Introduction to Securities Litigation Trends 2025

Securities litigation trends in 2025 demonstrates unprecedented financial stakes that directly affect investor recovery potential. Settlement values reached record heights in 2024, with securities class action settlements totaling $4.1 billion—the highest annual total on record. This upward trajectory accelerated through the first half of 2025, as average settlement values climbed to $56 million, representing a substantial 27% increase from 2024 levels.

Disclosure Dollar Loss (DDL) Index: Measures the dollar-value change in a defendant firm’s market capitalization between the trading day immediately preceding the end of the class period and the day immediately following it. The DDL Index surged to $403 billion in H1 2025, marking a 56% increase from H2 2024. This metric captures the immediate market reaction when alleged corporate misconduct becomes known to investors.

Maximum Dollar Loss (MDL) Index: Calculates the dollar-value change from the trading day with the highest market capitalization during the class period to the day immediately following the class period’s end. The MDL Index reached $1.851 trillion in H1 2025, nearly $200 billion higher than the entire 2024 figure. This broader measure assesses potential investor losses throughout the alleged period of misconduct.

Plaintiffs filed 111 securities class actions alleging violations of Sections 10(b), 11, or 12 during this period. Significantly, 44% of these filings contained allegations regarding missed earnings guidance—the highest percentage recorded in five years. This concentration of earnings-related claims highlights the continuing risks companies face when issuing forward-looking statements.

The data reveals critical developments affecting securities litigation trends in 2025, from filing patterns and jurisdictional shifts to settlement trends and recent Supreme Court decisions. Understanding these emerging patterns becomes essential for investors seeking to protect their rights and assess potential recovery opportunities in securities class actions throughout 2025 and beyond.

Securities Class Action Filing Trends in H1 2025

Federal securities class action filings maintained consistent volume during the first half of 2025, though significant shifts emerged across industries and claim types. Plaintiffs filed 111 securities class actions alleging violations of Sections 10(b), 11, or 12 during H1 2025. This figure aligns closely with the 112 filings observed in H2 2024 and exceeds the historical semiannual average of 97. NERA’s analysis presents a slightly different perspective, documenting 108 new federal securities class action suits during this period.

The quarterly distribution reveals striking contrasts: 65 cases filed in the first quarter (a five-year high) followed by only 43 in the second quarter (a five-year low). This pattern suggests concentrated litigation activity early in 2025, potentially reflecting strategic timing by plaintiffs’ counsel.

AI-Related Securities Litigation Filings: 12 Cases and Growing

Artificial intelligence litigation has become a defining trend in 2025. Cornerstone documented 12 AI-related filings in the first half of 2025, positioning this category to significantly surpass 2024’s total of 15 filings. NERA’s analysis reports slightly higher figures with 13 suits containing AI-related claims, projecting to exceed the 16 such suits filed throughout 2024.

The surge in AI-related litigation stems primarily from what industry observers describe as “AI washing”—companies allegedly “exaggerate, misrepresent, or falsify the extent or significance of their AI capabilities to investors and the public”. These misrepresentations typically trigger legal action once the truth emerges and investors experience financial losses. California has emerged as a particular hotspot for these cases, reflecting the concentration of AI companies in that jurisdiction.

Cryptocurrency Filings on Track to Double

Cryptocurrency-related securities litigation accelerated rapidly in 2025. Six filings related to cryptocurrency were recorded during H1 2025, nearly matching the seven total crypto-related cases filed throughout all of 2024. This pace suggests cryptocurrency filings will effectively double year-over-year. NERA identified eight crypto-related filings in the first half of 2025, already matching the total observed across full-year 2024.

Emerging technology securities litigation patterns:

• AI-related cases: 12 filings (highest trend category) • Cryptocurrency-related cases: 6 filings

• SPAC-related cases: 5 filings

Life Sciences and Biotech Sector Dominance

The consumer non-cyclical sector dominated securities litigation targeting in 2025, recording 42 filings in H1 2025 compared to 32 in H2 2024—a substantial 31% increase. This surge reflects heightened litigation activity within the biotechnology and pharmaceutical subsector.

NERA’s industry classification confirms this trend, noting that filings in the health technology and services sector accounted for 29% of total filings in 2025, up from 26% in 2024. Biotechnology companies consistently rank among the most frequently targeted industries for securities class action litigation.

The concentration of litigation risk within life sciences appears disproportionate to market representation. Consumer non-cyclical companies suffered 62% of total disclosure losses while constituting only 44% of core filings. Within specific subsectors, health services and pharmaceutical companies accounted for 31% of filings but generated 65% of total losses.

