Introduction to Accounting Fraud Exposed

- Accounting Fraud Exposed: Exposing accounting fraud requires familiarity with sophisticated financial engineering tactics that continue to proliferate across modern corporate America, creating substantial risks for securities class action lawsuits and regulatory enforcement actions. These deceptive practices have become increasingly complex as technology advances, making detection more challenging for investors and regulators alike.

- Financial statement fraud: Destroys companies and devastates investor portfolios with alarming frequency. When Tandem Computers issued its earnings restatement in 1983, the immediate 30% stock price collapse served as an early warning of the devastating impact of aggressive revenue recognition policies. Today’s CFOs report that technology represents their primary source of occupational stress, with 41 percent identifying it among their most significant professional challenges. The rapid pace of technological change has forced many financial professionals to prioritize technology adaptation over critical areas like internal controls accounting and staffing considerations.

- Accounting irregularities: Often employ deliberately deceptive techniques designed to obscure an organization’s true financial condition. Revenue manipulation through aggressive revenue recognition and expense understatement represent common pathways to accounting fraud, ranging from aggressive but technically legal practices to outright fraudulent financial reporting. While automated accounting processes can execute tasks within seconds rather than minutes, numerous companies fail to implement adequate internal controls and safeguards against manipulation and misconduct, creating significant vulnerabilities in their financial reporting systems.

- Securities litigation: Frequently follows when these deceptive practices are eventually discovered and disclosed to investors. Companies engaging in financial statement fraud face devastating consequences including regulatory penalties, class action settlements, and permanent reputational damage that can persist for years following resolution. The implementation of robust internal controls becomes crucial in preventing such outcomes and protecting shareholder value.

- This comprehensive analysis exposes the most prevalent accounting machinations, examines real-world corporate fraud cases, and provides six essential safeguards to protect organizations from potential securities class action exposure. Understanding these fraudulent tactics and implementing robust internal controls significantly reduces vulnerability to financial statement fraud while ensuring regulatory compliance with federal securities laws and maintaining market integrity.

Understanding Accounting Fraud in Modern Business

- Recent research reveals that approximately two-thirds of corporate fraud cases in public companies remain undetected, demonstrating the pervasive nature of accounting deception across the business landscape. This alarming statistic underscores the critical importance of strengthening internal controls accounting practices and maintaining vigilant oversight of financial reporting processes.

- The same comprehensive 2023 study uncovered that 41% of companies misrepresent their financial reports annually, excluding simple clerical errors. These findings underscore the critical importance of understanding financial machinations within today’s corporate environment and highlight the urgent need for enhanced internal controls.

Definition and Scope of Financial Machinations

Financial machinations represent deliberate manipulation of financial statements designed to create misleading impressions of corporate financial health, performance, and profitability. These calculated actions target investors, shareholders, regulatory authorities, and the general public through systematic deception. The scope encompasses various accounting documents and typically involves:

- Deliberate falsification of financial records through aggressive revenue recognition

- Creation of misleading corporate transactions designed to circumvent internal controls

- Intentional misrepresentation of financial position to deceive stakeholders

- Manipulation of accounting entries to alter reported outcomes and obscure true performance

- Implementation of aggressive revenue recognition policies that violate accounting standards

- Circumvention of established internal controls accounting procedures

- The financial impact proves substantial, with estimates indicating that fraud could affect as much as 15.6% of firms’ market capitalization. These practices follow a concerning progression that begins with “playing the system,” advances to “beating the system,” and ultimately evolves into “going outside the system” entirely. This progression often starts with aggressive revenue recognition before escalating to more egregious forms of financial statement manipulation.

Common Forms: Earnings Manipulations, Overstated Revenue, Understated Expenses

- Financial statement manipulations manifest through multiple sophisticated techniques that distort corporate performance metrics. The most prevalent deceptive practices that trigger securities litigation include:

Revenue Manipulation Techniques:

- Implementing aggressive revenue recognition policies that record revenue before completing service obligations

- Fabricating entirely fictitious sales transactions and corresponding documentation

- Deliberately misclassifying non-operational income like investment gains or loan proceeds as core business revenue

- Engaging in channel stuffing by shipping excessive inventory to distributors to artificially inflate period-end sales figures

- Orchestrating complex round-tripping arrangements involving coordinated asset sales and repurchases at similar values to create illusory revenue

- Employing aggressive revenue recognition policies that accelerate income recognition ahead of actual economic substance

Expense Manipulation Methods:

- Strategic understatement of operating costs and liabilities to artificially enhance reported profitability

- Improper shifting of current period expenses into future accounting periods through capitalization

- Extending asset depreciation and amortization timelines beyond reasonable economic life

- Deliberately avoiding or delaying necessary asset impairment charges despite clear value deterioration

- Systematically omitting or understating accrued liabilities including employee compensation, tax obligations, and financing costs

- Circumventing established internal controls accounting procedures to manipulate expense timing

Balance Sheet Manipulation Practices:

- Systematic overstatement of asset values while simultaneously understating actual liabilities

- Creating excessive “cookie jar” reserves during profitable periods to smooth future earnings

- Improperly reducing or completely concealing significant liability exposures

- Manipulating off-balance sheet arrangements and subsidiary transactions to hide debt

- Deliberately circumventing internal controls to execute unauthorized balance sheet adjustments

- Structuring complex transactions specifically designed to obscure true financial position

Consider this illustrative example that demonstrates the devastating impact of financial manipulation: A company with actual assets of $1 million and liabilities of $5 million might report inflated assets of $5 million while understating liabilities at only $500,000. This complete distortion of financial reality severely misleads investors regarding the organization’s true liquidity position and operational stability.

Legal vs. Fraudulent Accounting Practices

A critical distinction exists between aggressive but legal accounting methods and outright fraudulent practices. Not all financial manipulations constitute illegal fraud or violate securities regulations, though both can trigger securities litigation:

Legal Aggressive Accounting:

- Leverages flexibility and judgment allowed within established accounting standards

- Encompasses strategic earnings management and income smoothing techniques

- Involves calculated timing of investment dispositions, inter-division expense allocations, and asset sales

- Operates within technical compliance of Generally Accepted Accounting Principles (GAAP)

- May receive qualified auditor approval despite questionable ethical implications

- Tests the boundaries of aggressive revenue recognition without crossing into fraud

Fraudulent Accounting:

- Involves intentional deception that exceeds permissible accounting standard boundaries

- Includes deliberate falsification of financial records and supporting documentation

- Directly violates federal securities laws, regulations and disclosure requirements

- Often motivated by management incentives tied to stock price and earnings targets

- Frequently involves executive collusion and systematic override of internal controls

- Creates material misstatements that require eventual restatement when discovered

The primary catalyst driving these manipulative practices stems from intense financial pressure created by:

- Executive compensation structures directly tied to reported financial metrics

- Flexibility in accounting standards that enables aggressive interpretation

- Inherent difficulty outsiders face in detecting sophisticated manipulation schemes

- Weak internal controls accounting systems that fail to prevent or detect abuse

- Corporate cultures that prioritize short-term results over sustainable practicesAsset Misappropriation and Internal Controls: A Step-By-Step Essential Guide to Protecting Your Business [2025]

- Market expectations that incentivize aggressive or fraudulent reporting

Many fraudulent operations involve coordinated manipulation across multiple financial statement areas, creating an intricate web of deception designed to artificially enhance reported performance while evading detection by auditors and regulators.

