets, highlighting the broader implications of accounting fraud on investor sentiment and market stability.

The Evolving Legal Framework of Securities Litigation: Protecting Investors in Modern Markets

The Evolving Legal Framework of Securities Litigation: Protecting Investors in Modern Markets

- The legal framework surrounding securities litigation serves as the cornerstone of investor protection and market integrity in the United States.

- This comprehensive system has evolved significantly since its inception, adapting to address increasingly sophisticated forms of accounting fraud, asset misappropriation, and corporate scandals that threaten the foundation of our financial markets.

Historical Foundation and Core Legislation

Securities Act of 1933

The primary pillars of securities regulation—the Securities Act of 1933 and the Securities Exchange Act of 1934—were born from the market chaos of the Great Depression.

These landmark laws established rigorous requirements for financial disclosures and created powerful prohibitions against fraudulent activities related to securities transactions.

The 1933 Act focuses on initial public offerings and requires companies to provide investors with essential information about securities being offered for sale.

Securities Exchange Act of 1934

Meanwhile, the 1934 Act governs ongoing reporting requirements and secondary market trading.

These foundational statutes created a framework that demands transparency from public companies, requiring them to disclose material information that reasonable investors would consider important when making investment decisions.

Corporate governance standards emerged from these requirements, establishing accountability measures that continue to shape how companies operate today.

The SEC’s Enforcement Arsenal

- The SEC wields substantial authority in enforcing regulatory compliance across the securities markets.

- The Commission’s enforcement division actively investigates potential violations and brings civil enforcement actions against companies and individuals engaged in securities fraud.

- These actions can result in significant remedies, including injunctive relief, substantial monetary penalties, and disgorgement of ill-gotten gains.

- Beyond SEC enforcement, the legal framework empowers private investors to file securities class action lawsuits when they suffer losses due to fraudulent corporate activities.

- This dual enforcement mechanism—combining regulatory oversight with private litigation—creates a robust system for deterring misconduct and compensating harmed investors.

Asset Misappropriation and Accounting Fraud: Modern Challenges

Today’s securities litigation landscape increasingly focuses on sophisticated schemes involving asset misappropriation and accounting fraud.

These violations often involve complex financial manipulations designed to inflate company performance or conceal financial difficulties from investors and regulators.

Asset misappropriation cases typically involve corporate executives or employees who steal or misuse company resources for personal benefit.

These schemes can range from simple embezzlement to elaborate arrangements involving shell companies and fictitious transactions.

A Trigger for Litigation

- When such misconduct affects publicly traded securities, it triggers both regulatory enforcement and private litigation.

- Accounting fraud represents another critical area of securities litigation, encompassing revenue recognition manipulation, expense concealment, and other financial statement distortions.

- These violations directly impact investor decision-making by presenting false or misleading information about a company’s financial health and prospects.

Securities Class Action Lawsuits: Collective Justice

- Securities class action lawsuits provide a powerful mechanism for investors to seek collective redress when corporate misconduct affects large numbers of shareholders.

- These lawsuits enable individual investors with relatively small losses to band together and pursue claims that would be economically unfeasible to litigate individually.

- The Private Securities Litigation Reform Act of 1995 (PSLRA) significantly reformed the class action landscape by implementing heightened pleading standards and other procedural requirements designed to prevent frivolous litigation while preserving legitimate claims.

- Under the PSLRA, plaintiffs must demonstrate specific elements including materiality, scienter (intent to deceive), and loss causation to survive motions to dismiss.

Corporate Governance Failures and Compliance Breakdowns

- Corporate scandals often stem from fundamental compliance failures within company governance structures.

- The Enron and WorldCom scandals of the early 2000s exposed widespread weaknesses in corporate oversight, leading to the passage of the Sarbanes-Oxley Act in 2002.

- This legislation introduced stringent internal control requirements and enhanced penalties for securities violations.

- The 2008 financial crisis prompted additional reforms through the Dodd-Frank Wall Street Reform and Consumer Protection Act, which expanded whistleblower protections and created new regulatory oversight mechanisms.

- These legislative responses demonstrate the legal framework’s capacity to evolve in response to emerging threats to market integrity.

Contemporary Enforcement Trends

Recent developments in securities litigation reflect the increasing complexity of modern financial markets and corporate structures.

Technology companies face heightened scrutiny regarding data privacy, cybersecurity, and artificial intelligence disclosures.

Healthcare and pharmaceutical companies continue to generate significant litigation related to clinical trial results, regulatory approvals, and drug pricing practices.

Regulatory compliance requirements continue expanding as regulators adapt to new business models and emerging risks.

Companies must navigate an increasingly complex web of disclosure obligations while maintaining robust internal controls to prevent fraud and misconduct.

Looking Forward: The Future of Securities Litigation

The legal framework surrounding securities litigation will undoubtedly continue evolving to address emerging challenges in the financial markets.

