Introduction to Securites Ligation Cases in 2025

Securities litigation cases with artificial intelligence have more than doubled in 2024. These cases now rank among the top three trends in the legal world. The momentum has not slowed down.

AI-related securities class actions appeared every month in 2025, except January. The financial effects are massive – the Disclosure Dollar Loss Index hit $403 billion in 2025’s first half, jumping 56% from late 2024.

The spread of these securities class actions tells an interesting story. Tech sector led with eight AI-related securities class actions in 2024. Communications followed with four cases, while industrial had two and consumer had one.

These AI securities class actions have proven tough to dismiss. They’re 30%-50% more likely to survive a motion to dismiss than typical securities class actions. The Maximum Dollar Loss Index has shot up to $1.85 trillion – a dramatic 154% rise from before.

This piece will get into how AI tools are changing legal discovery in securities litigation. We will look at the rise of “AI-washing” claims and give an explanation about risk management strategies for public companies. Mega filings, which represent losses of $5 billion or more, have factored in 83% of total disclosure losses. They also make up 91% of maximum losses in 2025’s first half.

AI-Driven Securities Class Actions: 2025 Filing Trends

The digital world of securities litigation has changed dramatically in 2025. AI-related cases now make up much of class action filings. Let’s look at the key trends that showed up this year.

12 AI-related cases filed in H1 2025

Companies faced 12 AI-related securities class action filings across multiple jurisdictions in the first half of 2025. These cases target companies that allegedly misrepresented their AI capabilities or downplayed AI’s effect on their business models. The cases remain under review.

California stands out as the hotspot for these AI-related claims. The Northern District saw four actions while the Central District handled two. New York, Illinois, New Jersey, Washington, and Idaho split the remaining cases between them.

Comparison with 2024 and 2023 filing volumes in securities class actions

This is a big deal as it means that the 2025 AI-related filings will outpace 2024’s total of 15 cases. The trend keeps climbing – 2024’s 15 cases doubled the seven cases from 2023.

The overall securities class action numbers stayed steady. The first half of 2025 logged 114 total filings, just one less than late 2024’s 115. Money talks though – 2025 set a new record with the highest annual settlement amount ever seen in securities class actions: $4.10 billion.

There’s another reason to pay attention. Crypto-related filings hit six cases by mid-2025, almost matching 2024’s total of seven. Case dismissals might break last year’s record of 124 dismissals.

Rise of AI-washing and AI-risk cases

“AI washing” dominates the 2025 AI-related filings. Companies boost their stock prices by overselling their AI capabilities. These cases claim violations of Section 10(b) of the Exchange Act and Rule 10b-5, pointing to misleading AI-related statements.

Stanford Law Professor and former SEC Commissioner Joseph Grundfest explains it well: “ChatGPT explains the increase in AI-related securities litigation as ‘primarily driven by the phenomenon known as “AI washing”—where companies exaggerate, misrepresent, or falsify the extent or significance of their AI capabilities to investors and the public'”.

These cases fall into two main groups:

- Overstated AI capabilities – Companies paint too rosy a picture of AI’s benefits or promise unrealistic timelines.

- Understated AI risks – Companies stay quiet about how new AI developments could hurt their services. To name just one example, a social media platform faced legal trouble for not telling users that Google’s AI Overview feature might permanently disrupt their traffic.

The first half of 2025 brought groundbreaking enforcement. The SEC and Department of Justice filed joint actions against executives over AI-washing claims. University of Pennsylvania Law Professor Jill E. Fisch puts it simply: “AI statements are market-moving events, and so that’s going to be the focus of litigation until companies figure out what they’re doing with AI and get their disclosures right”.

Key Legal Theories in AI Securities Litigation Cases

The legal foundation for AI securities class action litigation builds on 20-year old frameworks that courts now apply to new technologies. Companies face lawsuits about misrepresenting their AI capabilities, and three main legal theories shape these cases.

Section 10(b) and Rule 10b-5 Misrepresentation Claims in Securities Class Action Settlements

Securities litigation about AI mainly relies on Section 10(b) of the Securities Exchange Act and Rule 10b-5. These rules make it illegal to make false statements when buying or selling securities. Lawsuits often claim that companies exaggerated their AI capabilities, didn’t reveal risks, waited too long to admit failures, or weren’t honest about how they used AI.