How Financial Statement Fraud Happens

Financial statement fraud inflicts median losses of USD 593,000 per incident, making it the most expensive category of occupational fraud despite occurring in only 9% of cases. Understanding how these deceptive practices materialize helps organizations identify and prevent potential manipulation before it damages their financial standing and triggers costly securities litigation.

Understating Expenses to Inflate Profits

Companies frequently manipulate expenses through various techniques designed to artificially boost reported earnings. Common approaches include:

- Improper capitalization of normal operating costs

- Extending depreciation periods beyond reasonable asset life

- Failing to record expenses in the proper period

- Understating warranty and return obligations

- Manipulating inventory costs and valuations

- Circumventing internal controls to delay expense recognition

These manipulative practices often start subtly through aggressive revenue recognition before escalating to more egregious forms of financial statement fraud that eventually trigger regulatory investigations and securities litigation.

- Expense manipulation serves as a primary method for artificially improving bottom-line earnings, with companies employing increasingly sophisticated techniques to understate costs and create misleading financial portraits. This practice directly violates fundamental internal controls accounting principles and often triggers extensive securities litigation when discovered.

- Improper capitalization of expenses represents one of the most egregious forms of accounting fraud, occurring when companies deliberately record operating expenses as fixed assets rather than immediate costs. This manipulation directly inflates net income figures by spreading costs over multiple future periods instead of recognizing them immediately.

- A notorious example is WorldCom, which employed manual journal entries to inappropriately capitalize billions in operating expenses as fixed assets, circumventing established internal controls to inflate net income by USD 3.80 billion. Similarly, HealthSouth Corporation utilized identical tactics, systematically capitalizing routine expenses to inflate earnings by USD 2.80 billion over six years through deliberate override of internal control systems.

- Falsified timing of expenses involves deliberately postponing current period expenses to later accounting periods, a practice that directly affects bottom-line earnings and helps companies meet specific performance targets. This manipulation of expense timing frequently coincides with aggressive revenue recognition to create a compounded effect on reported profits. Companies execute this fraud through multiple sophisticated mechanisms:

- Shifting expenses between accounting periods to artificially smooth earnings trajectories

- Improperly extending depreciation or amortization periods far beyond reasonable economic estimates

- Creating excessive initial reserves and strategically reducing them in later periods (known as “cookie-jar reserves”)

- Deliberately delaying recognition of known expenses until future reporting periods

- Manipulating accrual calculations to understate current period obligations

- Systematically misclassifying operating expenses as extraordinary or non-recurring items

Inventory manipulation provides another pathway for fraudulent earnings inflation, as companies overstate inventory values to directly understate cost of goods sold, thereby reducing reported expenses and increasing profits. This practice often accompanies aggressive revenue recognition policies to create artificially improved margins. Conversely, companies seeking to decrease profits might strategically understate inventory to increase expenses, depending on their specific financial objectives and tax planning strategies.

Channel Stuffing and Premature Revenue Recognition

- Premature revenue recognition represents the most common form of accounting manipulation as companies aggressively seek to inflate earnings by reporting revenue before it is legitimately earned. These schemes typically accelerate revenue recognition to meet quarterly or year-end targets that analysts and investors expect, often bypassing established internal controls designed to prevent such practices.

Channel stuffing involves deliberately overloading distribution channels with more products than retailers can realistically sell, artificially inflating sales figures through several coordinated tactics that frequently circumvent internal controls accounting safeguards:

- Offering unusually deep discounts or special incentives to distributors near quarter-end

- Providing extended payment terms that make purchases artificially attractive

- Shipping excessive inventory at period ends without legitimate customer demand

- Creating undisclosed side agreements to repurchase goods if they remain unsold

- Manipulating shipping documentation to record sales in incorrect periods

- Pressuring distributors to accept inventory beyond their normal capacity

A prominent example is Bristol-Myers Squibb, which paid USD 150 million to settle charges after it inflated revenues by USD 1.50 billion through systematic channel stuffing. The pharmaceutical giant aggressively pushed excessive products to wholesalers ahead of actual demand and improperly recognized revenue upon shipment rather than when products reached end customers, demonstrating how aggressive revenue recognition practices can lead to significant regulatory penalties.

Additional premature revenue recognition techniques demonstrate the creativity of financial manipulators in circumventing established control systems:

- Recording revenue before completing required services or delivering products to customers

- Manipulating “percentage of completion” calculations for long-term projects to accelerate income

- Implementing sophisticated “round-tripping” schemes where products are sold with undisclosed agreements to repurchase them

- Backdating sales agreements or keeping books open past period end to capture additional transactions

- Creating complex side agreements that modify standard sales terms

- Manipulating shipping terms to accelerate revenue recognition timing

- Warning signs of these deceptive practices include unusually large percentages of revenue recorded at period ends and transactions with unusual payment terms that deviate significantly from industry standards. Companies exhibiting these patterns often face increased scrutiny from regulatory bodies and heightened risk of securities litigation.

Off-Balance-Sheet Liabilities and Their Concealment

- The systematic concealment of liabilities represents another sophisticated form of financial manipulation that frequently circumvents standard internal controls. This practice involves complex structured transactions specifically designed to hide debt obligations and other liabilities from investors and regulators.

- Off-balance-sheet activities represent a sophisticated form of financial manipulation that companies employ to obscure their true financial obligations from stakeholders. These activities encompass loan commitments, letters of credit, and revolving underwriting facilities strategically structured to hide liabilities while artificially enhancing reported financial metrics.

- The manipulation becomes particularly concerning when companies pair these practices with aggressive revenue recognition policies, creating a dangerous combination that misleads investors about the organization’s true financial health. These Best Practices for Corporate Governance to Mitigate Securities Fraud [2025]transactions distort key financial ratios since revenue appears on income statements while related obligations remain concealed from balance sheets, circumventing established internal controls accounting standards.

Concealment methods for off-balance sheet liabilities have evolved into highly sophisticated schemes that demonstrate the complex nature of modern financial deception:

- Creating special purpose entities (SPEs) designed with intricate ownership structures and complex governance mechanisms specifically to hide debt or underperforming assets from primary financial statements. These entities often operate just beyond the technical threshold for consolidation while maintaining de facto control through sophisticated contractual arrangements.

- Employing deliberately complex financial instruments structured with multiple embedded derivatives, contingent obligations, and intricate trigger mechanisms. These instruments are intentionally designed to confuse investors and obscure their true economic substance, often exploiting gaps in internal controls systems.

