Introduction to Implementing Strong Internal Controls

Implementing Strong Internal Controls: Encompasses the implementation of the processes, policies and regulations that will ensure your organization is run efficiently, ethically and responds to its stakeholders.

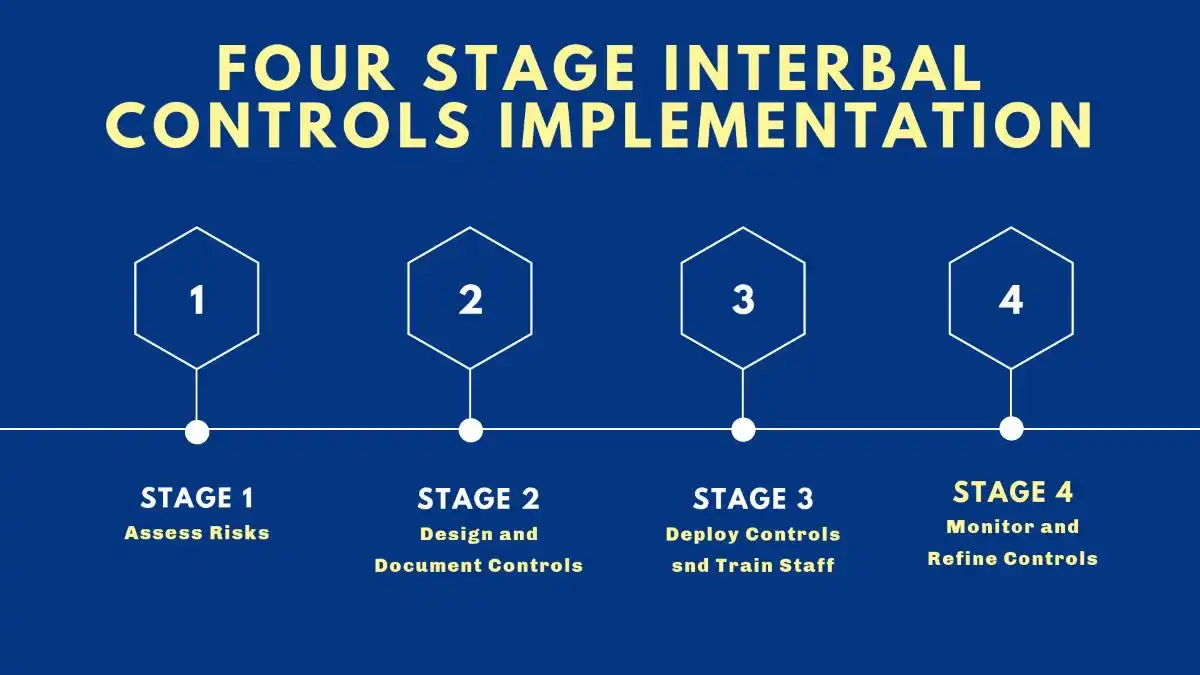

- Implementation Process: Access risk, design and document controls, deploy controls and train staff, and monitor and refine risk.

Corporate Governance: The system of rules, practices, and processes that directs and controls a company.

- It balances the interests of a company’s many stakeholders, including shareholders, management, customers, and the community, and provides a framework for achieving the company’s goals through , accountability, and responsibility.

- Its purpose is to ensure the company is run ethically and efficiently, and good governance is vital for a company’s long-term success, reputation, and sustainability.

Complex Environment: Businesses navigate an increasingly complex regulatory landscape, understanding these frameworks becomes crucial for investors seeking to protect their interests and foster sustainable growth.

Transparency through Financial Reporting: Openly, accurately, and understandably disclosing a company’s financial performance, risks, and activities to stakeholders. This process builds trust, enhances accountability, and helps prevent fraud by providing a clear picture of a company’s financial health through complete, accurate, and timely reports.

Securities Litigation: Usually the result of weak internal controls that allows shareholders to rely on false and misleading financial disclosures and when the truth comes out in a corrective disclosure they lose money and file securities litigation as a collective way of recouping the money they lost.

Understanding Internal Governance and Its Importance

Pivotal Role of Corporate Governance: In an ever-evolving corporate landscape, internal governance plays a pivotal role.

