Introduction to Fictitious Expenses in Financial Reporting

- Fictitious Expenses in Financial Reporting: Results in companies finanances being financial statment being false and miseading and when truth is revealed shareholders losses money from the articial inflactiong coming out of the stock price. .

- Disclosure:In the realm of financial reporting, the integrity and accuracy of disclosed information are paramount.

- Fictitious Expenses: The insertion of fictitious expenses in financial reporting continues to be a pervasive issue that undermines trust and transparency.

- Consequences: This excruciating guide to security litigation in 2025 aims to shed light on the consequences and legal repercussions associated with such fraudulent practices.

- Non-Existent Costs: Fictitious expenses in financial reporting refer to the deliberate inclusion of non-existent or inflated costs in an organization’s financial statements.

- Deception: These deceptive entries are often used to manipulate earnings, mislead investors, and create a false representation of the company’s financial health.

- Forensic Accounting: The detection of fictitious expenses in financial reporting requires meticulous scrutiny and advanced forensic accounting techniques.

- Financial Records: Regulators and auditors are increasingly employing sophisticated tools to identify discrepancies and anomalies in financial records.

- Severe Ramification: Organizations engaging in these illicit activities are severe, ranging from hefty fines and sanctions to criminal charges against responsible executives.

- Reputational Damage: Can be irreparable, leading to loss of nvestor confidence and significant market value depreciation.

- Security litigation: Securities class actions arising from fictitious expenses in financial reporting is an area of growing concern.

- Remedies: Shareholders and stakeholders who suffer financial losses due to fraudulent reporting practices are increasingly pursuing legal action to seek restitution and accountability.

- Evolving Landscape: The legal landscape in 2025 has evolved to provide more stringent penalties and comprehensive frameworks for addressing securities fraud. Courts are now better equipped to handle complex financial cases, and regulatory bodies have intensified their efforts to combat corporate malfeasance.

- Robust Internal Controls: Organizations must prioritize rrobust internal controls and ethical standards to mitigate the risk of fictitious expenses in financial reporting.

- Audit Procedures: Implementing rigorous audit procedures, fostering a culture of transparency, and ensuring compliance with regulatory requirements are essential steps in safeguarding against fraud.

- Viliglance: As the guide underscores, vigilance and proactive measures are crucial in maintaining the integrity of financial reporting and protecting stakeholders’ interests.or understanding the implications of these fraudulent practices and navigating the legal complexities that arise from them.

Fundamentals of Securities Class Actions

- Securities class action lawsuits serve as a powerful mechanism for investors to seek redress for financial losses caused by corporate misconduct.

- These lawsuits typically arise when a company, its officers, or directors make false or misleading statements, or fail to disclose material information affecting securities value.

- Significant drops in a company’s stock price resulting from misconduct can cause substantial financial losses for investors across the market.

- The class action format allows investors to band together in a single lawsuit rather than pursuing individual claims, streamlining the legal process.

- This collective approach ensures even small investors have a viable means to recover their losses when individually their claims might be too small to litigate.

- Seurities class actions are freqent in case involving ficticious expenses as they are usually the result of the lack of corporate governance and weak internal controls over financial reporting.

- However, the fraud eventually comes out whether it be from a whistleblower or in many circumstances regulations and is followed by a corrective disclosure causing the companies stock price to plummet and shareholders are left holding the bag with massive losses.

The Securities Litigation Process

- Securities litigation begins with identifying potentially fraudulent activities and filing a detailed complaint on behalf of affected investors.

- The complaint must demonstrate that defendants made materially false or misleading statements or omissions that investors relied upon.

- Plaintiffs must establish that these misrepresentations or omissions directly caused their financial losses (loss causation).

- After filing, the complaint undergoes rigorous judicial review, including motions to dismiss and class certification hearings if the court certifies the class, recognizing the group as having legitimate common claims, litigation proceeds to discovery and potentially trial.