- Utilizing related-party transactions executed through elaborate networks of affiliated entities to transfer profits or losses in ways that benefit the reporting company while concealing the true nature of relationships and obligations. These transactions frequently involve complex pricing mechanisms and non-standard terms that make detection particularly challenging.

- The most straightforward yet equally deceptive technique involves deliberately failing to record legitimate liabilities that should appear on financial statements. This direct manipulation inflates key metrics like equity, assets, or net earnings by systematically understating actual obligations. Companies often justify these omissions through aggressive interpretation of accounting standards or by claiming immateriality, demonstrating how aggressive revenue recognition policies can extend beyond revenue manipulation.

Fraud indicators associated with concealed liabilities have become increasingly sophisticated, requiring enhanced vigilance from stakeholders:

- Discovery of unrecorded invoices during audit procedures, particularly those deliberately held in separate files or locations

- Liability estimates that prove difficult to corroborate through standard verification procedures

- Direct management instructions to accounting personnel to omit specific transactions from official records

- Complex transaction structures that appear designed primarily to achieve accounting objectives rather than serve legitimate business purposes

- Unusual patterns in vendor payments or unexplained gaps in transaction sequences

- Significant discrepancies between cash flows and reported earnings

- Complex related-party transactions with non-standard terms or unusual pricing mechanisms

Companies engaging in substantial off-balance-sheet activities present heightened manipulation risk due to reduced transparency and compromised accountability. The complexity of these arrangements often overwhelms standard internal controls, creating opportunities for sophisticated financial engineering that obscures true obligations.

Proper examinations of off-balance-sheet activities must incorporate comprehensive reviews across multiple dimensions:

- Evaluation of policy adequacy and consistency with industry standards

- Assessment of internal controls specifically designed to monitor and report off-balance-sheet exposures

- Detailed analysis of credit quality and risk profiles for off-balance-sheet items

- Review of board oversight mechanisms and approval processes

- Examination of documentation supporting complex structured transactions

- Assessment of disclosure adequacy and compliance with regulatory requirements

- Analysis of economic substance versus accounting form for complex arrangements

These examinations become particularly critical given the potential for devastating securities class action lawsuits when hidden liabilities eventually surface. The market reaction to such disclosures typically triggers significant stock price declines as investors reassess company valuations based on newly revealed obligations. Legal consequences often extend beyond civil litigation to include regulatory enforcement actions and potential criminal charges for senior executives involved in deliberate concealment schemes.

VARIOUS FRAUD SCHEMES BY TYPE

| Scheme Type | Description | Example |

| Fictitious Revenue | Recording non-existent sales through false documentation and phantom customers | Creating counterfeit sales contracts or engaging in fraudulent bill-and-hold arrangements that lack economic substance |

| Premature Revenue Recognition | Recognizing revenue before satisfying essential accounting criteria | Accelerating revenue recognition before completing contracted service obligations or product delivery requirements |

| Channel Stuffing | Forcing excessive inventory into distribution channels to artificially inflate sales | Providing unusual incentives to distributors to accept unnecessary inventory levels that exceed reasonable demand |

| Asset Overstatement | Deliberately inflating reported asset values through accounting manipulation | Recording phantom inventory or applying inadequate depreciation to overstate asset carrying values |

| Liability Concealment | Hiding financial obligations through improper accounting treatments | Deliberately understating debt levels or warranty obligations through accounting manipulation |

| Material Omissions | Withholding critical information required for informed investment decisions | Failing to disclose significant related party transactions or contingent liabilities |

| Journal Entry Manipulation | Falsifying accounting records through improper manual adjustments | Making unsupported last-minute entries near reporting deadlines to manipulate results |

THE SECURITIES LITIGATION PROCESS

| Filing the Complaint | A lead plaintiff files a lawsuit on behalf of similarly affected shareholders, detailing the allegations against the company. |

| Motion to Dismiss | Defendants typically file a motion to dismiss, arguing that the complaint lacks sufficient claims. |

| Discovery | If the motion to dismiss is denied, both parties gather evidence, documents, emails, and witness testimonies. This phase can be extensive. |

| Motion for Class Certification | Plaintiffs request that the court to certify the lawsuit as a class action. The court assesses factors like the number of plaintiffs, commonality of claims, typicality of claims, and the adequacy of the proposed class representation. |

| Summary Judgment and Trial | Once the class is certified, the parties may file motions for summary judgment. If the case is not settled, it proceeds to trial, which is rare for securities class actions. |

| Settlement Negotiations and Approval | Most cases are resolved through settlements, negotiated between the parties, often with the help of a mediator. The court must review and grant preliminary approval to ensure the settlement is fair, adequate, and reasonable. |

| Class Notice | If the court grants preliminary approval, notice of the settlement is sent to all class members, often by mail, informing them about the terms and how to file a claim. |

| Final Approval Hearing | The court conducts a final hearing to review any objections and grant final approval of the settlement. |

| Claims Administration and Distribution | A court-appointed claims administrator manages the process of sending notices, processing claims from eligible class members, and distributing the settlement funds. The distribution is typically on a pro-rata basis based on recognized losses. |

Real-World Corporate Fraud Cases: When Accounting Fraud Trigger Securities Litigation

Corporate scandals throughout recent decades provide sobering examples of how sophisticated accounting fraud can devastate investor portfolios and trigger massive securities class action lawsuits. These cases offer critical insights into the devastating consequences awaiting companies that engage in deliberate financial statement fraud and the inevitable regulatory enforcement actions that follow.

1. IBM’s Share Buyback Strategy and EPS Inflation

IBM executed one of corporate America’s most extensive share repurchase programs between 1995 and 2019, allocating an extraordinary $201 billion to repurchase its own stock. The technology giant consistently dedicated approximately $8 billion annually to this financial engineering strategy, demonstrating how sophisticated financial manipulation can occur even within seemingly legitimate corporate actions.

The Manipulation Scheme:

- The corporation’s approach to earnings manipulation exhibited several concerning elements. While repurchasing approximately 67 million shares annually, IBM simultaneously issued about 18.3 million shares each year for stock-based compensation and purchase plans. This pattern raised significant questions about the true economic substance of the buyback program and its impact on reported earnings per share.

- Despite this massive financial commitment, IBM’s market value declined by more than 40% since 1999. Had these funds merely maintained pace with inflation, IBM’s stock price would have reached approximately $384 per share by 2023 instead of hovering around $164, highlighting the potential long-term value destruction from aggressive financial engineering strategies.

Funding Through Pension Raids

- IBM’s aggressive financial engineering strategy relied heavily on controversial pension plan manipulations that raised serious concerns about corporate governance and internal controls. Between 1995 and 2012, the company conducted five separate pension plan raids that diverted substantial funds toward share repurchases while potentially compromising long-term retirement security. These raids in 1995, 1999, 2008, 2009, and 2012 demonstrated how companies could exploit pension accounting rules to generate artificial earnings through aggressive revenue recognition practices.