- It encompasses the processes, policies, and regulations that ensure an organization operates efficiently and ethically.

- Effective internal governance is crucial as it builds trust among stakeholders and enhances organizational integrity.

- By fostering a culture of accountability, you can significantly mitigate the risks associated with operational failures and misconduct.

Internal governance is not just about compliance with laws and regulations but also about nurturing a robust organizational culture. It empowers you to manage resources effectively, ensuring that the strategic goals of your organization align with ethical practices. As businesses face increasing scrutiny, strengthening internal governance becomes crucial to maintaining a competitive edge.

- The importance of internal governance extends beyond mere compliance.

- It is about creating a sustainable framework that supports long-term growth and stability.

- By emphasizing governance, you can improve decision-making processes, enhance transparent communications, and ultimately drive business success.

What Are Internal Controls?

Internal controls are mechanisms put in place to ensure the reliability and integrity of financial and operational information. They help safeguard assets, ensure the accuracy of financial records, and promote operational efficiency. Implementing strong internal controls is essential to prevent fraud, errors, and inefficiencies within your organization.

These controls can be classified into preventive, detective, and corrective controls.

- Preventive controls aim to deter errors or irregularities from occurring.

- Detective controls are designed to identify errors that have already occurred, while corrective controls focus on rectifying identified anomalies.

- By understanding these categories, you can develop a comprehensive internal control framework tailored to your organization’s needs.

Moreover, internal controls are integral to achieving strategic goals. They provide a structured approach to risk management, allowing you to anticipate potential challenges and respond proactively. By embedding these controls into your operations, you create a resilient framework that adapts to changing business environments.

The Role of Internal Controls in Corporate Governance

Corporate governance refers to the system by which companies are directed and controlled.

- Internal controls are a fundamental component of this system, ensuring that the interests of stakeholders are protected.

- They provide a mechanism for accountability and oversight, crucial for maintaining investor confidence and safeguarding your organization’s reputation.

- Internal controls support corporate governance by promoting transparency and accountability.

- They ensure that management’s actions are consistent with the company’s policies and objectives.

- By doing so, they enhance the board’s ability to monitor performance and make informed decisions, thereby aligning management’s actions with shareholder interests.

Furthermore, internal controls play a critical role in mitigating risks associated with financial reporting.

- They ensure the reliability of financial statements, providing assurance to investors and regulators.

- In an era where corporate scandals can lead to significant financial and reputational damage, robust internal controls are indispensable to maintaining trust and credibility.

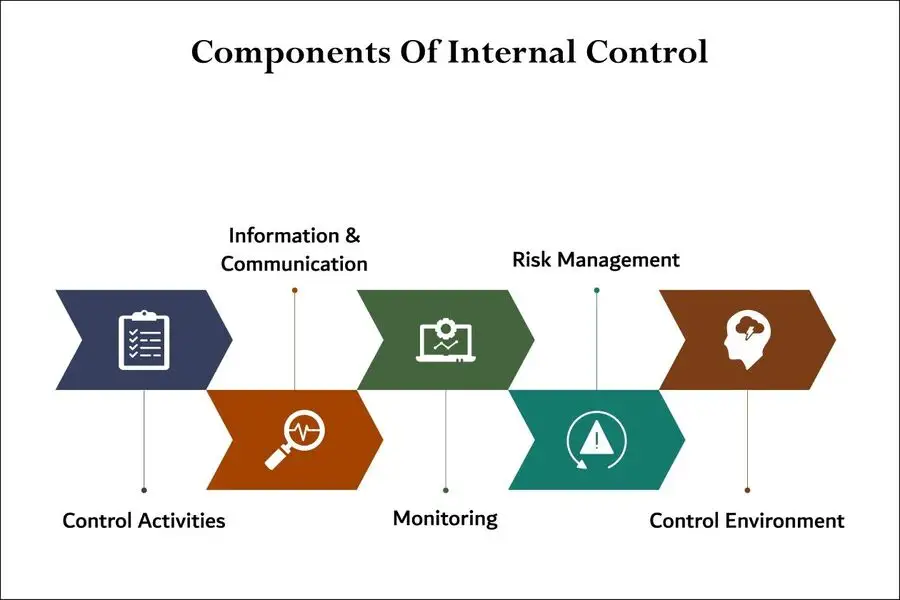

Key Components of Strong Internal Controls

Building effective internal controls involves several key components. These components form the backbone of a strong internal control system, ensuring that your organization operates efficiently and ethically.