As corporate structures become more complex and global, securities laws must adapt to ensure continued investor protection while promoting capital formation and economic growth.

Understanding this comprehensive legal framework remains essential for companies seeking to maintain regulatory compliance and avoid costly litigation.

For investors, knowledge of these protections enables informed decision-making and provides avenues for seeking redress when corporate misconduct causes financial harm.

The ongoing evolution of securities litigation law reflects our legal system’s commitment to maintaining fair, transparent, and efficient capital markets that serve the interests of all participants while holding wrongdoers accountable for their actions.

Preventive Measures Against Asset Misappropriation and Accounting Fraud

- Preventing asset misappropriation requires a proactive approach that combines robust internal controls, employee education, and a culture of ethical behavior.

- Organizations must implement comprehensive internal control systems that include segregation of duties, regular audits, and transaction monitoring. These controls help detect anomalies early and reduce opportunities for fraudulent activities.

- Employee education is also crucial in preventing asset misappropriation.

- Training programs that focus on fraud awareness and ethical behavior can empower employees to recognize and report suspicious activities.

Encouraging a Culture of Ethics and Integrity

- Encouraging a culture of transparency and accountability, where employees feel comfortable speaking up, can deter potential fraudsters and foster an environment of trust and integrity.

- Furthermore, organizations should leverage technology to enhance their fraud prevention efforts. Advanced analytics and artificial intelligence can help identify patterns and anomalies that may indicate fraudulent activities.

- By integrating these technologies into their operations, companies can improve their ability to detect and prevent asset misappropriation, ultimately safeguarding their resources and reputation.

Role of Internal Controls in Accounting Fraud Prevention

- Internal controls are a cornerstone of fraud prevention, providing a framework for safeguarding assets, ensuring accurate financial reporting, and maintaining compliance with laws and regulations.

- Effective internal controls involve a combination of policies, procedures, and practices that collectively reduce the risk of fraud and errors within an organization.

- One of the key elements of internal controls is the segregation of duties, which involves dividing responsibilities among different employees to prevent any single individual from having unchecked control over financial transactions.

Regular Audits Reduce the Risk of Fraud

- This reduces the risk of fraudulent activities by ensuring that multiple people are involved in the approval and execution of transactions, making it more challenging for fraud to go undetected.

- Regular audits and reviews are also vital components of internal controls. These processes help identify weaknesses in the control system and provide opportunities for continuous improvement.

- By conducting regular audits, organizations can ensure that their internal controls remain effective and adapt to changing business environments, ultimately reducing the risk of asset misappropriation and accounting fraud.

Future Trends in Securities Litigation

- As we look toward the future, several trends are likely to shape the landscape of securities litigation. One such trend is the increasing role of technology in detecting and preventing fraud.

- With advancements in data analytics and artificial intelligence, companies are better equipped to identify patterns and anomalies that may indicate fraudulent activities, leading to more proactive and efficient fraud prevention measures.

- Another trend is the growing emphasis on environmental, social, and governance (ESG) factors in securities litigation.

- Investors are increasingly holding companies accountable for their sustainability practices and ethical conduct, leading to litigation cases that focus on ESG-related disclosures and misrepresentations.

Creating Long-Term Value for Stakeholders

- This shift reflects a broader recognition of the importance of responsible corporate behavior in creating long-term value.

- Regulatory compliance and international cooperation are also expected to influence securities litigation.

- As markets become more globalized, cross-border collaborations among regulatory bodies will be essential in addressing complex fraud cases that span multiple jurisdictions.

- These trends highlight the need for companies to stay informed and adaptable, ensuring they meet evolving legal and ethical standards in a dynamic regulatory environment.

Conclusion: Safeguarding Against Fraud in 2025

- As we explore the complex area of asset misappropriation and accounting fraud in 2025, it is clear that vigilance and proactive measures are essential in safeguarding against these threats.

- The intricate relationship between accounting fraud and securities litigation underscores the importance of transparency, integrity, and accountability in financial reporting.

- By understanding the warning signs of fraud and implementing robust preventive measures, organizations can protect their assets and maintain investor trust.

- The role of internal controls and technology in fraud prevention cannot be overstated.

- As companies leverage advanced analytics and artificial intelligence, they enhance their ability to detect and prevent fraudulent activities, ultimately safeguarding their resources and reputation.

- Moreover, fostering a culture of ethical behavior and transparency within the organization is crucial in deterring potential fraudsters and fostering an environment of trust and integrity.

- Looking ahead, the future of securities litigation will be shaped by technological advancements, regulatory changes, and a growing emphasis on ESG factors.

- Companies must remain informed and adaptable, ensuring they meet evolving legal and ethical standards in a dynamic regulatory environment.

- By doing so, they can safeguard against fraud and contribute to a more transparent, accountable, and resilient financial market landscape in 2025 and beyond.