Jaeger v. Zillow Group Inc. stands out as a good example. Plaintiffs said Zillow wasn’t truthful about how accurate its algorithms were in the “Zestimate offer” program. The company promoted its AI use while actually depending on human workers, which led them to pay too much for thousands of homes. The court let these AI-related claims move forward.

In re Upstart Holdings Inc. Securities Litigation shows another case. Plaintiffs claimed the company wasn’t honest when it said its AI loan system gave “higher approval rates and lower interest rates at the same loss rate” compared to regular FICO scores. The court agreed that plaintiffs “adequately pled that the Upstart model did not provide these specific verifiable advantages“.

The Supreme Court’s ruling in Macquarie Infrastructure Corp. v. Moab Partners made a vital difference. Simply not saying something isn’t enough for Rule 10b-5(b) claims. Plaintiffs must point to specific misleading statements and show the difference between “half-truths” and “pure omissions”.

Section 11 IPO Disclosure Violations

Section 11 of the Securities Act of 1933 differs from Section 10(b) claims. Companies can be liable just for leaving out required information, even without making misleading statements. This creates a big difference in how courts handle missing information in IPO documents.

AI securities class actions in 2024 often include claims about Initial Public Offering registration statements under Section 11. A recent case showed how this works. The court believed former employees who said their company wasn’t using AI in logistics as claimed in offering materials.

The Supreme Court highlighted this difference. They pointed out that “Congress imposed liability for pure omissions in § 11(a) of the Securities Act of 1933.” Section 10(b) needs specific statements before courts can decide if other facts were needed to make them “not misleading”.

Scienter and Materiality in AI Statements

Courts look carefully at scienter (intent to deceive) and materiality in AI claims. One court threw out fraud claims because plaintiffs couldn’t prove executives meant to deceive. Executives wanting to “hide past mistakes, keep their jobs, or protect their reputations” wasn’t enough to show fraud.

Courts treat specific AI claims differently from vague promotional statements. Calling an AI model “magical” or saying it “shined” won’t support a lawsuit. Another court ignored general statements about strong technology but took seriously specific claims about AI use.

SEC Chair Gary Gensler explained it well: “Claims about prospects should have a reasonable basis, and investors should be told that basis”. Courts continue to use this idea of specific, provable claims versus general promotion to judge AI securities cases.

AI-Washing Allegations in Securities Class Action Litigation

“AI-washing” has become a new category of securities class actions where companies face lawsuits for overstating their artificial intelligence capabilities to boost stock prices. This issue caught everyone’s attention after SEC Chair Gary Gensler voiced his concerns in December 2023 about companies that might mislead investors about their real AI capabilities. The number of securities class actions about AI-washing has grown rapidly. Fifteen such cases were filed in 2024, twice the number from 2023.

Overstated AI capabilities in product marketing

Courts that look at AI-washing cases see a clear difference between vague marketing language and specific, verifiable claims about AI capabilities. The court in In re Upstart Holdings, Inc. Securities Litigation decided that calling an AI model a “fairly magical thing” was just marketing talk. However, specific claims about the AI model’s “significant advantage” over “traditional FICO-based models” could lead to legal action if proven false.

The same principle applied in In re General Motors Co. Securities Litigation. The court ruled that claims about vehicles running “with no human in the loop” could be proven false. Yet descriptions like “fully driverless” were too vague to support fraud claims. This difference between specific, verifiable claims and general marketing language shapes how courts handle AI-washing cases.

The Federal Trade Commission also tackles deceptive AI claims. Software provider accessiBe had to pay $1 million because it misrepresented its AI product’s ability to make websites meet accessibility guidelines. The company made claims about its AI capabilities without enough evidence.

False revenue projections tied to AI features Results in Securities Class Action Litigation

Companies often face lawsuits when they miss their public goals related to AI development. A good example comes from Genesee County Employees’ Retirement System v. DocGo Inc. An executive highlighted his “graduate degree in computational learning, which is a subset of artificial intelligence”. He used these credentials to support claims that the company’s AI systems would “need as little people as possible”.

Skyworks provides another example. The company predicted strong growth in smartphones, claiming AI would “ignite a transformative smartphone upgrade cycle”. Investors sued after poor financial results, saying the company “oversold Skyworks’ position and ability to capitalize on AI in the smartphone upgrade cycle”.

Case example: Oddity Tech Ltd.

