SECURITIES CLASS ACTION LAWSUITS: A COMPREHENSIVE GUIDE ON THE ROLE OF REGULATORY BODIES [2025]

LAW OFFICES OF TIMOTHY L. MILES

TIMOTHY L. MILES

(855) TIM-M-LAW (855-846-659)

[email protected]

(24/7/365)

Introduction to the Role of Regulatory Bodies in Securities Class Action Lawsuits

Securities Class Action Lawsuits pose a major financial risk to companies. The median settlement value reached $13 million in 2022, and this is a big deal as it means that some cases hit the $1 billion mark. Legal professionals and corporate leaders need to grasp these complex legal proceedings to protect their organizations and stakeholders better.

Securities class action is a federal class action lawsuit where investors join forces to seek damages when they believe securities laws have been violated. On top of that, these cases represent much of today’s class action landscape. As of a 2017 survey, labor and employment class actions made up 37.7% of all class action matters, while consumer fraud accounted for 19%. This piece analyzes the securities class action definition and shows how regulatory bodies shape these proceedings.

The regulatory scene keeps changing. This becomes even more crucial when you have both U.S. and some European countries demanding companies to disclose their human rights effects annually. Yet many companies provide minimal or potentially misleading disclosures, which adds new layers of complexity to regulatory oversight.

This piece breaks down the legal frameworks behind securities class actions. You will learn what triggers these filings and get strategic guidance to handle these complex legal challenges.

Please see these additional various investor resources below for an additional wealth of information on shareholder litigation.

What is a Securities Class Action?

Securities class action lawsuits serve as a powerful legal tool that helps groups of investors address their grievances together. These legal proceedings play a vital role in U.S. securities regulation. They give shareholders a chance to seek justice when they lack resources to file individual claims.

TIMOTHY L. MILES | FREE CASE EVALUATION

Securities class action definition under Rule 23

Key differences from other federal class action lawsuits

Securities class actions stand out from other federal class action lawsuits in several ways. These cases focus on violations of federal securities laws.

Most securities class actions claim that company leaders made misleading statements or held back information. These actions artificially raised stock prices, causing investors to lose money when the truth came out. The “fraud-on-the-market” theory backs many of these cases, making them different from other class actions.

The law treats securities class actions differently too. The Private Securities Litigation Reform Act of 1995 states that the best lead plaintiff has the largest financial interest in the outcome. This creates a unique way to pick class representatives.

Securities class actions automatically include investors who purchased during the class period and suffered a loss, unless they choose to leave. This “opt out” approach differs from other class actions that need members to join actively.

Lead plaintiff applications must follow strict timing rules. Applicants have 60 days after the first complaint to file, and courts strictly enforce this deadline.

These cases usually take two to three years to finish, whether through settlement, judgment, or dismissal. This timeline reflects the complex nature of proving securities fraud and gathering evidence.

Legal Framework Governing Securities Class Actions

Securities class action regulations have evolved through decades of legislative and judicial action. Three main pillars shape the legal framework that controls these complex proceedings. Each pillar plays a unique but connected role in defining how investors can seek compensation for alleged securities violations.

Securities Exchange Act of 1934 and Rule 10b-5

Private Securities Litigation Reform Act (PSLRA)

Congress passed the Private Securities Litigation Reform Act in 1995 to address concerns about frivolous securities lawsuits. The PSLRA covers private actions under both the Securities Act of 1933 and the Exchange Act of 1934 and brought several key changes to stop perceived abuses.

The PSLRA created stricter pleading standards. Plaintiffs now must point out each misleading statement, explain why it is misleading, and show clear facts that strongly suggest scienter. The Supreme Court’s ruling in Tellabs, Inc. v. Makor Issues & Rights, Ltd. states that a complaint only survives when a reasonable person would find the scienter inference “cogent and at least as compelling as any opposing inference.”

The law’s lead plaintiff provision now pushes institutional investors to take charge of cases. This stopped the old “race to the courthouse” by making courts pick the investor with the biggest financial stake as lead plaintiff. The PSLRA also stops discovery while a motion to dismiss is pending, which protects defendants from expensive discovery costs in potentially baseless cases.