- The pension raids involved complex actuarial assumptions and accounting maneuvers that allowed IBM to tap into pension surpluses while maintaining technical compliance with regulations. However, these actions drew intense scrutiny from employee advocacy groups and regulatory bodies concerned about the potential long-term impact on retiree benefits. The company’s internal controls accounting systems failed to adequately flag the risks associated with these aggressive financial strategies.

- This sophisticated financial engineering enabled IBM to maintain artificial earnings growth even as underlying business performance stagnated. By dramatically reducing the outstanding share count through buybacks funded by pension raids, IBM created an illusion of earnings per share growth that masked concerning operational trends. The company’s aggressive revenue recognition policies combined with pension-funded buybacks to paint a misleading picture of financial health.

The Financial Impact:

- The stark disconnect between IBM’s revenue growth and share count reduction reveals the extent of this financial manipulation. Over the fourteen-year period from 2000 to 2014, IBM’s total revenue grew by a mere 5.6% – reflecting essentially flat business performance when adjusted for inflation. However, during this same period, the company’s aggressive buyback program slashed the outstanding share count by more than 45%, creating artificial earnings per share growth that didn’t reflect genuine business improvement.

- This dramatic share count reduction allowed IBM to report consistent earnings per share growth even as revenues stagnated and organic business growth proved elusive. The company’s sophisticated deployment of pension assets to fund buybacks demonstrated how internal controls weaknesses could enable potentially destructive financial engineering. While technically legal, these practices raised serious concerns about corporate governance and long-term sustainability.

- The eventual suspension of IBM’s buyback program in 2019 following the Red Hat acquisition marked a significant shift in capital allocation strategy. This change came amid mounting scrutiny of the company’s aggressive financial engineering and growing recognition that buybacks funded through pension raids had potentially compromised long-term value creation. The focus on debt repayment signaled an important pivot toward more sustainable financial management.

The IBM case highlights several critical lessons about aggressive financial engineering and the importance of robust internal controls accounting:

- Share buybacks funded through pension raids can create artificial earnings growth that masks underlying business challenges

- Aggressive financial engineering strategies may deliver short-term EPS growth while potentially destroying long-term shareholder value

- Weak internal controls around pension accounting and capital allocation can enable potentially destructive financial manipulation

- Companies pursuing aggressive buybacks warrant particularly close scrutiny regarding funding sources and sustainability

- Pension accounting rules can be exploited to generate artificial earnings through sophisticated financial engineering

- The combination of stagnant revenue growth and massive share count reduction should trigger enhanced investor vigilance

- Suspension of long-running buyback programs may signal recognition of unsustainable financial engineering

The eventual market recognition of IBM’s aggressive financial engineering triggered significant shareholder losses as the stock price declined over 40% from 1999 levels. This outcome demonstrates how sophisticated manipulation of pension assets and share counts can ultimately destroy rather than create shareholder value when used to mask operational challenges rather than reflect genuine business improvement.

The IBM case remains a cautionary tale about the risks of aggressive financial engineering and the critical importance of robust internal controls around pension accounting and capital allocation decisions. While share buybacks can be legitimate tools for returning capital to shareholders, funding them through pension raids while masking stagnant business performance ultimately proved destructive to long-term shareholder value.

- The lawsuit alleged that during 2006, Motorola’s handset business engaged in two primary accounting machinations that demonstrated serious weaknesses in internal controls accounting:

- Deliberately concealing the company’s inability to deliver promised 3G handsets due to persistent chip supply problems from Freescale Semiconductor, despite having clear knowledge of these material production constraints. This lack of disclosure violated SEC requirements for transparent reporting of known business risks and manufacturing challenges that could impact financial performance.

- Orchestrating complex “sham intellectual property transactions” with Freescale and Qualcomm that violated generally accepted accounting principles, specifically designed to obscure the severe financial impact of the 3G product failures through aggressive revenue recognition. These transactions lacked economic substance and were structured primarily to create artificial revenue streams.

- The lawsuit alleged that during 2006, Motorola’s handset business engaged in two primary Long-term Market Impact factors that highlighted systemic failures in internal controls:

- These accounting irregularities occurred during a pivotal period when Motorola’s handset business held dominant market share and industry leadership. The company’s position as a market leader made the deceptive practices particularly egregious, as investors relied heavily on Motorola’s financial statements and disclosures to assess both company-specific and broader industry trends.

- Following the revelation of these aggressive revenue recognition policies, Motorola’s handset division experienced an irreversible decline, never regaining its former market position. This permanent damage to competitive positioning and investor confidence demonstrates how accounting fraud can devastate even seemingly invincible market leaders.

- These accounting irregularities allegedly occurred during a critical period when Motorola’s handset business held market dominance. Following these events, Motorola’s handset division never regained its former market position, demonstrating how The Broader Implications extend beyond any single company:

- These corporate fraud cases illustrate several key patterns regarding accounting machinations that occur consistently across industries and time periods, affecting companies regardless of size or market prominence:

- Weak internal controls frequently enable aggressive accounting practices to persist undetected until significant damage occurs

- Complex revenue recognition schemes often mask deteriorating business fundamentals

- Material omissions regarding known business risks violate core disclosure obligations

- Artificial transactions lacking economic substance are commonly used to obscure operational challenges

- Market-leading companies are not immune from engaging in deceptive practices

- The discovery of accounting fraud typically triggers both regulatory investigations and private securities litigation

- Reputational damage from accounting scandals often proves permanent and irreversible