- Control Environment: This is the foundation of any internal control system. It includes the organization’s values, integrity, and ethical standards. A strong control environment sets the tone for the entire organization, emphasizing the importance of internal controls.

- Risk Assessment: Identifying and assessing risks is crucial to implementing effective internal controls. By understanding potential threats, you can develop strategies to mitigate them, ensuring that your organization is well-prepared to face challenges.

- Control Activities: These are the policies and procedures put in place to address identified risks. Control activities ensure that management directives are carried out effectively, preventing errors and irregularities.

- Information and Communication: Effective internal controls rely on timely and accurate information. Ensuring that relevant information is communicated to the right people is vital for decision-making and accountability.

- Monitoring: Continuous monitoring of internal controls is essential to ensure their effectiveness. Regular assessments help identify areas for improvement, ensuring that your internal control system remains relevant and robust.

By focusing on these components, you can implement a comprehensive internal control framework that supports your organizational objectives.

Why Transparency Matters in Internal Governance

Transparency is a cornerstone of effective internal governance.

- It enhances trust and confidence among stakeholders by providing clear, accurate, and timely information about organizational activities.

- Transparency ensures that stakeholders have access to relevant information, enabling informed decision-making and fostering accountability.

- Incorporating transparency into your governance practices strengthens relationships with stakeholders, including employees, investors, and regulators.

- It demonstrates a commitment to ethical practices and accountability, which is essential for building a positive organizational reputation.

- By being transparent, you create an environment where stakeholders feel valued and engaged.

Moreover, transparency reduces the likelihood of unethical behavior by promoting accountability and oversight.

- It encourages open communication and collaboration, essential for addressing potential issues before they escalate.

- By prioritizing transparency, you can foster a culture of integrity and trust, ultimately contributing to long-term organizational success.

The Consequences of Weak Internal Controls

Severe Consequences: Weak internal controls can have significant consequences for your organization including ending up in costly securities fraud litigation.

- They increase the risk of fraud, errors, and inefficiencies, potentially leading to financial losses and reputational damage.

- Without robust controls, your organization is vulnerable to operational disruptions, compliance failures, and strategic misalignments.

Restatement of Financials: One of the most severe consequences of weak internal controls is financial misstatement. Inaccurate financial reporting can lead to securities litigation, regulatory enforcement, loss of investor confidence, and regulatory penalties. Furthermore, weak controls can result in unauthorized transactions, asset misappropriation, and other fraudulent activities.

Lack of Accountability: In addition to financial repercussions, weak internal controls can impact employee morale and organizational culture. A lack of accountability and oversight can lead to ethical lapses, creating an environment of distrust and disengagement. By strengthening internal controls, you can mitigate these risks and protect your organization’s interests.

Steps to Implement Strong Internal Controls in Your Organization

Implementing strong internal controls requires a strategic and systematic approach. Here are some steps to guide you in developing an effective internal control framework:

- Conduct a Risk Assessment: Identify potential risks that could impact your organization. Assess the likelihood and impact of these risks, prioritizing them based on their significance.

- Develop Control Activities: Establish policies and procedures to address identified risks. Ensure that these controls are aligned with your organization’s objectives and are communicated effectively to all relevant stakeholders.

- Enhance the Control Environment: Foster a culture of integrity and accountability by promoting ethical behavior and setting clear expectations. Encourage management and employees to prioritize internal controls as part of their daily operations.

- Implement Monitoring Mechanisms: Regularly assess the effectiveness of your internal controls. Conduct audits and reviews to identify areas for improvement and ensure that controls remain relevant and effective.

- Facilitate Information and Communication: Ensure that accurate and timely information is communicated to the right stakeholders. Encourage open communication to support decision-making and accountability.

Comprehensive Controls: By following these steps, you can implement a comprehensive internal control framework that supports your organization’s strategic goals.

Best Practices for Maintaining Internal Controls

Ongoing Vigilance: Maintaining effective internal controls requires ongoing commitment and vigilance. Here are some best practices to ensure the sustainability of your internal control framework:

- Regularly Review and Update Controls: Continuously assess the effectiveness of your internal controls and make necessary adjustments to address emerging risks and challenges.