Case content analysis reveals that 78% of biotechnology sector securities litigation linked to clinical trial outcomes, regulatory interactions, or product development delays. This pattern underscores the unique disclosure risks faced by companies developing novel therapies and medical technologies, where regulatory setbacks or trial failures can trigger immediate investor lawsuits.

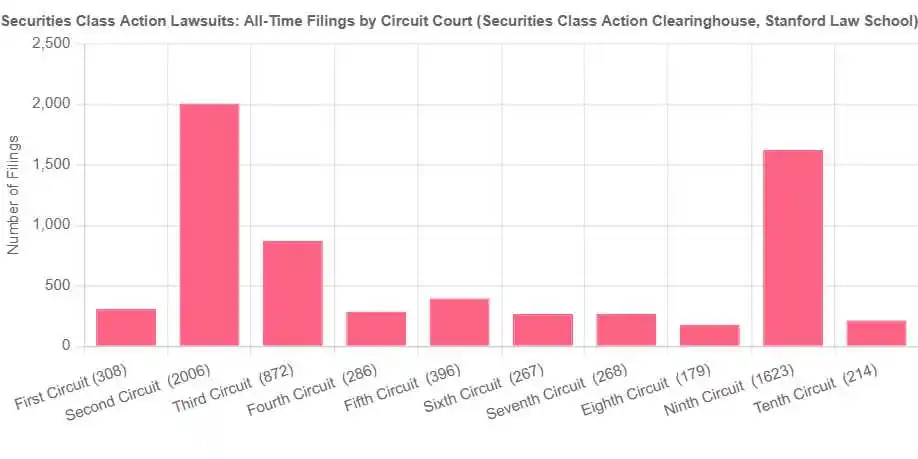

Jurisdictional Shifts in Securities Class Actions

The geographic landscape of securities class action lawsuits experienced remarkable changes during the first half of 2025, with several federal judicial circuits witnessing dramatic shifts in case distribution. These jurisdictional patterns carry significant implications for investors, as venue selection often influences both case outcomes and settlement negotiations.

Third Circuit Emerges as New Litigation Hotspot

Case filings in the Third Circuit surged from six cases in H2 2024 to 20 cases in H1 2025, representing a 233% increase that stands as one of the most significant jurisdictional shifts in recent securities litigation history. This 233% increase reflects concentrated growth in biotechnology and pharmaceutical litigation, as the Third Circuit encompasses Delaware, New Jersey, and Pennsylvania—states hosting numerous life sciences companies.

The Third Circuit’s emergence parallels similar growth in the Eleventh Circuit, where filings jumped from three cases in H2 2024 to ten cases in H1 2025. Companies headquartered in Florida, Georgia, and Alabama faced increased scrutiny from plaintiffs’ counsel throughout early 2025, suggesting favorable litigation conditions in these jurisdictions.

This jurisdictional concentration creates important strategic considerations for investors. When multiple potential venues exist for securities claims, plaintiffs’ attorneys often select circuits where procedural rules or judicial precedents favor class certification and settlement negotiations. The Third Circuit’s rapid growth indicates it may offer such advantages, particularly for life sciences litigation.

Traditional Powerhouses Maintain Dominance Despite Decline

The Second and Ninth Circuits continue their historical dominance in securities litigation, accounting for 51% of total federal securities class action filings during H1 2025, despite experiencing nearly 20% decreases in filing activity. The Second Circuit covers New York, Connecticut, and Vermont, while the Ninth Circuit encompasses California and other western states, positioning both as natural venues for financial and technology company litigation.

When measured by economic impact rather than case volume, these traditional venues remain even more significant. The Second and Ninth Circuits collectively represented 69% of the total Disclosure Dollar Loss across all securities class actions filed in H1 2025. This concentration means investors in cases filed within these circuits face higher potential damages but also greater competition for settlement funds.

Jurisdictional Distribution Analysis

| Circuit | H2 2024 Cases | H1 2025 Cases | Percentage Change | DDL Share |

|---|---|---|---|---|

| Third Circuit | 6 | 20 | +233% | Data not specified |

| Eleventh Circuit | 3 | 10 | +233% | Data not specified |

| Second & Ninth Combined | Higher baseline | 51% of total | -20% | 69% |

Core filings (excluding M&A-related cases) demonstrate particular geographic concentration, with biotechnology and pharmaceutical cases driving the Third Circuit’s growth. Technology-sector litigation remained concentrated in the Ninth Circuit, reflecting Silicon Valley’s continuing exposure to securities claims.