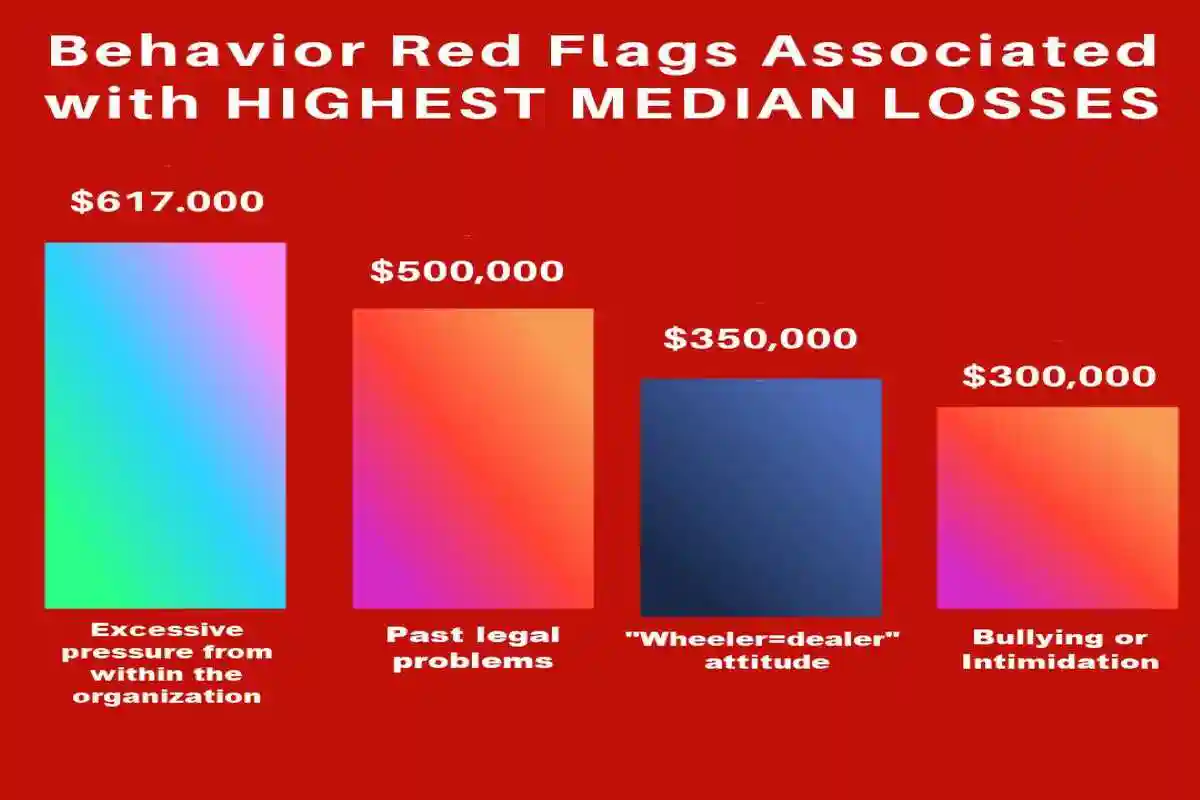

The Eight Biggest Triggers to Securities Litigation

| Trigger | Description |

| Asset Valuation Manipulation | This sophisticated deception involves deliberately misrepresenting asset values to create misleading impressions of financial health. Common techniques include overstating inventory values, manipulating asset impairment calculations, and applying improper capitalization policies. The eventual discovery of inflated asset values typically triggers substantial write-downs that devastate shareholder value. |

| Off-Balance-Sheet (OBS) Schemes | While some OBS arrangements serve legitimate business purposes, deceptive schemes deliberately hide liabilities and risks from shareholders. These complex structures frequently involve special purpose entities, synthetic leases, and other vehicles designed to circumvent proper accounting disclosure requirements. The concealment of significant obligations creates misleading impressions of financial strength. |

| Material Omission | The deliberate withholding of information that shareholders need for informed investment decisions represents a particularly dangerous form of deception. Common examples include failing to disclose related party transactions, contingent liabilities, and regulatory investigations. These omissions prevent investors from accurately assessing business risks and financial condition. |

| Timing Manipulation | This trigger involves deliberately manipulating the timing of revenue and expense recognition to create artificial impressions of financial performance. Companies frequently accelerate revenue recognition while deferring expense recognition through aggressive revenue recognition policies designed to inflate reported profits. This manipulation distorts period-to-period comparability. |

| Cookie Jar Reserves | This deceptive practice involves creating excessive reserves during strong periods that management can later release to artificially smooth earnings. The deliberate manipulation of reserve estimates enables companies to meet analyst expectations even when actual business performance falls short. This practice misleads shareholders about true financial performance. |

| Expense Capitalization | The improper capitalization of costs that should be expensed represents another common trigger for securities litigation. Companies frequently capitalize normal operating costs to artificially boost reported profits. This manipulation creates misleading impressions of profitability while deferring expense recognition to future periods. |

Six Essential Safeguards to Prevent Securities Litigation and Regulatory Enforcement

Corporate fraud costs organizations approximately 5% of annual revenues globally, translating into trillions of dollars in losses each year and spawning countless securities class action lawsuits filed by damaged investors. Protecting organizations from these devastating consequences requires implementing systematic safeguards that create multiple layers of defense against financial statement fraud and accounting irregularities.

- Implementing Strong Internal Controls

Internal controls serve as the primary defense mechanism against fraudulent activities that trigger securities litigation. Well-designed control systems must establish clear procedures, enforce proper segregation of duties, require multiple levels of authorization, and promote accountability throughout all organizational levels. Key elements include:

- Organizations must perform comprehensive risk assessments to identify areas most vulnerable to manipulation and fraud. These risks should be documented within a detailed risk assessment matrix and ranked based on both likelihood of occurrence and potential financial impact. Following this systematic evaluation, organizations should implement targeted preventive controls addressing high-priority risks:

- Rigorous physical controls over assets and sensitive financial information

- Strict IT access controls implementing the principle of least privilege

- Mandatory regular account reconciliation comparing internal records against external statements

- Comprehensive training and testing programs for all financial personnel

- Clear policies regarding revenue recognition and contract documentation

- Multiple levels of review for significant transactions

- Regular monitoring of key performance indicators for anomalies

- The Association of Certified Fraud Examiners consistently reports that approximately half of all frauds occur due to inadequate internal controls. Companies that implement and maintain robust control systems significantly reduce their exposure to both regulatory enforcement actions and securities class action lawsuits.

Enforcing Segregation of Duties in Finance Teams

Enforcing Segregation of Duties in Finance Teams

- Segregation of duties represents a foundational internal control mechanism that prevents fraudulent activities by ensuring no single individual maintains complete control over critical financial processes. This essential principle strategically divides key responsibilities among multiple employees, establishing natural verification points that detect potential errors or deliberate manipulation before they escalate into serious accounting fraud requiring regulatory intervention or triggering securities litigation.

- Critical operational areas requiring robust duty segregation encompass cash handling procedures, procurement processes, information system access privileges, and financial record maintenance responsibilities.

- Organizations must implement clear policies ensuring different individuals handle various aspects of cash-related activities – from initial collection and deposits to recording transactions and performing reconciliations. Similarly, the purchasing cycle should separate personnel who initiate purchase requests from those who approve expenditures and process vendor payments. This separation creates natural checks and balances that make fraudulent schemes significantly more difficult to execute without detection.

- For smaller organizations facing resource constraints that complicate traditional segregation approaches, implementing compensating controls becomes essential. These alternative protective measures should include:

- Enhanced executive oversight with detailed transaction review procedures

- Mandatory job rotation programs that prevent excessive concentration of knowledge

- Regular independent reviews of high-risk transactions and processes

- Cross-training programs ensuring multiple employees understand key procedures

- Documentation requirements mandating detailed audit trails

- Surprise audits and spot checks of financial activities

- Regular assessment and updating of internal controls accounting procedures

These compensating mechanisms help prevent the dangerous consolidation of financial authority that often enables fraudulent activities and subsequent securities litigation.

Conducting Regular Internal Audits

Regular internal audits provide crucial independent assurance regarding the effectiveness of governance structures, risk management protocols, and compliance programs. These systematic evaluations serve as an early warning system to identify potential control weaknesses before they develop into serious fraud schemes that attract unwanted regulatory scrutiny and trigger costly securities class action lawsuits.