- Provide Training and Awareness: Educate employees about the importance of internal controls and their role in maintaining organizational integrity. Regular training sessions can help reinforce the significance of internal controls and ensure compliance.

- Foster a Culture of Accountability: Encourage employees to take ownership of their responsibilities and hold them accountable for their actions. A culture of accountability promotes ethical behavior and supports the effectiveness of internal controls.

- Leverage Technology: Utilize technology to automate control processes and enhance efficiency. Implementing advanced data analytics can help identify anomalies and support decision-making.

- Engage Stakeholders: Involve stakeholders in the development and implementation of internal controls. Their input can provide valuable insights and enhance the effectiveness of your control framework.

Best Practices: By adhering to these best practices, you can maintain a robust internal control system that supports your organization’s objectives and mitigates risks.

The Link Between Controls and Securities Litigation

Internal controls play a critical role in mitigating the risk of securities class action litigation. Securities litigation typically arises from allegations of financial misrepresentation or fraud, often due to weak internal controls. By implementing strong internal controls, you can reduce the likelihood of such litigation and protect your organization from legal liabilities.

Robust Controls: Effective controls ensure the accuracy and reliability of financial reporting, providing assurance to investors and regulators. They help prevent fraudulent activities and financial misstatements, reducing the risk of regulatory scrutiny and legal action. By prioritizing internal controls, you can enhance investor confidence and safeguard your organization’s reputation.

Addresses Legal Requirements: Moreover, a robust control framework supports compliance with securities laws and regulations. It ensures that your organization adheres to legal requirements, minimizing the risk of penalties and sanctions. By linking internal controls with litigation, you can proactively address potential risks and protect your organization’s interests.

THE SECURITIES LITIGATION PROCESS

|

Filing the Complaint |

A lead plaintiff files a lawsuit on behalf of similarly affected shareholders, detailing the allegations against the company. |

|

Motion to Dismiss |

Defendants typically file a motion to dismiss the class action lawsuits, arguing that the complaint lacks sufficient claims. |

|

Discovery |

If the motion to dismiss is denied, both parties gather evidence, documents, emails, and witness testimonies. This phase of the litigation can be extensive. |

|

Motion for Class Certification |

Plaintiffs request that the court to certify the litigation as a class action. The court assesses factors like the number of plaintiffs, commonality of claims, typicality of claims, and the adequacy of the proposed class representation. |

|

Summary Judgment and Trial |

Once the class is certified, the parties may file motions for summary judgment. If the case is not settled, it proceeds to trial, which is rare for securities class actions. |

|

Settlement Negotiations and Approval |

Most securities litigation cases are resolved through settlements, negotiated between the parties, often with the help of a mediator. The court must review and grant preliminary approval to ensure the settlement is fair, adequate, and reasonable. |

|

Class Notice |

If the court grants preliminary approval, notice of the settlement is sent to all class members often by mail, informing them about the terms and how to file a claim. |

|

Final Approval Hearing |

The court conducts a final hearing to review any objections and grant final approval of the settlement of the securities litigation. |

|

Claims Administration and Distribution |

A court-appointed claims administrator manages the process of sending notices, processing claims from eligible class members, and distributing the settlement funds. The distribution is typically on a pro-rata basis based on recognized losses. |

Conclusion: The Future of Internal Governance and Compliance

Internal Governance: As we look to the future, internal governance and compliance will continue to be critical for organizational success. Strong internal controls are essential for navigating the complexities of the modern business environment and ensuring long-term sustainability. By prioritizing internal governance, you can enhance accountability, and trust among stakeholders.

Proactive and Maintain: To thrive in the competitive landscape of 2025 and beyond, you must be proactive in implementing and maintaining effective internal controls. By fostering a culture of integrity and accountability, you can mitigate risks, drive innovation, and achieve your strategic objectives. As you embark on this journey, remember that internal governance is not a one-time effort but an ongoing commitment to excellence.

Call to Action: Now is the time to take action. Evaluate your current internal control framework and identify areas for improvement. Collaborate with your team to implement best practices and ensure that your organization is prepared to face future challenges. By mastering internal governance, you can pave the way for sustainable growth and success. Start today by prioritizing controls and building a resilient foundation for your organization.