These jurisdictional shifts reveal strategic opportunities for both investors and their counsel. The Third Circuit’s rise as a securities litigation venue suggests plaintiffs may find more favorable conditions there, especially for life sciences cases. Conversely, the slight decline in Second and Ninth Circuit filings may indicate procedural challenges or evolving case law in those traditionally plaintiff-friendly venues.

Understanding these geographic patterns becomes essential for investors evaluating potential securities claims, as jurisdictional selection significantly affects both the likelihood of successful class certification and ultimate recovery amounts.

- Targeting of life sciences companies: A key trend in H1 2025 was a surge in securities class actions against life sciences and pharmaceutical firms. Many of these companies are headquartered in the Third Circuit, which includes Delaware, New Jersey, and Pennsylvania, creating a natural geographic concentration for lawsuits.

- Reduced activity in other circuits: While the Third Circuit saw a sharp rise in filings, the Second and Ninth Circuits—traditionally the most common jurisdictions for securities cases—saw filing numbers decrease by nearly 20% during the same period. This shift made the Third Circuit’s increase more pronounced in comparison.

- Distinct litigation focus: The increase in the Third Circuit was largely driven by a particular subject matter (biotech and pharma), while national filings for other types of securities litigation, such as cases related to COVID-19 and special purpose acquisition companies (SPACs), continued to decline.

- Influence of specific rulings: While not a cause for the overall filing increase, other Third Circuit rulings could influence litigation dynamics. For example, in August 2025, the court rejected the “reasonable indication” opt-out standard for class actions, which could influence litigation strategy in class-related securities cases.

Investor Loss Metrics: DDL and MDL Index Surges in Securities Litigation

Investor loss metrics in 2025 reveal extraordinary financial exposure patterns that directly affect potential recovery amounts in securities class action lawsuits. These figures provide essential context for understanding the true economic stakes involved in securities litigation beyond simple case counts.

DDL Index Hits $403 Billion

The DDL Index reached $403 billion in H1 2025, representing a substantial 56% increase from the $259 billion recorded in H2 2024. This dramatic rise marks the highest semiannual total since the record established in H1 2022. The current figure stands more than three times higher than the historical semiannual average of $125 billion (1997-2024).

Consumer non-cyclical sector companies accounted for a disproportionate 62% of the total DDL Index value, despite representing only 44% of core filings. Health services and pharmaceutical subsectors showed even greater concentration:

• 31% of filings originated from health services and pharmaceutical companies • 65% of total losses came from these same subsectors

This concentration pattern demonstrates the outsized financial impact of life sciences litigation relative to filing volume.

MDL Index Reaches $1.85 Trillion

The MDL Index exhibited even more dramatic growth, climbing to $1.85 trillion in H1 2025—a staggering 154% increase from the $730 billion recorded in H2 2024. This figure exceeds the full-year 2024 MDL Index by almost $200 billion. H1 2025 marks the eighth consecutive semiannual period where the MDL Index has exceeded its historical average of $622 billion.

The tremendous scale of these losses reflects a concerning concentration of massive financial exposure in relatively few cases. Mega filings—cases involving losses of at least $5 billion for DDL or $10 billion for MDL—accounted for:

• 83% of total disclosure losses • 91% of maximum losses in H1 2025

Technology Sector’s Disproportionate Impact

The technology sector represented only 18% of total core filings in H1 2025, yet these cases accounted for an extraordinary 58% of the total MDL Index value. This disparity illustrates the outsized economic impact of technology-related securities litigation relative to filing volume.

The concentration pattern reveals different risk profiles across industries. Consumer non-cyclical companies (primarily healthcare) dominated the DDL Index, while technology companies primarily influenced the MDL Index—reflecting distinct patterns of alleged misconduct and market reactions across sectors.

Neither the DDL nor MDL indices should be interpreted as direct indicators of liability or measures of potential damages. These metrics estimate the impact of all information revealed during or at the end of the class period, including information potentially unrelated to the litigation.

The record-high figures signal heightened risk exposure for public companies, particularly those in technology and healthcare sectors. Given that these metrics often inform case selection and settlement discussions, securities class actions in 2025 may involve significantly higher stakes than in previous years.

Dismissal Trends and Resolution Timelines

Case resolutions accelerated substantially during the first half of 2025, with dismissals reaching levels that significantly affect investor recovery prospects. The data demonstrates both increases in dismissal volumes and notable shifts in resolution timelines that reshape the securities litigation landscape.