Implications for Litigants

- For plaintiffs, these lawsuits offer an opportunity to recover lost investments and hold corporations accountable for misconduct.

- Securities class actions serve as a powerful deterrent against future corporate fraud by establishing legal precedents.

- For defendants, facing securities class actions can result in substantial financial penalties, reputational damage, and increased regulatory scrutiny.

- Companies often must implement more robust compliance programs and improve corporate governance practices following litigation

- Many cases resolve through settlements before trial, with amounts ranging from millions to billions depending on the misconduct’s scale.

An Overview of Ficticious Expenses

- In financial reporting, fictitious expenses are fabricated costs used to manipulate financial statements, either by employees creating fake claims for reimbursement or by management intentionally misrepresenting actual expenses to present a false financial picture.

- Common examples include creating ffake invoices for non-existent vendors or overstating the costs of legitimate business trips.

- This type of fraud, which involves the intentional misstatement of financial information, misleads stakeholders and can have serious legal consequences for a company.

How Fictitious Expenses are Created

Employee-Level Fraud:

- Employees might invent expenses or create fake receipts for items like non-existent equipment, supplies, or even for personal trips.

Management-Level Fraud:

- Management can also manipulate expenses, for example, by moving costs into fixed assets, failing to write down impaired assets, or not reporting sales returns to artificially lower expenses and inflate profits.

Examples of Fictitious Expenses

Fake Invoices:

- Submitting invoices from non-existent vendors for services or goods that were never provided.

Fabricated Travel Expenses:

- Inventing entire business trips, including claims for flights, hotels, and meals, with fake receipts.

Inflated Receipts:

- Overstating the cost of legitimate items like office supplies or meals on the expense report.

- Misleading Stakeholders: The primary goal is to create a false and overly positive impression of a company’s financial health, profits, or performance.

Unauthorized Reimbursement:

- Employees may commit fraud to receive money they are not entitled to.

Meeting Performance Targets:

- Management might use fictitious expenses to temporarily appear more profitable or to conceal poor performance.

Impact of Fictitious Expenses

Financial Statement Fraud:

- Fictitious expenses are a form of accounting fraud that can distort a company’s financial statements

Misleading Investors and Creditors:

- Stakeholders are misled about the company’s true financial situation, which can lead to poor investment decisions.

Legal Consequences:

- Companies and individuals involved in financial reporting fraud can face severe legal penalties.

The Connection Between Corporate Governance, Internal Controls and Securities Litigation

- Having no strong corporate governance framwork and weak internal controls over financial reporting are frequently at the center of securities fraud allegations.

- Fictitious expensea and other accounting irregularities often stem directly from inadequate internal control systems.

- The absence of proper oversight mechanisms creates an environment where executives can manipulate financial statements without detection.

- Companies with deficient audit committee oversight face substantially higher risks of securities class action litigation.

- When internal controls fail, financial misstatements often follow, leading to stock drops when the truth emerges.

- Securities litigation frequently targets the representation that a company maintained “effective internal controls” when evidence suggests otherwise.

- Sarbanes-Oxley certifications regarding iinternal controls create personal liability for executives when those controls prove inadequate.

- Material weaknesses in internal controls over financial reporting serve as early warning signs of potential securities fraud.

- Plaintiff attorneys specifically target companies that have disclosed internal control weaknesses and subsequent financial restatements.

- Settlements in cases involving internal control failures tend to be significantly higher than other securities class actions.

Significance of Securities Class Actions

• Securities litigation plays a crucial role in maintaining the integrity of financial markets.

• These lawsuits provide necessary remedies for investors harmed by corporate fraud.

• The threat of class actions helps ensure companies adhere to high standards of transparency and accountability.

• While legally complex and challenging, securities class actions remain an indispensable tool for protecting investor interests.

• By targeting companies with fictitious expenses resulting from poor corporate governance and internal controls, securities litigation promotes better corporate governance across the market.

Fictitious Expenses in Financial Reporting

Understanding Fictitious Expenses

- Deceptive Financial Entries: Fictitious expenses are misleading entries within financial statements that inaccurately reflect a company’s financial position.