FREQUENTLY ASKED QUESTIONS

1. What are internal controls?

Internal controls comprise the plan of organization and all coordinated methods adopted within a business to:

- Safeguard assets

- Check the accuracy and reliability of accounting data

- Promote operational efficiency

- Encourage adherence to prescribed managerial policies

In simpler terms, internal controls are anything we do to help achieve our objectives—logical, common-sense procedures applied to business processes.

2. What is the purpose of internal controls?

Internal controls serve four primary purposes:

- To protect the organization’s assets

- To ensure records are accurate

- To promote operational efficiency

- To encourage adherence to policies and procedures

3. What are the different types of internal controls?

There are two main types of internal controls:

Preventative Controls: Designed to discourage errors or irregularities from occurring.

Example: Processing vouchers only after obtaining approval signatures.

Detective Controls: Designed to find errors or irregularities after they have occurred.

Example: Reconciling monthly account statements.

4. Who is responsible for internal controls?

Internal controls are the responsibility of management, not internal auditors. Every employee plays a role in either strengthening or weakening the organization’s internal control system. Internal auditors evaluate controls and make recommendations for improvements, but implementation and maintenance remain management’s responsibility.

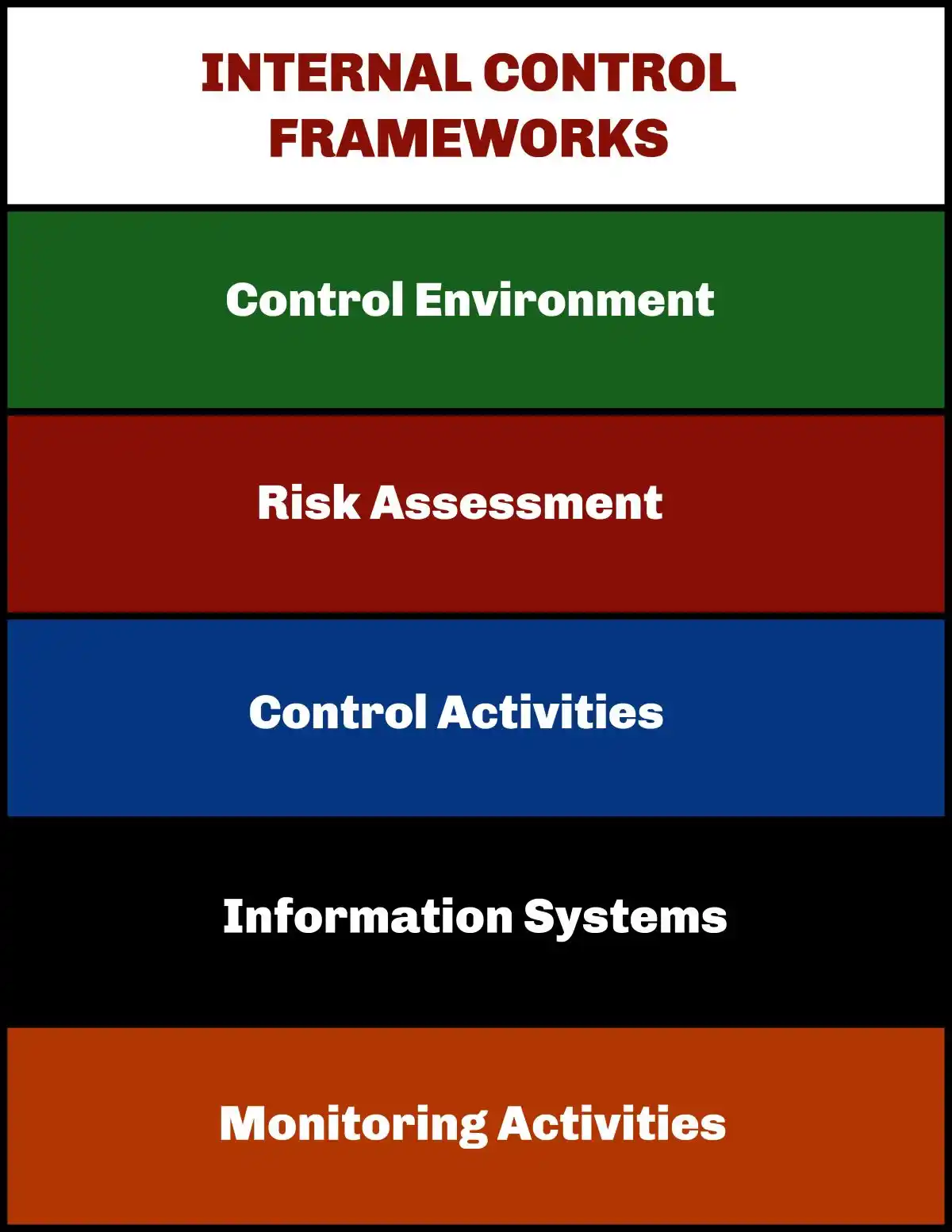

5. What are the five components of the COSO Internal Control Framework?

The Committee of Sponsoring Organizations (COSO) Framework identifies five essential components:

- Control Environment: Sets the tone for the organization, influencing control consciousness

- Risk Assessment: Involves identification and analysis of relevant risks

- Control Activities: Policies and procedures that help ensure management directives are carried out

- Information and Communication: Systems supporting identification, capture, and exchange of information

- Monitoring Activities: Processes that assess internal control quality over time

6. How does internal control relate to risk management?

The internal control system forms the foundation of risk management. It supports management in controlling and managing risks inherent in business activities. Organizations determine their goals, identify internal risks that might prevent achieving them, and implement control measures to mitigate these risks.

7. What is the relationship between internal control and internal audit?

Internal control and internal audit are different but complementary concepts:

- Internal control is built into processes and workflows, influenced by people, and used to achieve business objectives

- Internal audit evaluates the effectiveness and appropriateness of internal controls

While internal control constitutes a foundation of organizational institutionalization, internal audit assesses the quality and appropriateness of those controls.