77 Dismissals in H1 2025: 37.5% Annualized Increase

NERA’s analysis documented 104 total resolutions of securities class action cases during H1 2025, with 77 ending in dismissals and 27 concluding with settlements. This dismissal rate represents a substantial increase over previous periods. When annualized, these figures project to 154 dismissals for full-year 2025, which would mark a 37.5% increase compared to the 112 dismissals recorded throughout 2024.

Other industry reports suggest even higher dismissal figures. One analysis identified 87 dismissals among 121 resolved cases in the first half of 2025. Assuming this pace continues, year-end resolved cases would total 242, representing a 12% increase from the 217 cases resolved in 2024.

Dismissals are currently on track to increase for the second consecutive year, likely exceeding the 124 dismissals observed in 2024. This trend highlights the growing challenge plaintiffs face when attempting to advance securities class actions beyond preliminary stages. Since 2016, dismissals have consistently outnumbered settlements, with approximately 30% of filed cases remaining pending at any given time.

Median Time to Dismissal Drops to 1.6 Years

Resolution timelines underwent equally significant changes. The median time from the filing of the first complaint to dismissal was 1.6 years for cases dismissed in H1 2025, representing a notable decrease from the 2.0-year median recorded in 2024. This acceleration reverses a period of lengthening timelines, as the median dismissal time had previously increased from 1.4 years to 2.0 years between 2021 and 2024.

Faster dismissals may benefit defendant corporations by reducing litigation costs and uncertainty, though they create challenges for plaintiff attorneys seeking to develop cases. The shortened timeline potentially signals increased judicial efficiency or evolving procedural approaches to securities litigation.

Judicial discretion remains an important qualitative factor. Legal experts have noted that despite statistical consistency in dismissal rates across jurisdictions (approximately 44%), which judge handles a case significantly impacts dismissal outcomes. This reality underscores that even sophisticated legal strategies remain subject to judicial interpretation.

Pro-defendant and pro-plaintiff judges appear relatively evenly distributed across jurisdictions. This distribution may explain why the overall dismissal rate remains fairly consistent despite individual variations in judicial approach. For investors considering securities litigation, this implies that predicting case outcomes based solely on legal merit remains challenging due to the human element in judicial decision-making.

These dismissal trends offer important strategic insights for investors and their counsel. The increasing rate of dismissals coupled with faster resolution timelines may influence case selection criteria and alter the economics of securities class action litigation throughout 2025.

Settlement Patterns: Fewer Cases, Bigger Payouts

Securities class action settlements in 2025 demonstrate a clear shift toward higher-value resolutions, even as fewer cases reach settlement agreements. This pattern directly affects investor recovery potential and reflects strategic changes in how securities class action cases proceed through the litigation process.

Average Settlement Value Rises to $56 Million

The average settlement value climbed to $56 million in H1 2025, representing a substantial 27% increase from the 2024 inflation-adjusted average of $44 million. This growth occurred despite consistent settlement volumes, with the first half of 2025 recording 41 settlements totaling $1.10 billion. NERA’s analysis documented 27 settlements with an aggregate value of $1.80 billion, representing 45% of the inflation-adjusted total of $3.90 billion recorded in 2024.

Settlement distribution across industries has shifted notably from previous patterns. Technology sector cases no longer dominate large settlements, as major payouts now emerge from energy, mining, services, and technology companies. These settlements address M&A disputes, operational issues, price-fixing allegations, and accounting irregularities.

13% of Securities Litigation Settlements Exceed $100 Million

High-value settlements increased substantially as a proportion of total resolutions. Cases with monetary payments exceeding $100 million represented 13% of H1 2025 settlements, up from 8% in 2024. An additional 13% fell between $50-$100 million, increasing from 9% in 2024.

Notable settlements from this period include:

• $362.50 million General Electric resolution in Q1 2025, representing significant shareholder recovery

• $398.05 million antitrust settlement involving wage-fixing allegations in the poultry processing industry

• $140 million Taxi and Limousine Commission settlement addressing driver license suspension practices

• $109 million class action resolution for property owners affected by unpaid tax issues

International cases also yielded substantial recoveries. The Grupo Televisa case involving a Mexico-based defendant achieved a pro rata payout rate of nearly 22%, demonstrating how U.S. class actions provide meaningful recoveries for non-U.S. shareholders.