A fresh AI-washing case surfaced in July 2024 against Oddity Tech Ltd., an online cosmetics platform. After its July 2023 IPO, Oddity branded itself as a revolutionary force in cosmetics. The company claimed it used proprietary AI-based technologies to meet consumer needs.

Short-seller NINGI Research published a report on May 21, 2024, claiming Oddity had “completely misled investors about every critical aspect of its business”. The report stated Oddity’s AI approach was “nothing but a questionnaire” and its high “repeat purchase rates” came from “customers unknowingly entering into non-cancelable plans”.

The lawsuit that followed claimed violations of Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5. Oddity allegedly “overstated its AI technology and capabilities, and/or the extent to which this technology drove the company’s sales”. The complaint also said the company’s “repeat purchase rates and revenues were, at least in part, derived from unsustainable and deceptive sales and advertising practices”.

The SEC settled charges with two investment advisers in March 2024. Delphia (USA) Inc. and Global Predictions Inc. made false statements about their AI use. They agreed to pay $400,000 in total civil penalties. SEC’s Division of Enforcement Director Gurbir S. Grewal made it clear: “We are committed to protecting [investors] against those engaged in ‘AI washing'”.

AI-Risk Disclosure Failures and Emerging Claims in Securities Litigation Cases

Companies not only exaggerate AI capabilities, but they also fail to reveal the most important AI-related risks. This has become the second biggest trend in 2025 securities litigation. These new claims focus on how businesses downplay or completely skip disclosing AI’s negative effects on their operations and business models.

Understated third-party AI impact risks

AI has become essential to business operations. Many companies focus solely on their own AI systems. They often miss how their vendors, subcontractors, and service providers make use of this technology. This creates a huge risk exposure. Third parties now employ AI in cloud platforms, SaaS tools, and outsourced services to boost performance and automate decisions.

The stakes here are quite high. Third-party AI usage processes sensitive data and automates crucial decisions. It creates dependencies that are hard to audit or control. Current oversight tools like SOC 2 reports or basic risk questionnaires don’t dig deep enough. They can’t properly assess how vendors use AI, what data they depend on, or if they have proper controls in place.

SEC Enforcement Director Gurbir S. Grewal highlighted this risk area. He said the SEC looks at “what a person actually knew or should have known; what the person actually did or did not do; and how that measures up to the standards of [the SEC’s] statutes, rules, and regulations”. This scrutiny grew stronger in 2024-2025. Companies moved from narrow to generative to agentic AI, which made risks much more complex.

Zero-click search and traffic loss: Reddit case

A notable securities class action emerged against Reddit after its IPO in early 2025. The case claimed Reddit didn’t disclose how AI-powered “zero-click” search results could hurt its traffic and revenue. The complaint cited data showing more than 50% of Google searches now end without an organic click. This led to growing losses in both revenue and leads.

The lawsuit pointed to research with some alarming numbers. Click-through rates for top search results drop by 39% when AI-generated content shows up. Studies also show about 60% of Google searches get no clicks at all. Reddit knew but didn’t tell investors how these AI search developments would permanently change user traffic patterns.

This case shows a new trend. Securities class actions now targets companies that don’t disclose how external AI developments might hurt their core business metrics. As zero-click search becomes normal and organic traffic keeps dropping, other platform companies will likely face similar lawsuits.

Delayed AI rollouts: Apple Siri Securities Class Action Litigation

Apple’s delayed Siri upgrades turned into 2025’s biggest AI risk disclosure case. Shareholders filed a securities fraud class action against Apple, CEO Tim Cook, current CFO Kevan Parekh, and former CFO Luca Maestri in June 2025.

The lawsuit claims Apple misled investors at its June 2024 Worldwide Developers Conference. Apple suggested AI would drive iPhone 16 sales through better Siri features. Instead, they pushed the promised Siri updates to 2026. This led to poor iPhone sales and a big drop in stock price.

The case centers on one key claim. Apple had no working prototype ready and “could not reasonably believe the features would be ready” for the iPhone 16 lineup. Apple shares hit a record high in December 2024, then dropped by nearly 25%. This wiped out about $900 billion in market value.

This case shows how securities litigation now goes after companies that set unrealistic AI rollout timelines, especially when linked to revenue projections or product launches. The court must decide if Apple’s statements were forward-looking projections protected by safe harbor rules or if they misrepresented current capabilities and development status.