- Manipulation Motives: Companies create these deceptive practices often to iinflate expenses, manipulate earnings, reduce taxable income, or meet specific financial benchmarks.

- •Market Pressure: External pressures to maintain investor confidence or meet market expectations frequently drive this misconduct. Usually the result for weak corporate governance and lack of robust internal controls over financial reporting.

- Intentional Deception: At the core of fictitious expenses is the deliberate intention to deceive stakeholders by presenting an unrealistic picture of financial health.

Methods and Detection Challenges

- Sophisticated Accounting Tactics: Creation methods include recording non-existent transactions, inflating actual expenses, or generating false invoices. The perpetrator is able to get away because in large part is is a company without a strong corporate governance framework and lack of internal controls.

- Detection Difficulties: These practices present significant challenges to auditors, especially in large organizations with numerous transactions.

- Oversight Risks: The complexity of these deceptive practices increases the likelihood of regulatory bodies missing fraudulent activities.

- Professional Vigilance Required: Financial professionals must maintain a keen understanding of accounting principles and vigilantly monitor for anomalies in financial statements.

- Critical Protective Skill: Identifying discrepancies and questioning unusual patterns helps protect organizations from the potentially devastating effects of financial misreporting.

Impact on Financial Statements

• Severe Distortion: Fictitious expenses can dramatically distort a company’s financial statements, leading to misleading conclusions about profitability, cash flow, and overall financial health.

• Investor Deception: These distortions can result in misguided investments and significant financial losses for those relying on accurate financial information.

• Ratio Manipulation: Key financial metrics used by analysts and investors (profit margin, return on assets, earnings per share) can be artificially altered.

• Reputation Damage: Discovery of fictitious expenses typically leads to restatements of financial results, severely damaging company reputation and eroding stakeholder trust.

• Cascading Consequences: Restatements often trigger regulatory scrutiny, legal action, and substantial loss of market value.

Common Types of Fictitious Expenses

• Fake Invoice Creation: Generating invoices for goods or services never received, recording expenses that don’t correspond to actual transactions.

• Legitimate Expense Exaggeration: Overstating costs associated with operations or projects by inflating expenses for materials, labor, or overhead.

• Related-Party Transactions: Engaging in transactions with related parties at artificially inflated prices, creating fictitious expenses through self-dealing.

• Disguised Self-Dealing: Masking these transactions as legitimate business expenses to manipulate financial results for desired outcomes.

Legal Framework and Consequences

• Regulatory Oversight: Laws and regulations mandate accurate and truthful financial statements in most jurisdictions.

• Severe Penalties: Violations can result in substantial fines, sanctions, and criminal charges for individuals involved.

• Sarbanes-Oxley Act: This U.S. legislation exemplifies legal measures enacted to combat financial fraud, imposing strict requirements on public companies.

• Management Accountability: SOX enhances responsibilities of management and auditors in preventing and detecting financial misconduct.

• International Standards: The International Financial Reporting Standards (IFRS) and regional accounting standards provide guidelines ensuring consistency, comparability, and transparency.

• Global Compliance: Companies must adhere to these standards to avoid llegal repercussions and maintain their reputations in global markets.

Corporate Governance and Internal Controls: Root Causes of Fictitious Expenses

- Weak corporate governance structures create an environment where fictitious expenses can flourish without proper oversight or accountability.

- Inadequate board independence often results in insufficient questioning of management’s financial reporting practices and assertions which are signs of lack of corporate govrnance and no internal contrals

- The absence of a robust audit committee with financial expertise overseeing corporate governance and internal contraols can significantly impairs the detection of accounting irregularities and fictitious transactions.

- Deficient internal controls over financial reporting allow unauthorized or fraudulent expense entries to remain undetected throughout accounting cycles.

- Segregation of duties failures enable individuals to both initiate transactions and approve their recording, creating opportunities for fraud.