Median Settlement Value Declines to $12.50 Million

While average settlement values increased, the median settlement amount fell to $12.50 million in H1 2025, declining $1.80 million from the 2024 inflation-adjusted median of $14.30 million. This divergence between average and median figures reveals concentration of settlement dollars among fewer high-value cases.

The contrasting movement of these metrics indicates greater polarization in settlement outcomes. High-profile nine-figure settlements capture attention, yet most securities litigation resolves for more modest amounts. This pattern suggests plaintiffs’ counsel increasingly concentrate resources on cases with substantial recovery potential rather than pursuing numerous smaller actions.

The economics of securities class action lawsuits appear to reflect a “quality over quantity” approach in 2025, with significant implications for investor recovery strategies and case selection criteria.

Subject Matter Trends in Securities Lawsuits

Securities litigation patterns reveal specific triggers that consistently lead to investor losses and subsequent legal action. The data from H1 2025 demonstrates clear shifts in allegation types, providing important insights for investors monitoring their portfolio companies’ disclosure practices.

Missed Earnings Guidance Reaches Five-Year High

Earnings guidance failures now represent the dominant source of securities litigation risk. A remarkable 44% of filings in H1 2025 contained claims concerning missed earnings guidance. This percentage marks the highest level recorded in five years, climbing steadily from 23% in 2021 and 2022, to 31% in 2023, and 41% in 2024.

Forward-looking statements create substantial litigation exposure once companies fail to meet announced targets. Financial projections that miss their mark become litigation triggers when the market learns the truth about a company’s actual performance. As one expert observed, “projections that missed the mark can also be fodder for government enforcement actions, especially if the SEC is prioritizing ‘fraud'”.

NERA’s analysis of standard cases (those alleging violations of Rule 10b-5, Section 11, and/or Section 12) confirmed that 41% included claims related to missed earnings guidance. This concentration underscores the persistent risks companies face when issuing quantitative financial projections, regardless of whether targets are missed due to external market conditions or internal operational challenges.

Misleading Future Performance Claims Hold Steady

Broader business projections beyond specific financial metrics appeared in 33% of securities class action filings during H1 2025. This represents a slight increase from 29% in 2023 and maintains the 32% level observed in 2024.

These allegations typically target qualitative statements about business conditions, market opportunities, or competitive positioning rather than specific financial targets. Companies face litigation risk when their optimistic statements about future prospects prove inconsistent with subsequent business developments.

The data reveals a notable shift away from traditional accounting-based claims. Standard cases containing accounting-related allegations declined to just 13%, representing more than a one-third decrease. Similarly, merger-integration issues continued falling, dropping over 25% to only 8% of standard cases. This pattern suggests plaintiff attorneys currently find greater success challenging forward-looking statements than historical financial reporting.

Technology Securities Litigation Categories Emerge

Artificial intelligence and cryptocurrency cases represent the fastest-growing litigation categories in 2025. AI-related claims led with 12 filings, while cryptocurrency cases reached 6 filings in H1 2025. Cryptocurrency litigation shows particular momentum, nearly matching in six months the seven cases filed throughout all of 2024.

These emerging technology cases typically arise from “AI washing” or cryptocurrency misrepresentations, where companies allegedly exaggerate their technological capabilities or involvement in trending sectors to boost investor interest.

Traditional Categories Decline

SPAC and COVID-related securities litigation continued their downward trajectories in early 2025. SPAC-related filings fell to just four suits in H1 2025, compared to nine throughout 2024. COVID-related cases dropped to merely two filings, representing the lowest level since this category emerged in 2020.

These declines reflect both the cooling of relevant markets and the maturation of litigation cycles arising from earlier periods of heightened activity. The SPAC decline parallels reduced market activity in that sector, while fewer COVID-related cases suggest most pandemic-related corporate disclosure issues have been addressed through the legal system.

Understanding these subject matter trends helps investors identify potential risk factors in their holdings and assess the likelihood of future securities litigation affecting specific companies or sectors.

Impact of Supreme Court Rulings on Litigation Strategy

Recent Supreme Court decisions fundamentally altered securities litigation in 2025, creating new challenges for investor recovery while reshaping both private plaintiff strategies and SEC enforcement approaches. These landmark rulings require investors and their counsel to adapt their legal strategies when pursuing securities fraud claims.