Sector-Specific Litigation Patterns in 2025

Litigation patterns in 2025 show clear concentrations in specific sectors and court preferences, with notable changes in both case numbers and financial effects across industries.

Technology and cybersecurity sector concentration

AI-related securities litigation has spread to many industries, but the technology sector remains the main target. The AI-related case filings in 2024 show that eight cases centered in the technology sector, while four were in communications, two in industrial, and one in consumer sectors. The total number of technology sector filings dropped slightly to 20 cases from 23 in the previous period. This lower number of cases doesn’t tell the whole story because technology companies faced much higher market capitalization losses.

The number of cybersecurity-related lawsuits kept falling from its peak of seven filings in 2021, with only two cases filed in 2024. Companies might have improved their disclosure practices, or plaintiff attorneys might have shifted their focus to more profitable AI-related claims.

Consumer non-cyclicals and biotech exposure

Consumer non-cyclical sector became the hotbed of litigation in 2025, with a 31% rise in filings compared to late 2024. Biotechnology and pharmaceutical companies faced more scrutiny, which drove this increase. The sector felt a disproportionate effect—consumer non-cyclical companies suffered 62% of the total disclosure losses while making up only 44% of core filings.

The concentration within this sector runs even deeper. Health services and pharmaceutical subsectors made up 31% of filings but created 65% of total losses. Cornerstone Research called this concentration of huge financial losses in just a few cases “the most important risk management challenge” in their analysis.

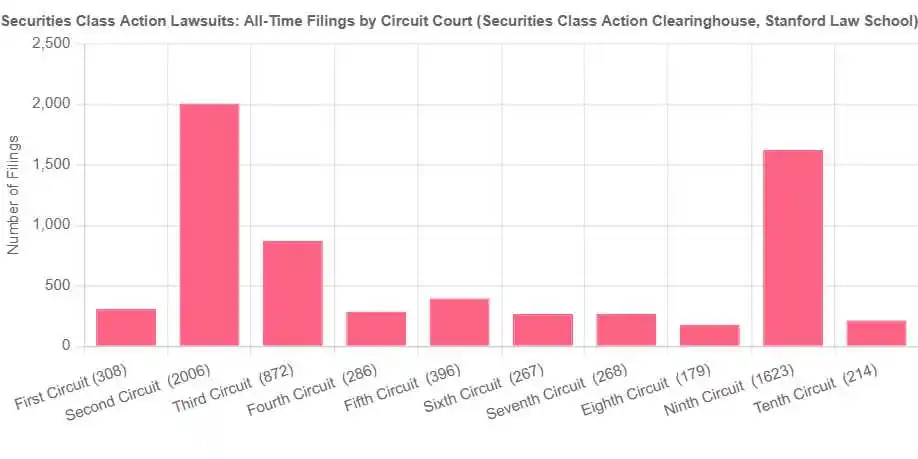

Jurisdictional hotspots for AI Securities Class Actions: ND Cal, SDNY, D. Mass

California has become the go-to forum for AI-related securities litigation. Four actions were filed in the Northern District of California and two in the Central District of California during early 2025. Plaintiffs also filed cases in:

- New York (including SDNY)

- Illinois

- New Jersey

- Washington

- Idaho

The Third Circuit saw its filings more than triple, mostly from biotech and pharmaceutical cases. The Eleventh Circuit experienced a similar increase in numbers. The Southern District of New York managed to keep its importance. Judge John P. Cronan’s July 2025 decision highlighted this when he dismissed a putative securities class action against an AI company that allegedly made misleading statements about its turnaround strategy.

Plaintiffs’ attorneys seem to choose courts based on where specific industries cluster or where securities litigation has historically succeeded.

Regulatory Oversight and SEC Enforcement Actions

Federal regulators have stepped up their examination of AI-related disclosures through 2024-2025. They have set new enforcement priorities and compliance expectations for public companies.

SEC AI disclosure guidance and enforcement

The SEC now watches AI-related disclosures more closely as more companies mention AI in their public filings. The agency took its first enforcement actions against two investment advisers in March 2024. These firms faced penalties between $175,000 and $225,000 for falsely claiming to use AI in their investment decisions.

The SEC appointed a senior leader as Chief Artificial Intelligence Officer (CAIO) to advance AI adoption and governance throughout the agency. This officer implements AI guidance from the Office of Management and Budget.