8. How can an organization ensure it has appropriate controls?

Organizations can ensure appropriate controls by:

- Performing self-assessments of controls

- Requesting an internal audit for an independent assessment

- Participating in internal control training sessions

- Regularly reviewing and updating control procedures

9. What questions should be asked about cash management controls?

Key questions regarding cash management controls include:

- Who is responsible for receiving and depositing cash or checks?

- Who performs bank reconciliations, and who reviews them?

- Who has access to bank accounts, and who can authorize payments?

- Who counts cash from fundraisers or donations, and who ensures proper recording and deposit?

10. What are important controls for expenditures and disbursements?

Critical controls for expenditures include determining:

- Who approves expenditures before payment

- Who processes payments (checks or electronic disbursements)

- Who reviews and matches invoices to purchase orders or approvals

- Who authorizes and reviews employee reimbursement requests

11. How should duties be segregated for effective controls?

Effective segregation of duties requires separating these key functions:

- Who authorizes transactions (e.g., payments, donations)

- Who records transactions in the accounting system

- Who handles or has custody of assets (e.g., cash, checks)

- If one person performs multiple roles, who reviews their work

12. What are the principles of internal control?

Internal control principles include:

- Ethical values and integrity

- Oversight responsibility of the board

- Establishing structure, authority, and responsibilities

- Commitment to competence

- Accountability

- Setting appropriate goals

- Identifying and analyzing risks

- Assessing fraud risk

- Implementing control activities through policies and procedures

13. How do controls affect external audits?

External auditors must understand the organization’s internal control system. They use this information to:

- Identify possible types of material misstatement

- Review factors affecting the risk of material misstatement

- Design the timing, scope, and structure of additional audit techniques

An effective internal control system reduces audit risk, potentially allowing auditors to narrow the scope and work with smaller sample sizes.

14. What are IT controls and why are they important?

IT controls protect financial systems and data integrity. Key questions include:

- Who has access to financial software, and how is access granted or revoked?

- Who maintains passwords and system security for financial systems?

- Who ensures financial data is backed up regularly?

- Where are backups stored?

15. What are the benefits of strong controls?

Strong internal controls provide:

- Reduced risk of fraud

- Better and more accurate financial reporting

- Improved operational efficiency

- Enhanced compliance with laws and regulations

- Greater organizational success