Macquarie v. Moab: Pure Omissions No Longer Actionable

The Supreme Court’s unanimous ruling in Macquarie Infrastructure Corp. v. Moab Partners LP eliminated a significant pathway for securities fraud claims. The Court determined that “pure omissions” cannot support private claims under Rule 10b-5(b), even when such omissions might violate SEC regulations. This decision resolved a longstanding circuit split, holding that the “failure to disclose information required by Item 303 can support a Rule 10b-5(b) claim only if the omission renders affirmative statements made misleading”.

Pure omissions: Situations where a company says nothing about a material topic, remaining completely silent on important information that investors might need.

Half-truths: Statements that are technically accurate but omit essential qualifying information that would change their meaning or significance.

Plaintiffs must now identify specific statements rendered misleading by alleged omissions rather than claiming standalone disclosure violations. Courts throughout 2025 have increasingly dismissed cases lacking this connection, requiring “a meaningful relationship between statements made and those allegedly omitted”. This ruling significantly narrows the scope of actionable securities fraud claims, potentially reducing recovery opportunities for investors who suffered losses due to corporate silence on material issues.

Jarkesy: SEC Civil Penalties Require Jury Trial

The Court’s ruling in SEC v. Jarkesy stripped the SEC of a powerful enforcement tool, determining that “the Seventh Amendment entitles a defendant to a jury trial when the SEC seeks civil penalties against him for securities fraud“. This decision prevents the agency from using its own administrative courts to pursue civil penalties.

The 6-3 opinion explained that civil penalties constitute “a legal remedy implicating the Seventh Amendment jury right whenever they are meant to punish or deter a defendant“. Consequently, the SEC must now bring cases seeking civil penalties in federal court, potentially becoming “more selective regarding what claims to pursue”. This selectivity may result in fewer enforcement actions, potentially reducing the deterrent effect of SEC oversight on corporate misconduct.

Implications for Rule 10b-5 and Section 11 Claims

These decisions prompted substantial adjustments in securities class action strategy. Following Macquarie, plaintiffs pursue two primary approaches: identifying “textual hooks” rendered misleading by omissions or pursuing claims under scheme liability theory. Litigation increasingly focuses on whether generic statements about corporate policies were rendered misleading by specific negative developments.

The Court’s earlier decision in Goldman Sachs continues influencing class certification challenges, with defendants successfully defeating certification by demonstrating “a mismatch between the challenged statement and a purported corrective disclosure“. Post-Macquarie rulings show courts increasingly willing to dismiss cases when alleged omissions are “untethered to any affirmative statement”.

These Supreme Court decisions have made securities fraud claims more challenging to plead and prove, requiring stronger connections between alleged omissions and specific misleading statements while simultaneously reshaping SEC enforcement approaches. Investors pursuing securities litigation must now work with counsel who understand these evolving legal standards and can craft complaints that survive increasingly rigorous judicial scrutiny.

Class Certification Requirements and Price Impact Analysis

Class certification serves as the crucial gateway that determines whether securities litigation can proceed as a class action, directly affecting investors’ ability to pursue collective recovery. Federal courts apply refined frameworks that examine price impact evidence and damages models to evaluate whether individual investor claims can be resolved through common proof.

The Goldman Sachs Mismatch Framework

The Supreme Court’s “mismatch” analysis from Goldman Sachs gained significant application throughout 2025. This framework examines whether generic corporate statements align with specific corrective disclosures when courts evaluate price impact at class certification. Courts increasingly deny certification where generic statements fail to match specific corrections. The 2024 period showed a marked increase in class certification denials based on this analytical framework .

The Second Circuit demonstrated this principle’s power by decertifying a class in Arkansas Teacher Retirement System v. Goldman Sachs. The court determined that defendants “managed to sever the link between back-end price drop and front-end misrepresentation” . The Second Circuit directed district courts to conduct a “searching price impact analysis” whenever there exists a “considerable gap” between the genericness of statements and their corrections .

- A gap in “genericness” between a misrepresentation and a corrective disclosure reduces the likelihood that investors would understand the disclosure to have corrected the misrepresentation.

- When this “genericness gap” exists, the inference that the stock price drop was caused by the corrective disclosure “starts to break down”.

- The court found that there was an “insufficient link” between Goldman Sachs’s generic statements and the later, specific disclosures to show that the generic statements had impacted the stock price.