SEC data shows AI-related securities class actions were 30%-50% less likely to be resolved through motions to dismiss compared to other securities cases from 2020-2023. Companies now face greater legal risks when making claims about their AI capabilities.

DOJ and FTC investigations into AI misstatements

The SEC and Department of Justice filed joint actions against Nate Inc.’s founder Albert Saniger in April 2025. They alleged Saniger made false claims about his company’s AI technology. The mobile shopping app supposedly used AI, but foreign contract workers processed transactions manually. These alleged false statements helped Saniger raise more than $42 million over three years.

The FTC launched an investigation into generative AI investments and partnerships at the same time. They sent orders to Alphabet, Amazon, Anthropic, Microsoft, and OpenAI. The investigation seeks details about specific investments, practical effects, competitive impact, and competition for AI resources.

Securities Class Actions: AI-related compliance expectations for issuers

Companies must focus on accurate disclosures and proper internal controls. Regulators recommend that companies should:

- Define AI terms clearly in their disclosures

- Share specific, relevant information based on AI’s importance to the company

- Describe actual or planned AI use instead of general industry trends

- Support all AI-related claims with solid evidence

Eric Gerding, Director of the SEC’s Division of Corporation Finance, named AI as a key disclosure priority. He noted many more companies now mention artificial intelligence in their annual reports. Companies must review their AI-related disclosures carefully to avoid enforcement actions from overstated capabilities or hidden risks.

Risk Mitigation Strategies for Public Companies to Avoid Securities Class Actions

The rise in AI-related class action trends cases means public companies just need detailed protection measures to reduce legal risks. A SEC official analyzed AI disclosures and noted that “no one is on the same page”. This lack of consistency creates vulnerabilities that need a planned approach.

Consistent AI definitions across disclosures to avoiod securities class actions

Companies should standardize their AI terminology in all public communications to avoid securities class action litigation liability. Recent studies show approximately 18% of S&P 500 companies and 12% of Russell 3000 companies now mention AI in their risk factors. Legal exposure increases when definitions differ between investor presentations, earnings calls, marketing materials, and SEC filings.

Companies should avoid defining AI differently when highlighting opportunities versus discussing risks. Organizations can protect themselves by creating company-wide glossaries for AI terms. This ensures marketing teams, investor relations, and legal departments use similar definitions in all external communications.

Internal controls for AI-related statements can greatly help in avoiding Securities Class Action Litigation

Good governance requires strong internal controls specifically for AI-related disclosures. These controls help reduce risks related to errors, data privacy, operational failures, ethics and noncompliance. Essential components include:

- Human oversight of AI-generated outputs with detailed validation protocols

- Tailored review processes based on specific AI applications’ complexity and risk

- Verification procedures for third-party AI systems that blend into company operations

The audit committee should participate in these controls. Note that audit committee members “may have an increased need for digital upskilling to enable their understanding and ability to govern new and emerging risks from AI”.

Forward-looking risk disclosures and disclaimers leading to securities class action litigation

Future disclosures should address six key risk categories found in corporate filings: regulatory risks, operational risks, competitive risks, cybersecurity risks, ethical risks, and third-party risks. Research shows companies that disclose more AI risks show higher stock and option-implied volatility. This signals that investors recognize uncertainty.

Risk reduction depends on companies conducting full AI-specific audits that match their unique business models. These assessments should include stakeholders from business units, third-party vendors, and AI providers to spot vulnerabilities before they appear in securities class action litigation.

Case Study Highlights: Super Micro, UiPath, CrowdStrike

Recent securities class actions against three prominent companies demonstrate significant financial risks when AI systems fail or companies overstate their capabilities.

Super Micro: Revenue misallocation and export violations

A Hindenburg Research report published in August 2024 sparked the Super Micro Computer litigation. The short-seller accused Super Micro of manipulating financial reports and breaking U.S. export regulations to China and Russia. Super Micro’s stock dropped 12% after the company delayed filing its annual report.

The Department of Justice started investigating alleged financial misconduct and possible sanctions evasion. The situation became more serious as Super Micro’s exports to Russia surged threefold after the Ukraine invasion. The company shipped products worth $46.30 million to Niagara Computers, a supplier connected to a previously secret Russian nuclear research center.