- Effective internal audit processes must follow a structured four-phase approach:

- Planning Phase: Define clear objectives, establish audit scope, identify key risk areas

- Fieldwork Phase: Execute detailed testing using comprehensive assessment tools

- Reporting Phase: Document findings with actionable recommendations

- Follow-up Phase: Monitor implementation of recommended improvements

- The internal audit function should maintain particular focus on areas prone to aggressive revenue recognition schemes, including:

- Contract terms and documentation supporting revenue recognition

- Timing of revenue recognition relative to delivery obligations

- Treatment of complex transactions with multiple elements

- Related party transactions and unusual payment terms

- Channel partner relationships and inventory management

- Reserve methodologies and estimation processes

- Corporate governance effectiveness improves substantially through regular internal audits that evaluate risk management protocols, strengthen control processes, and enhance oversight procedures. This proactive approach helps organizations identify and address potential issues before external auditors discover them during their annual reviews, thereby avoiding regulatory complications that frequently precede costly securities litigation.

Using Automated Accounting Processes to Reduce Manual Errors

Manual accounting procedures create significant regulatory compliance vulnerabilities through inconsistent application of standards and incomplete documentation trails. Modern automation solutions build compliance requirements directly into daily workflows by:

- Enforcing standardized procedures across all transactions

- Creating detailed audit trails automatically

- Preventing unauthorized actions through system controls

- Maintaining segregation of duties through software architecture

- Generating exception reports for management review

- Ensuring consistent application of accounting policies

- Facilitating accurate and timely financial reporting

- Advanced automation systems provide essential protective features including:

- Role-based access controls that strictly limit user capabilities

- Comprehensive audit logs recording all system activities

- Configurable validation rules preventing unauthorized actions

- Automated workflow approvals enforcing proper authorization

- Real-time monitoring of suspicious patterns or anomalies

- Integration with compliance monitoring systems

- Regular testing of control effectiveness

- Recent research from Gartner indicates that finance departments implementing Robotic Process Automation in financial reporting processes can eliminate approximately 25,000 hours of avoidable rework annually. This automation significantly reduces the reported 59% of accountants who make “several errors per month,” thereby decreasing the risk of accounting irregularities that often trigger investor lawsuits.

Ensuring Transparent Financial Disclosures

- Transparent financial reporting requires organizations to disclose all material information to stakeholders in clear, accessible formats that facilitate understanding. This fundamental practice builds essential investor trust while reducing exposure to securities class action lawsuits alleging material misrepresentations or omissions in financial statements.

- Organizations must prioritize honest, accountable reporting while avoiding creative accounting tactics that may temporarily boost performance metrics but ultimately destroy long-term credibility. Key considerations include:

- Balancing regulatory compliance requirements with readability

- Using plain language to explain complex transactions

- Providing appropriate context for significant events

- Including relevant non-GAAP measures with clear reconciliations

- Maintaining consistency in reporting methodologies

- Addressing known risks and uncertainties directly

- Ensuring completeness of all required disclosures

- Recent market research indicates that over 80% of American investors now consider corporate transparency more important than ever before in making investment decisions. Organizations that maintain transparent disclosure practices benefit from:

- Enhanced stakeholder trust and confidence

- Reduced risk of regulatory investigations

- Lower cost of capital through improved credibility

- Stronger relationships with investors and analysts

- Decreased exposure to securities litigation

- Improved governance practices and controls

- Greater long-term market value stability

Establishing a Whistleblower Policy

Effective whistleblower programs serve as a critical line of defense against financial misconduct by creating secure channels for employees to report suspected violations of securities laws, accounting standards, and internal controls. These comprehensive reporting systems build organizational trust by educating employees about compliance expectations, providing multiple secure reporting mechanisms, and ensuring robust legal protections that shield whistleblowers from workplace retaliation.

- Essential program elements must include detailed written policies that clearly outline:

- Protected reporting activities and covered violations

- Multiple confidential reporting channels accessible 24/7

- Options for anonymous reporting through third-party hotlines

- Mandatory investigation timelines with 7-day acknowledgment

- Anti-retaliation protections and enforcement procedures

- Regular employee training and awareness programs

- Clear escalation protocols for serious allegations

- Documentation requirements for all reported concerns

- Regular testing of reporting system effectiveness

- Annual review and updates of program policies

- Research indicates that fear of retaliation remains the primary barrier preventing employees from reporting suspected accounting fraud and aggressive revenue recognition policies. Organizations that implement robust confidential reporting systems experience:

- 50% higher fraud detection rates

- 33% reduction in median fraud losses

- 45% shorter fraud scheme duration

- Significantly decreased securities litigation exposure

- Enhanced regulatory compliance outcomes

- Stronger ethical corporate culture

- Improved employee trust and engagement

- Risk mitigation through these comprehensive safeguards creates an essential early warning system that helps organizations detect and address potential violations before they escalate into serious regulatory enforcement actions or trigger devastating securities class action lawsuits. Companies with effective whistleblower programs demonstrate their commitment to ethical conduct while protecting long-term shareholder value.

Corporate Governance and Regulatory Compliance: The Final Defense Against Securities Litigation

- Robust corporate governance frameworks represent the ultimate barrier against financial misrepresentation and aggressive revenue recognition. Organizations that maintain comprehensive oversight structures can identify potential compliance risks early, before they develop into serious regulatory violations that frequently trigger costly securities class action lawsuits.

Board Oversight and Audit Committee Responsibilities

Board members establish the critical “tone at the top” by demonstrating zero tolerance for fraud and unethical conduct at every organizational level. This message must be consistently reinforced through:

- Regular written communications to all employees

- Comprehensive ethics and compliance policies

- Mandatory training programs at all levels

- Swift disciplinary action for violations

- Public commitment to transparency

- Active engagement in oversight activities

Board Structure with Both Executive and Independent Directors

The board structure must include both executive and independent directors, with independent members providing crucial objective oversight of management activities and potential conflicts of interest. Regular board evaluation of internal controls accounting effectiveness helps ensure early detection of control weaknesses that could enable fraudulent activities.

- Audit committees function as the cornerstone of financial oversight within corporate governance structures by providing independent review of:

- Financial reporting processes and controls

- Internal audit activities and findings

- External auditor relationships

- Risk management programs

- Compliance monitoring systems

- Whistleblower reports and investigations

- Management’s accounting judgments

- Significant transactions and estimates

The Sarbanes-Oxley Act requires all public companies to maintain audit committees composed entirely of independent directors, including at least one designated financial expert. This independence requirement helps ensure objective oversight of financial reporting practices and internal controls, reducing the risk of securities litigation.