Plaintiffs started filing in state courts to dodge these requirements. Congress answered by passing the Securities Litigation Uniform Standards Act of 1998 (SLUSA), which moves most securities fraud class actions to federal court where the PSLRA applies.

Role of the Sarbanes-Oxley Act in Class Actions

The Sarbanes-Oxley Act of 2002 (SOX) came after major corporate scandals at Enron and WorldCom. While not focused on class actions, SOX changes how securities litigation works through several important rules.

SOX’s Section 302 makes corporate officers personally responsible by requiring them to certify financial reports’ accuracy. This requirement creates strong evidence for securities class actions about financial misreporting.

Section 806 shields whistleblowers who report corporate wrongdoing. These protections help insiders speak up about potential securities violations, often providing facts that lead to class actions.

Research shows that SOX’s better internal controls have reduced financial restatements since 2005. Securities class action filings dropped, while audit quality improved overall.

Regulatory Triggers That Lead to Class Action Filings

Securities class actions start when potential violations of securities laws come to light. Companies and investors need to know these warning signs that might lead to legal proceedings.

Material misstatements and omissions

Stock price drops and investor losses

Stock price drops are the clearest trigger for securities class actions. These cases “routinely get filed against public companies when their stock price drops”. The pattern usually goes like this:

- Company makes allegedly misleading statements that push the stock price up

- Truth comes out through corrective disclosures

- Stock price drops

- Investors sue to get their money back

Damage calculations assume the stock price drop comes from the alleged fraud. This method does not always factor in complex market forces, including how stock prices drop not just from corrections but from changes in how investors see risk.

Big market cap losses raise the risk of lawsuits. A NERA report showed that total settlement amounts for cases in 2022 reached $4 billion—$2 billion more than the inflation-adjusted amount in 2021. The average settlement grew by more than 70% to $38 million that year.

SEC investigations and enforcement actions

Government investigations, especially from the Securities and Exchange Commission, often come before or alongside securities class actions. The SEC can stop trading when disclosure questions come up or block sales under misleading registration statements.

SEC involvement makes things easier for plaintiffs because they can “piggyback on the work done by the government”. About 20% of class action settlements come from cases targeting the same issues as SEC enforcement actions. Research shows these “piggybacking” actions have a better chance of surviving dismissal motions and getting bigger settlements.

Companies facing both SEC investigations and class actions lose more market confidence than those dealing with just one type of proceeding. Class actions alone show stronger links to decreased institutional ownership and increased stock turnover than SEC investigations by themselves.

The SEC can also order violators to give up their ill-gotten gains, with money potentially going to harmed investors. This creates two paths for recovery and makes the securities market more accountable.

Red Flags That Attract Regulatory Scrutiny

Warning signs usually appear before regulatory action hits the securities sector. Companies that see these red flags should get ready for close examination that often guides them toward class action lawsuits. Knowledge of these warning signs helps spot possible legal risks before official proceedings start.

Multiple CIDs and parallel investigations

Regulators use Civil Investigative Demands (CIDs) as a powerful tool to make companies produce documents or give sworn testimony before litigation begins. Companies receiving multiple CIDs from different agencies should take notice. This usually shows regulators working together and sharing information between civil and criminal investigations.

CIDs work differently from grand jury subpoenas that limit information sharing. Criminal prosecutors can cooperate better with their civil attorney colleagues through CIDs. Multiple CIDs signal possible parallel enforcement actions from both federal and state regulators.

These parallel proceedings can create more problems by starting a cycle of growing regulatory scrutiny. Criminal prosecutors might pick CIDs over grand jury subpoenas to help share information with civil counterparts. Companies should think about pursuing settlements with multiple government regulators during this time, even though these negotiations take considerable effort.