Super Micro’s independent Special Committee conducted a detailed three-month investigation and found “no evidence of misconduct”. The committee decided no financial restatement was needed.

UiPath: AI rebranding and missed revenue targets

UiPath faced securities class action litigation after rebranding as an “AI-powered Business Automation Platform” in September 2022. The securities class action litigation UiPath misled investors about executing valuable multi-year contracts. The company made internal changes that discouraged such deals.

The company’s first quarter 2025 revenue fell short at $423.60 million compared to expected $425.30 million. Bank of America downgraded UiPath to “Underperform”. The stock price fell 58% year-over-year and hit a record low of $9.50.

CrowdStrike: Faulty AI update and stock crash

CrowdStrike’s troubles began with a disastrous software update on July 19, 2024, that crashed 8.5 million Microsoft Windows computers worldwide. This disruption caused global chaos with potential economic damages reaching tens of billions of dollars.

Shareholders filed securities class action litigation claiming CrowdStrike made “false and misleading” statements about software testing. CEO George Kurtz had stated in March that the company’s software was “validated, tested and certified”. CrowdStrike’s share price dropped 32% in 12 days, wiping out $25 billion in market value.

Delta Air Lines lost $500 million from the outage and filed a separate lawsuit stating the update was “pushed out in an unsafe manner”.

Conclusion

AI-related securities class action litigation has grown dramatically through 2024-2025, which shows a major change in the legal world. These cases have doubled since 2023 and now rank among the most costly categories of securities litigation. The disclosure losses are a big deal as they mean more than $403 billion just in the first six months of 2025.

Clear patterns show up in this wave of Securities Litigation Cases. “AI-washing” claims target companies that supposedly inflate their tech capabilities to drive up stock prices. Companies also face trouble when they downplay how external AI developments could hurt their business models. These trends show that AI has become crucial information that reasonable investors need.

Securities Class Actions about AI claims are more successful at fighting dismissal motions than traditional securities cases. Courts seem to view specific, verifiable AI capability claims as potentially valid, while they dismiss vague promotional language as simple marketing talk.

The SEC, DOJ, and FTC have noticed this trend and created new enforcement priorities that target AI misrepresentations. Their actions against both executives and companies who misstate their AI capabilities point to closer monitoring in the future.

Companies need to change fast. They should create consistent AI definitions in all public statements and build strong controls for AI communications. A detailed risk disclosure plan will help protect them. On top of that, they must carefully check how outside AI use might affect their operations.

Courts will keep working to clarify the difference between valid AI misrepresentations and protected forward-looking statements. Companies that can highlight AI opportunities while acknowledging real risks will face less litigation risk in this fast-changing legal environment.

Key Takeaways

AI-related Securities Class Action Litigation has exploded in 2025, with cases doubling from 2023 and creating unprecedented financial exposure for public companies across multiple sectors.

• AI-washing allegations dominate litigation trends – Companies face securities class action litigation for exaggerating AI capabilities or understating AI risks, with cases 30-50% less likely to be dismissed than traditional securities litigation.

• Financial impact reaches record levels – The Disclosure Dollar Loss Index hit $403 billion in H1 2025, marking a 56% increase as AI-related claims generate massive market cap losses.

• Two distinct legal theories emerge – Courts distinguish between actionable specific AI capability claims versus protected “puffery,” while also targeting failures to disclose external AI risks to business models.

• Regulatory enforcement intensifies rapidly – SEC, DOJ, and FTC have launched parallel investigations and enforcement actions, establishing AI disclosure compliance as a top regulatory priority.

• Risk mitigation requires comprehensive strategy – Companies must standardize AI definitions across all communications, implement robust internal controls, and develop tailored risk disclosures to avoid litigation exposure.

The surge in AI securities litigation reflects how artificial intelligence has become material information for investors, requiring companies to balance promotional opportunities with accurate risk disclosure to minimize legal vulnerability.

Timothy L. Miles, Esq.

Law Offices of Timothy L. Miles

Tapestry at Brentwood Town Center

300 Centerview Dr. #247

Mailbox #1091

Brentwood,TN 37027

Phone: (855) Tim-MLaw (855-846-6529)

Email: [email protected]

Website: www.classactionlawyertn.com

Facebook Linkedin Pinterest youtube

Visit Our Extensive Investor Hub: Learning for Informed Investors