SEC Enforcement and Federal Securities Laws

The Securities and Exchange Commission (SEC) serves as the primary federal agency responsible for protecting investors and maintaining fair, efficient markets through robust enforcement of securities laws. SEC enforcement activities focus on:

Securities exchanges and broker-dealers

- Market manipulation prevention

- Trading practice oversight

- Registration requirements

- Financial responsibility rules

- Customer protection standards

Investment advisors and mutual funds

- Fiduciary duty compliance

- Fee disclosure requirements

- Portfolio management practices

- Marketing and advertising rules

- Custody requirements

Corporate financial disclosures

- Reporting accuracy and completeness

- Internal controls effectiveness

- Aggressive revenue recognition schemes

- Material misstatements or omissions

- Insider trading violations

Regulatory compliance monitoring

- Industry examinations and inspections

- Risk assessment programs

- Investigation procedures

- Enforcement protocols

- Penalty determinations

- Recent SEC enforcement statistics: Demonstrate the agency’s aggressive pursuit of securities law violators, with fiscal year 2022 resulting in record penalties exceeding $6.44 billion. This unprecedented level of regulatory enforcement reflects the SEC’s commitment to maintaining market integrity and protecting investors from financial misrepresentation through aggressive revenue recognition schemes and other forms of accounting fraud.

Sarbanes-Oxley Act Compliance Requirements

- Following major corporate scandals, the Sarbanes-Oxley Act introduced transformative reforms that fundamentally reshaped financial reporting and corporate governance practices. The legislation established stringent new requirements designed to prevent aggressive revenue recognition schemes and strengthen internal controls accounting. Organizations that achieve comprehensive SOX compliance realize multiple strategic benefits that enhance shareholder value and reduce exposure to costly securities litigation:

- Enhanced Financial Reporting Standards: Companies must now adhere to rigorous financial reporting requirements and maintain robust internal controls frameworks, which significantly improves transparency and bolsters investor confidence. Organizations that fully comply with Sarbanes-Oxley mandates operate more effectively due to enhanced control over financial processes, regulatory compliance, and operational risk management. The legislation’s emphasis on accountability has dramatically reduced instances of aggressive revenue recognition policies that previously enabled widespread financial manipulation.

- Key SOX Provisions include mandatory CEO and CFO certification of financial statements under Section 302, which creates direct personal liability for senior executives who knowingly certify misleading financial reports. Section 404 requires establishment of comprehensive internal controls frameworks with annual testing and reporting on control effectiveness. Section 301 strengthens auditor independence requirements to prevent conflicts of interest that historically enabled aggressive revenue recognition schemes to escape detection. Since implementation, the Sarbanes-Oxley Act has substantially reduced instances of corporate fraud and accounting scandals, providing stronger protection against devastating securities class action exposure.

Detecting and Responding to Fraudulent Financial Reporting

Early detection of accounting machinations demands systematic vigilance and sophisticated analytical capabilities supported by robust technology solutions. Organizations must develop and maintain advanced detection mechanisms to identify warning signs before fraudulent practices escalate into costly securities class action lawsuits and regulatory enforcement actions that can destroy shareholder value.

Red Flags in Financial Statements

- Warning signs of fraudulent financial reporting create distinct patterns that investors and auditors can identify through careful analysis of financial statements and supporting documentation:

- Implausible revenue growth, particularly during challenging economic conditions, frequently signals manipulation designed to meet aggressive analyst expectations through improper aggressive revenue recognition. Inconsistency between cash flows and revenue growth reveals fundamental disconnects that suggest artificial inflation of earnings through premature or fictitious revenue recognition schemes.

- Unusually consistent sales growth or profit margins significantly exceeding industry averages should trigger heightened scrutiny of financial reporting practices and internal controls. Companies maintaining suspiciously stable performance metrics often employ sophisticated accounting irregularities and aggressive revenue recognition tactics to smooth earnings fluctuations and mask underlying business volatility.

- Frequent restatements of financial statements or disclosures indicate systematic problems with financial reporting accuracy and potential weaknesses in internal controls accounting. Rising debt-to-equity ratios exceeding 100% combined with significant fourth-quarter earnings spikes without clear seasonal justification represent additional red flags warranting investigation.

Using Forensic Accounting Tools

- Forensic accounting combines deep accounting expertise with sophisticated investigative techniques to uncover complex fraud schemes before they trigger devastating securities litigation. Modern analytical tools provide investigators with unprecedented capabilities to detect accounting fraud through:

- Advanced systems that automatically import and analyze thousands of bank statements and transaction records within seconds versus weeks of manual review. Specialized forensic data analytics software identifies suspicious patterns, statistical outliers, and concerning trends that traditional audit procedures might overlook.

- AI-powered analytical tools leverage machine learning algorithms to detect hidden data patterns and anomalies that even experienced forensic examiners might miss. These technological advances dramatically enhance organizations’ ability to identify accounting machinations during their early stages before they escalate into material misstatements.

Legal Implications: Securities Class Actions and Litigation

Securities class action filings reached an unprecedented 428 cases in 2023, highlighting the devastating legal exposure created by financial reporting fraud. Organizations facing allegations of aggressive revenue recognition or other forms of accounting fraud confront catastrophic legal and financial consequences extending far beyond immediate monetary penalties, including:

- Massive defense costs and settlement payments

- Severe reputational damage

- Loss of investor confidence

- Credit rating downgrades

- Increased borrowing costs

- Management turnover

- Regulatory investigations

- Criminal prosecution risk

- Bankruptcy exposure

- The implementation of robust internal controls and compliance programs represents the most effective defense against these devastating outcomes. Organizations must maintain comprehensive fraud prevention frameworks that combine rigorous oversight, sophisticated detection tools, and swift response protocols to protect shareholder value.

- The legal ramifications of financial reporting fraud extend far beyond monetary penalties. Companies engaging in deceptive practices face severe civil and criminal consequences, with executives directly involved in aggressive revenue recognition schemes risking personal criminal prosecution. The threat of devastating securities class action lawsuits creates powerful incentives for maintaining accurate financial statements supported by robust internal controls accounting frameworks.

- When evaluating potential litigation, plaintiff attorneys carefully assess whether courts will hold auditors accountable for failing to detect fraudulent practices, particularly in cases involving inadequate internal controls. These complex legal proceedings frequently result in settlements ranging from tens to hundreds of millions of dollars, inflicting long-lasting financial damage and reputational harm on organizations that engage in accounting manipulation.

Safeguarding Against Securities Litigation: The Path Forward

- Accounting fraud represent an insidious threat that undermines market confidence and triggers catastrophic securities class action lawsuits across industries regardless of company size. Organizations failing to implement comprehensive safeguards face devastating consequences including massive regulatory penalties, crippling legal settlements, and permanent reputational damage that can persist long after case resolution.

- Evidence demonstrates that effective fraud prevention requires a multi-layered systematic approach combining several critical protective elements:

- Robust internal controls create the foundational defense against manipulation by establishing clear policies, procedures and oversight mechanisms

- Careful segregation of duties ensures no individual can compromise entire financial processes

- Regular internal audits proactively identify control weaknesses before they enable fraud

- Automated accounting systems reduce human error while creating consistent documentation trails

- Advanced monitoring tools detect suspicious patterns and anomalies in real-time

- Transparent financial reporting builds essential stakeholder trust and accountability, while effective whistleblower mechanisms enable employees to report concerns without fear of retaliation. Strong corporate governance frameworks provide crucial oversight, particularly when combined with rigorous compliance programs addressing key regulatory requirements like aggressive revenue recognition policies.