- Insufficient documentation requirements for expenses make it easier to process and approve fictitious or inflated expenditures. This is almost always the result of the uttler lact of interal contraols.

- Lack of regular reconciliation procedures between supporting documentation and recorded expenses creates blind spots in financial oversight.

Red Flags of Ficticious Expenses

- One employee at one ccompany submitting numeous expense report very close in time

- When it is know that an employee is not on company business but seekes ficticious expense reimbursement for things such as on company business hotel, flight, taxis or other travel-related receipts for dates and times he was known not to be on company time.

- Non pre-approved expenses that employee seeks reimbursement for

Preventative Measures

- Robust Internal Controls: Implem enting comprehensive control systems that separate duties and require multiple approvals for expenses.

- Regular Audit Procedures: Conducting thorough internal and external audits with specific attention to expense verification.

- Whistleblower Protections: Establishing secure channels for emplSecurities Class Action Lawsuits and Regulatory Developments: A Complete Guide [2025]oyees to report suspicious financial activities without fear of retaliation.

- Data Analytics: Employing advanced analytical tools to identify unusual patterns or anomalies in financial data.

- Corporate Governance: Maintaining strong oversight from independent board members and audit committees focused on financial integrity.

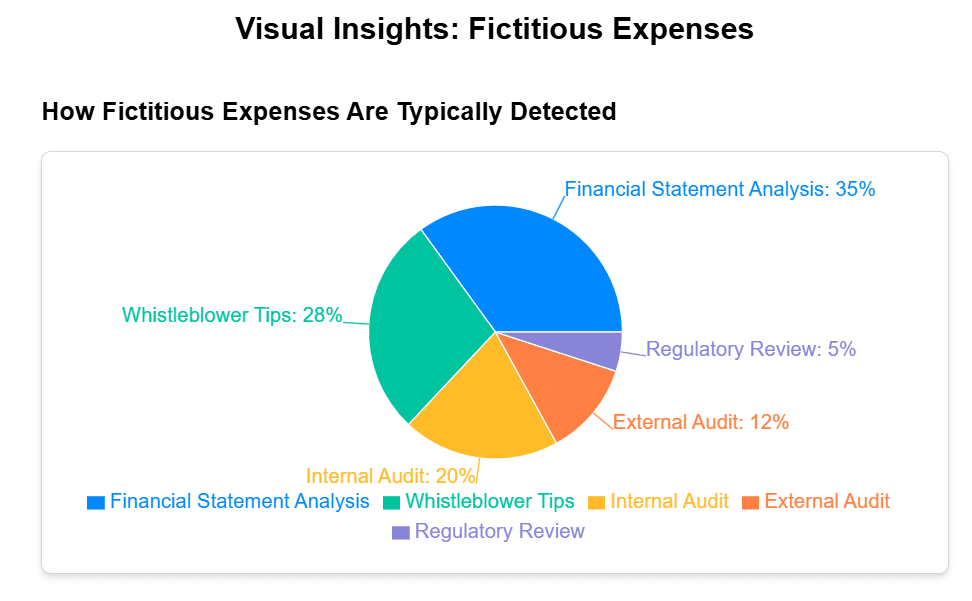

The Role of Auditors in Detecting Fictitious Expenses

- Auditors serve as a critical line of defense by vigorously examining financial records to identify potential fraudulent activity.

- They employ analytical procedures, substantive testing, and examination of supporting documentation to detect unusual patterns that may indicate fictitious expenses.

- Comparison of historical financial data with current performance and industry benchmarks helps auditors identify discrepancies warranting further investigation.

- Evaluating internal controls and risk management practices is a key responsibility of auditors in preventing fictitious expenses.

Case Studies: Notable Security Litigation Involving Fictitious Expenses

• The Enron scandal featured complex accounting schemes to hide debt and inflate profits, leading to bankruptcy and the dissolution of Arthur Andersen.

• WorldCom falsely reported billions in expenses to inflate earnings, resulting in one of the largest bankruptcies in U.S. history and significant regulatory changes.