Goldman v. Macquarie Securities Litigation Comparison

| Case | Issue | Holding | Importance/Context |

|---|---|---|---|

| Macquarie Infrastructure Corp. v. Moab Partners LP | Can a pure omission (failure to disclose information without an otherwise misleading statement) create liability under Rule 10b-5(b) of the Securities Exchange Act in securities class actions? | No. The Supreme Court held that Rule 10b-5(b) targets only misrepresentations and half-truths, not pure omissions. A pure omission, even if violating a disclosure duty like Item 303, doesn’t, on its own, support a private right of action under Rule 10b-5(b). | This unanimous Supreme Court decision resolved a circuit split and confirmed that Rule 10b-5(b) focuses on actively misleading statements, not simply failing to disclose required information. However, it doesn’t limit SEC enforcement actions or the potential for liability under other securities law provisions like Section 11 of the Securities Act, or under other parts of Rule 10b-5 (e.g., scheme liability). |

| Goldman Sachs Group, Inc. v. Arkansas Teacher Retirement System | At the class certification stage in securities class actions, how should courts consider the generic nature of alleged misrepresentations when evaluating price impact and the presumption of reliance? | The generic nature of alleged misrepresentations is important evidence that courts should consider when evaluating price impact to determine if the Basic presumption of reliance is rebutted in securities class actions. | This case clarifies that the generic nature of statements is a relevant factor at the class certification stage in evaluating price impact, even if it might overlap with merits issues like materiality. The Second Circuit decertified the class in 2023, finding that Goldman Sachs successfully rebutted the presumption of reliance by demonstrating an insufficient link between their generic statements and the later, more specific corrective disclosures. |

- Distinguishing pure omissions from half-truths: The Macquarie decision draws a clear line: Rule 10b-5(b) addresses misleading statements and “half-truths” (statements that are true but incomplete and thus misleading), but not “pure omissions” (simply failing to disclose information, even if required by regulation, absent an otherwise misleading statement).

- Significance of “genericness” in price impact: Goldman Sachs highlights that the generic nature of alleged misrepresentations can be a powerful tool for defendants to challenge class certification in securities class actions.

- Continued Importance of Item 303 and SEC Enforcement: Even though a private right of action for pure omissions under Rule 10b-5(b) may be limited by Macquarie, public companies still have a duty to disclose information required by Item 303 and can face SEC enforcement actions for failing to do so.

- Nuance in Securities Fraud Claims: These cases emphasize the nuanced nature of proving securities fraud, particularly in securities class actions involving omissions. Plaintiffs must carefully consider the specific nature of the alleged omissions and their relation to any affirmative statements made by the defendant in securities class actions.

Damages Model Standards: Lytle v. Nutramax Decision

The Ninth Circuit resolved a critical question in August 2025 regarding damages model requirements before class certification. In Lytle v. Nutramax, the court held that unexecuted damages models—even if unpersuasive—can demonstrate that damages are susceptible to common proof . The panel ruled that an expert’s conjoint analysis methodology need not be applied to actual data before certification, provided it “will be able to reliably calculate damages in a manner common to the class at trial” .

Event Studies as Certification Defense Tools

Event studies have become essential components in securities litigation. These statistical analyses determine whether alleged misrepresentations affected stock prices—critical evidence for defeating class certification under Halliburton II . The studies analyze price movements at two essential points: when misrepresentations occur (“front-end”) and when corrective disclosures happen (“back-end”) .

Courts recognize event studies’ limitations with “bundled” disclosures that combine multiple news items . Despite these analytical challenges, defendants who succeed at class certification typically prevail because “their expert’s event studies are more probative of price impact than the fund’s expert event studies” .

Practical implications for investors: These certification standards directly affect whether individual investor claims can proceed collectively. When courts deny class certification, investors must pursue individual lawsuits or accept that their claims may not be economically viable to pursue alone.

Conclusion

Securities litigation in 2025 reveals patterns that fundamentally reshape investor risk assessment and recovery expectations. The data demonstrates a clear shift toward higher-stakes litigation, with DDL Index reaching $403 billion and settlement values averaging $56 million—figures that demand serious attention from anyone involved in securities markets.

The concentration of financial exposure tells a compelling story. While tech companies now account for 58% of the total MDL Index value despite representing only 18% of filings, healthcare and life sciences companies face their own disproportionate litigation risks. This sector-specific targeting requires enhanced disclosure practices, particularly regarding clinical trials, regulatory interactions, and forward-looking statements about product development.

Emerging litigation categories reflect broader market dynamics. AI-related filings reached 12 cases in the first half of 2025, positioning this category to exceed 2024’s total significantly. Cryptocurrency litigation shows similar momentum, with cases on track to double year-over-year. These trends follow capital flows, suggesting securities litigation will continue adapting to technological innovation and investment patterns.