Consumer harm and public interest concerns

Regulatory bodies become aggressive when business activities allegedly harm consumers. The Federal Trade Commission (FTC) targets companies that try to “fix prices, lessen competition, and otherwise illegally manipulate the marketplace” through unfair practices. Consumer harm can lead to major civil liability, restitution, and penalties.

Business activities that become part of political discussions need extra attention. Cases affecting regional or national interests might go public and spark more regulatory inquiries and class action interest.

The FTC’s role in consumer protection shows this pattern clearly. Regulators actively target scams that hurt vulnerable populations. One regulator put it simply: “scammers are like cockroaches. You might kill one, but there are plenty more out there”. This means companies working in consumer-focused sectors face closer examination.

Whistleblower disclosures and internal leaks

Whistleblowers create significant risk because they can access records and documents. The SEC shows steadfast dedication to protecting whistleblowers by taking action against companies that create barriers to whistleblower programs.

Small provisions in employment agreements can catch the SEC’s attention. The SEC charged seven companies that made employees waive monetary awards for helping with government investigations. These companies paid civil penalties between $19,500 and $1,380,600, based on how many violative agreements they had.

The SEC ordered International Game Technology to pay a $500,000 penalty after they fired a whistleblower who reported possible financial statement problems. This action highlights the SEC’s focus on whistleblower protection. Andrew Ceresney, former SEC Enforcement Director, stated: “Strong enforcement of anti-retaliation protections is critical to the success of the SEC’s whistleblower program”.

Companies should check all employee documents to make sure they don’t have language that might stop reporting to the SEC. The SEC can charge companies just for having problematic language, even if they don’t enforce it.

Coordination Between Federal and State Regulators

Federal and state regulators work together in a complex ecosystem where jurisdictions overlap and frameworks align to address securities violations. Their coordination has grown stronger over the last several years. This has created a unified approach to enforcement that affects how securities class action lawsuits develop.

Role of the SEC and DOJ in securities litigation

The SEC and Department of Justice (DOJ) have strengthened their joint approach to curb securities violations. Many practitioners now see them as a “unified front.” These agencies share resources, expertise, and data to boost their enforcement capabilities against unlawful trading practices. Their partnership helps them identify and prosecute securities violations more effectively through complementary approaches.

The agencies often demonstrate their coordination through parallel proceedings—SEC handles civil enforcement while DOJ pursues criminal prosecution. Recent cases show both agencies announcing charges together, which proves their aligned strategy. A good example shows up in the BP-TravelCenters merger case. The SEC’s Market Abuse Unit spotted suspicious trading and referred it to DOJ for criminal charges within three months.

This interagency teamwork creates real challenges for defendants. They must handle both civil and criminal proceedings at once, each with its own standards of proof and procedural rules.

State Attorneys General and multistate actions

State Attorneys General (AGs) have become powerful enforcers in securities law. They often step in where federal enforcement might fall short. The New York Attorney General leads state-level enforcement with broad statutory powers to conduct civil and criminal securities investigations. California and Maryland AGs have also taken action against cryptocurrency issuers and exchanges for alleged state securities law violations.

Multistate litigation has proven highly effective since 1907. Two or more state AGs work together against common defendants in these coordinated actions. They tap into collective resources and expertise across jurisdictions. The North American Securities Administrators Association (NASAA) makes shared enforcement easier among its members.

State AGs help each other by exchanging information and dividing resources in complex multi-state cases. Companies find it challenging to deal with investigations happening in several jurisdictions simultaneously.

Information sharing and joint enforcement

Federal and state regulators have expanded their formal information sharing channels. The SEC and NASAA signed a Memorandum of Understanding (MOU) in 2017 to share information about intrastate crowdfunding and regional securities offerings. NASAA then signed another MOU with the Commodity Futures Trading Commission (CFTC) in 2018, setting up confidential information exchange rules.

These agreements help participants enforce the Commodity Exchange Act. State securities regulators and AGs can enforce this act alongside federal agencies. CFTC Chairman Christopher Giancarlo called the 2018 MOU “a milestone in the area of U.S. federal and state financial fraud detection and prosecution”.