• Olympus Corporation used fictitious expenses to cover up investment losses, causing severe financial and reputational damage with executives facing criminal charges.

Consequences of Fictitious Expenses for Companies and Executives

• Companies face loss of investor confidence, declining stock prices, and significant reputational damage when fictitious expenses are discovered.

• Financial restatements often lead to increased regulatory scrutiny and potential legal action against the company.

• Executives may face personal liability including fines, sanctions, and imprisonment for their involvement in financial misreporting.

• Companies typically incur substantial financial penalties and must implement costly remedial measures such as overhauling internal controls.

Best Practices for Preventing Fictitious Expenses

• Establish clear policies and procedures for financial reporting, ensuring all transactions are properly authorized and documented.

• Conduct regular audits and reviews of financial records to detect anomalies before they escalate.

• Foster a culture of integrity and accountability through comprehensive training and education programs.

• Implement protected whistleblower channels with assurances of confidentiality and non-retaliation.

• Leverage advanced data analytics and automated monitoring systems to identify unusual patterns in financial data.

The Future of Financial Reporting and Fictitious Expenses

• Increased reliance on automation and artificial intelligence will enhance real-time detection of financial anomalies.

• Blockchain technology shows promise for improving transparency and security of financial transactions through immutable record-keeping.

• The regulatory landscape continues to evolve, emphasizing greater accountability and transparency in financial reporting.

• Companies must adapt their processes and controls to leverage emerging technologies while ensuring compliance with new standards.

Conclusion: Navigating the Risks of Fictitious Expenses

• Understanding and addressing fictitious expenses is essential for maintaining transparency and accountability in financial reporting.

• Learning from past case studies and implementing robust controls helps companies protect themselves from financial fraud.

• Leveraging innovative technological solutions enhances the integrity and accuracy of financial reporting.

• Prioritizing ethical behavior and fostering a culture of transparency safeguards a company’s financial future in an increasingly complex business environment.

FREQUENTLY ASLED QIESTIONS

What is corporate governance and why is it important?

Corporate governance refers to the system of rules, practices, and processes by which a company is directed and controlled. It essentially involves balancing the interests of a company’s many stakeholders, including shareholders, management, customers, suppliers, financiers, government, and the community.

What role does the board of directors play in corporate governance?

The board of directors serves as the primary governing body of a corporation, acting as fiduciaries who represent shareholder interests while ensuring the company’s prosperity.

What are internal controls and how do they relate to corporate governance?

Internal controls are the mechanisms, rules, and procedures implemented by a company to ensure the integrity of financial and accounting information, promote accountability, and prevent fraud. What are fictitious expenses and how do they impact financial statements?

How can companies prevent and detect expense fraud?

Preventing and detecting expense fraud requires a multi-layered approach combining robust controls, technology, and corporate culture.

What triggers securities class action lawsuits related to financial reporting?

Securities class action lawsuits are typically triggered by significant stock price drops following revelations of potential misconduct in financial reporting.

What are internal controls and why are they important for investors?

Internal controls are the policies, procedures, and practices that companies implement to safeguard assets, ensure accurate financial reporting, and promote operational efficiency.

What are the most effective internal controls for preventing expense fraud?

The most effective internal controls for preventing expense fraud combine technological solutions with clear policies and human oversight.

What are fictitious expenses and how are they commonly created in corporate settings?

Fictitious expenses are fraudulent charges recorded in a company’s financial statements that either never occurred or are intentionally misrepresented. These false expenses artificially reduce reported profits, often to evade taxes or hide funds being diverted for personal use.

How can companies detect fictitious expenses before they cause significant damage?

Early detection of fictitious expenses requires a multi-layered approach combining technology, process controls, and human oversight.

How do inadequate internal controls lead to securities class actions?

Internal controls over financial reporting are the specific procedures designed to ensure accurate financial statements.

Contact Timothy L. Miles Today for a Free Case Evaluation