Recent Supreme Court decisions create new strategic imperatives. The Macquarie ruling eliminates “pure omissions” claims, forcing plaintiffs to connect alleged omissions to specific misleading statements. Meanwhile, Jarkesy requires jury trials for SEC civil penalties, fundamentally altering regulatory enforcement approaches. These precedents will influence securities law for years ahead.

The jurisdictional shifts observed throughout 2025 provide tactical insights for both investors and defendants. The Third Circuit’s dramatic surge in life sciences litigation, coupled with continued dominance of the Second and Ninth Circuits, reveals geographic patterns that affect case strategy and potential outcomes.

Perhaps most significantly, the trend toward fewer but larger settlements suggests a maturing litigation market. Plaintiffs’ counsel increasingly focus resources on high-value cases rather than pursuing numerous smaller actions. This concentration pattern benefits investors in strong cases while potentially limiting options for those with smaller losses.

For investors monitoring these trends, the implications are clear: companies face heightened scrutiny of forward-looking statements, particularly earnings guidance, which appeared in 44% of H1 2025 filings. The accelerated dismissal timelines—dropping to 1.6 years median—require prompt action when securities violations occur.

Securities litigation continues evolving toward higher stakes, greater selectivity, and enhanced complexity. Investors who understand these patterns can better assess their rights and potential recoveries while navigating an increasingly sophisticated legal landscape. Companies must adapt their risk management and disclosure practices accordingly, recognizing that the financial and reputational stakes have never been higher.

Key Takeaways

Securities litigation in 2025 reveals unprecedented financial stakes and evolving risk patterns that demand immediate attention from corporate leaders and legal practitioners.

• Record-breaking investor losses: DDL Index surged 56% to $403 billion while MDL Index reached $1.85 trillion, creating the highest financial stakes in securities litigation history.

• AI and crypto litigation exploding: AI-related filings hit 12 cases (on track to exceed 2024’s total), while cryptocurrency cases are set to double year-over-year.

• Healthcare and tech sectors face disproportionate risk: Life sciences companies saw 31% increase in filings, while tech represents 58% of total maximum dollar losses despite only 18% of cases.

• Supreme Court rulings reshape strategy: Macquarie decision eliminates “pure omissions” claims, while Jarkesy requires jury trials for SEC civil penalties, fundamentally altering litigation approaches.

• Settlement values soar despite fewer cases: Average settlements jumped 27% to $56 million, with 13% exceeding $100 million, indicating a shift toward higher-stakes, selective litigation.

The concentration of massive financial exposure in fewer cases signals a fundamental shift toward “quality over quantity” in securities litigation, requiring enhanced risk management and more sophisticated legal strategies.

FAQs

Q1. What are the key trends in securities class action filings for 2025? Securities class action filings in 2025 show significant increases in AI-related and cryptocurrency cases, with life sciences and biotech sectors facing the highest number of lawsuits. There’s also a notable shift in jurisdictional patterns, with the Third Circuit experiencing a dramatic surge in case filings.

Q2. How have investor loss metrics changed in recent securities litigation? Investor loss metrics have reached unprecedented levels in 2025. The Disclosure Dollar Loss (DDL) Index hit $403 billion, while the Maximum Dollar Loss (MDL) Index soared to $1.85 trillion. These figures represent substantial increases from previous periods and indicate heightened financial stakes in securities litigation.

Q3. What impact have recent Supreme Court rulings had on securities litigation strategies? Recent Supreme Court decisions have significantly altered securities litigation strategies. The Macquarie v. Moab ruling has made it harder to pursue claims based on pure omissions, while the Jarkesy decision now requires jury trials for SEC civil penalties. These rulings have forced both plaintiffs and regulators to adjust their approaches to securities cases.

Q4. How have settlement patterns in securities class actions evolved in 2025? Settlement patterns in 2025 show fewer cases but larger payouts. The average settlement value rose to $56 million, a 27% increase from 2024. Additionally, 13% of settlements now exceed $100 million, up from 8% in the previous year. This trend suggests a shift towards more selective, high-stakes litigation.

Q5. What are the primary subject matter trends in recent securities lawsuits? The most common allegations in recent securities lawsuits involve missed earnings guidance, appearing in 44% of cases. Claims about misleading future performance are also prevalent, featured in 33% of filings. Notably, there’s been a decline in SPAC and COVID-related filings, while AI and cryptocurrency-related cases are on the rise.

Visit Our Extensive Investor Hub: Learning for Informed Investors