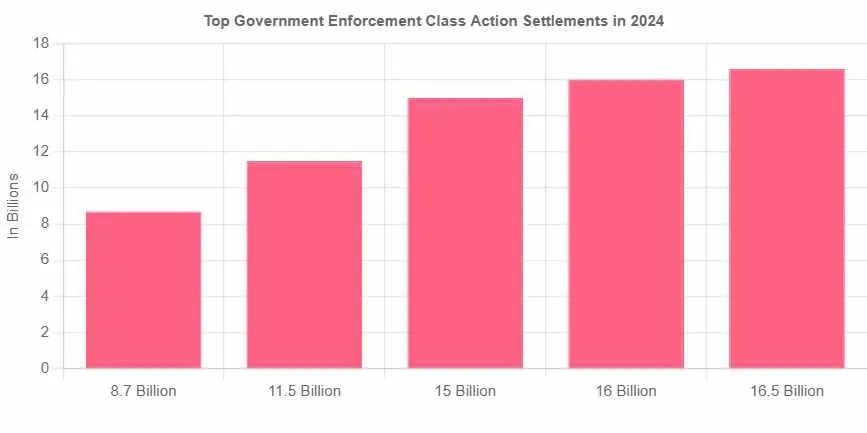

Information sharing remains crucial to cooperative enforcement in today’s regulatory world. A 2023 case highlights this perfectly. A group of 30 state securities regulators worked with both the SEC and CFTC to reach a $68 million settlement in a precious metals fraud case. These multi-jurisdictional actions work efficiently for regulators but increase costs and complexity for defendants.

Parallel Litigation and Its Impact on Class Actions

Companies dealing with securities class actions must handle multiple parallel lawsuits based on the same allegations. This creates a complex legal landscape with major financial consequences.

Overlap with antitrust and derivative lawsuits

Securities class actions often come with parallel litigation, especially derivative lawsuits. Research shows that 47% of securities class action settlements between 2019 and 2023 had an accompanying derivative action. Shareholders can use these derivative suits to sue on behalf of the corporation when directors or officers cause harm, usually based on facts similar to the securities class action.

Multiple parallel actions create unique dynamics in these cases. A Cornerstone Research study shows better outcomes for plaintiffs when securities class actions run alongside derivative actions. Settlement amounts show a 36% premium based on median figures for cases settled between 2019 and 2023. This dual legal pressure gives investors more negotiating power and leads to better settlements.

Antitrust claims sometimes overlap with securities litigation alongside derivative suits. The Credit Default Swaps Antitrust Litigation settled for $1.86 billion in 2015, while the FX-rigging case exceeded $2.31 billion. These cases often involve over-the-counter transactions that traditional securities identifiers can’t easily track, so filing claims needs special attention.

TIMOTHY L. MILES | FREE CASE EVALUATION

Response Strategy for Companies Facing Class Actions

A swift and decisive response can substantially affect the outcome when a company faces a securities class action lawsuit. Companies need to coordinate multiple parties right away and pay close attention to procedural requirements for an effective defense strategy.

Activating legal and compliance teams

Companies should talk to their insurance brokers about entity insurance coverage as soon as they spot potential litigation risks. Securities litigation counsel can review directors and officers (D&O) liability insurance policies and work with carriers to meet coverage requirements effectively. Quick action is vital since delayed notifications might lead to coverage denials.

Legal teams must think over the best ways to protect attorney-client privilege and work product across all communications. This protection becomes especially important with today’s multiple communication platforms like messaging apps, text messages, and email. Early discussions with counsel help protect privilege proactively in third-party cases.

Preserving documents and issuing legal holds

Companies must set up a litigation hold (also called a legal hold notice or document preservation notice) to stop relevant information from being deleted or destroyed when litigation is predicted. A proper legal hold notice should:

- Detail the scope of the matter and relevant time periods

- Provide representative examples of data types to preserve

- Explain custodians’ obligations for compliance

- Offer reliable contact information for questions

Top legal hold tool providers include automated systems to issue and track notices. These systems make your process look more reasonable to litigation opponents and judges, which reduces the risk of expensive “discovery-on-discovery” disputes. Many electronic sources can be preserved automatically through backend software features or mobile device management solutions, though some data types might still need custodian involvement.