- The warning signs of potential fraud remain remarkably consistent across different industries and time periods. Key red flags demanding immediate investigation include:

- Implausible growth during economic downturns

- Cash flows inconsistent with reported earnings

- Frequent financial restatements

- Unusual changes in internal controls

- Complex transactions near period end

- Unexplained changes in accounting policies

- High turnover in senior financial positions

- Companies that engage in financial manipulation may achieve short-term benefits but face devastating long-term consequences. Legal ramifications include both substantial civil penalties and criminal prosecution risk for executives, while regulatory enforcement actions can fundamentally reshape organizational operations. Stock price collapses following corrective disclosures create the foundation for costly securities litigation spanning multiple years.

- The investment in comprehensive fraud prevention represents sound business strategy rather than mere regulatory compliance. The cost of implementing robust internal controls accounting frameworks pales in comparison to the catastrophic impact of financial reporting fraud, which can threaten organizational survival and destroy decades of accumulated shareholder value. Key elements of an effective prevention program include:

- Regular testing and updating of control systems

- Ongoing staff training on fraud awareness

- Clear policies prohibiting aggressive revenue recognition

- Independent oversight of financial reporting

- Robust documentation requirements

- Regular risk assessments

- Swift investigation of red flags

- Strong ethical culture enforcement

Organizations prioritizing accurate financial reporting contribute to market integrity while protecting their own interests. This commitment extends beyond individual company protection to strengthen the foundation of transparent capital markets enabling economic growth and investor confidence. Companies maintaining ethical reporting practices position themselves for sustainable success while fulfilling obligations to investors, employees and the broader business community.

Key Takeaways

Financial statement fraud inflicts median losses of $593,000 per incident, making prevention crucial for business survival and stakeholder protection. Organizations must implement comprehensive safeguards combining:

- Strong internal controls frameworks

- Regular testing and monitoring

- Clear policies against aggressive revenue recognition

- Independent oversight mechanisms

- Swift investigation protocols

- Ongoing staff training

- Ethical culture reinforcement

Final Thoughts

The devastating consequences of financial reporting fraud underscore why prevention through robust controls and oversight represents sound business strategy rather than mere compliance obligation. Companies that maintain transparent reporting practices supported by comprehensive fraud prevention programs protect shareholder value while contributing to market integrity and investor confidence.

• Deploy sophisticated automated accounting systems integrated with regular internal audit programs. Modern technology solutions can flag suspicious patterns and anomalies in real-time while reducing manual processing vulnerabilities. When combined with systematic internal audits, these tools enable early detection of potential aggressive revenue recognition schemes or other manipulative practices before they escalate into material misstatements.

• Foster a culture of transparency through detailed financial disclosures and protected whistleblower channels. Clear policies should outline expected processes for reporting concerns about questionable accounting practices without fear of retaliation. This transparency builds crucial stakeholder trust while empowering employees to raise red flags about potentially fraudulent activities through secure reporting mechanisms.

• Monitor diligently for warning signs that may indicate manipulated financial reporting. Key red flags demanding immediate investigation include inexplicable revenue growth during industry downturns, cash flows that fail to align with reported earnings trends, and frequent restatements of previously issued financial statements. Companies must also watch for unusual changes in internal controls accounting practices and complex transactions executed near period-end.

• Maintain strong corporate governance through independent audit committees and strict compliance with Sarbanes-Oxley requirements. The audit committee should include financially sophisticated directors who can effectively oversee accounting policies, internal controls, and risk management activities. Regular evaluation of control effectiveness helps ensure continued adherence to regulatory standards while preserving investor confidence.

• Leverage advanced forensic accounting tools and artificial intelligence capabilities to enhance fraud detection efforts. These sophisticated technologies can identify hidden patterns and questionable transactions that might escape traditional review processes. AI-powered analytics provide an additional layer of scrutiny to catch potential manipulation before it triggers devastating consequences.

- The relatively modest investment required to implement these protective measures pales in comparison to the catastrophic financial, legal, and reputational damage that can result from accounting fraud. Beyond monetary losses, companies face severe regulatory penalties, costly securities litigation, and permanent erosion of stakeholder trust when fraudulent practices are discovered. Organizations that prioritize ethical financial reporting through robust controls and oversight not only protect their own interests but also strengthen the integrity of broader capital markets.

FAQs

Q1. What are the most prevalent forms of accounting manipulation seen today? The most common deceptive practices include premature or fictitious revenue recognition, improper expense capitalization, and manipulation of balance sheet items to enhance apparent financial health. Companies may engage in aggressive revenue recognition schemes, understate liabilities, or employ complex transactions to obscure their true financial position from investors and regulators.

Q2. How can organizations establish effective internal controls to prevent fraudulent reporting? Companies should implement comprehensive internal controls accounting frameworks that include segregated financial duties, regular audits, automated systems, transparent disclosures, and protected whistleblower mechanisms. These layered safeguards create multiple checkpoints while reducing opportunities for manipulation.

Q3. What role does corporate governance play in fraud prevention? Strong corporate governance provides essential oversight through independent board members and audit committees. These bodies monitor financial reporting processes, evaluate internal controls, assess risk management practices, and ensure compliance with regulatory requirements like Sarbanes-Oxley. Their independence helps maintain objective supervision of management’s financial reporting practices.

Q4. What warning signs might indicate potential financial statement fraud? Key red flags include implausible revenue growth during market downturns, misalignment between cash flows and reported earnings, frequent financial restatements, rising debt ratios exceeding industry norms, and significant fourth-quarter adjustments without clear business justification. Companies should also monitor for unusual changes in accounting policies or aggressive revenue recognition policies.

Q5. How do forensic accounting tools enhance fraud detection capabilities? Modern forensic tools combine traditional accounting expertise with advanced analytics and AI capabilities to uncover potential manipulation. These technologies can automatically analyze transaction patterns, identify statistical anomalies, and detect hidden relationships that might indicate fraudulent activity, enabling more effective and efficient fraud detection.

Contact Timothy L. Miles Today for a Free Case Evaluation.

If you have experienced significant financial losses and are interested in serving as lead plaintiff in a securities class action lawsuit, or if you have questions regarding securities class action settlements or your rights as a shareholder, please reach out to Tmothy L. Miles, an experienced securities litigation attorney at the Law Offices of Timothy L. Miles. We offer free consultations and are available 24/7/365 to discuss your case. You can contact us by calling 855/846-6529 or via email at [email protected]

As a shareholder advocate focused on cases involving aggressive revenue recognition and inadequate internal controls, we understand the devastating impact that misleading financial statements can have on investment portfolios. Our firm has extensive experience helping shareholders recover losses stemming from aggressive revenue recognition policies and failures in internal controls accounting.

Visit Our Extensive Investor Hub: Learning for Informed Investors