Engaging experienced securities litigation counsel

Skilled class action defense counsel can mean the difference between a good outcome and a long, expensive litigation process. Boards should review each firm’s securities litigation expertise, reputation, and resources before making their choice.

Plaintiff lawyers know which defense firms maintain trial-ready positions and aggressive pre-trial strategies. Defense counsel’s credibility with plaintiff lawyers often leads to better and earlier settlements. Lawyers who specialize in securities litigation often get cases dismissed before discovery begins at the motion-to-dismiss phase. These dismissals can reduce average settlements to less than half the national average.

Directors should get regular updates from their legal team during these critical periods to make informed decisions throughout the litigation process.

Future Trends in Regulatory Oversight of Class Actions

Securities class action regulations keep changing as new technologies and disclosure requirements alter enforcement priorities.

Increased focus on ESG-related disclosures

ESG litigation has grown significantly over the last several years. Climate change cases saw a dramatic rise from 884 in 24 countries to 1,550 across 38 countries between 2017 and 2020. The FTC now revises its Green Guides while EU climate legislation shapes U.S. regulatory approaches. California has implemented mandatory climate reporting rules that affect large companies operating in the state. Nonprofits file most ESG-related class actions in District of Columbia courts and use local consumer protection laws. These cases primarily target “greenwashing” practices.

AI and data analytics in fraud detection

Government agencies now make use of artificial intelligence to spot potential securities violations. The SEC has used AI-powered data analytics since more than a decade to identify insider trading patterns. The SEC’s 2018 Earnings Per Share Initiative applies risk-based analytics to detect accounting violations and has led to at least six enforcement actions. AI-related claims have risen sharply, as shown in a 2024 report that reveals these suits more than doubled compared to 2023, with 13 cases filed. SEC Chair Gary Gensler has cautioned against misleading AI-related disclosures and emphasized that “securities laws still apply”.

Conclusion

Securities class action lawsuits pose big challenges for companies in today’s complex regulatory environment. This piece explores these legal proceedings and the vital role regulatory bodies play in their outcomes.

The Securities Exchange Act of 1934, the Private Securities Litigation Reform Act, and the Sarbanes-Oxley Act are the foundations for these cases. Companies need to understand these frameworks because a single securities class action can lead to settlements over $13 million, with some cases reaching beyond $1 billion.

Material misstatements, major stock price drops, and SEC investigations trigger these lawsuits most often. Red flags like multiple Civil Investigative Demands, consumer harm allegations, and whistleblower disclosures draw extra regulatory attention that leads to formal litigation.

Federal and state regulators have built strong coordination systems to boost their enforcement capabilities. Their coordination creates what practitioners call a “unified front” against securities violations. This makes defense strategies more complex for targeted companies.

Parallel litigation makes things harder as companies often face securities class actions with derivative and antitrust lawsuits at the same time. These overlapping cases risk inconsistent rulings and increase defense costs and management burdens significantly.

Quick action is essential for companies facing securities class actions. They must activate legal and compliance teams right away, preserve documents fully, and bring in experienced securities litigation counsel to respond effectively.

New trends will alter the regulatory scene ahead. ESG-related disclosures get more attention now. Artificial intelligence and advanced data analytics are changing how fraud gets detected. Proposed changes to Rule 23 and the PSLRA might shift the legal landscape for these proceedings.

Securities class action litigation keeps evolving with regulatory priorities and enforcement methods. Companies that grasp these dynamics and prepare well can better handle these legal challenges when securities litigation comes their way.

Contact Timothy L. Miles Today for a Free Case Evaluation About Securities Class Action Lawsuits

If you need reprentation in a securities class action lawsuit or believe youhave a viable class action, call us today for a free case evaluation. 855-846-6529 or [email protected] (24/7/365).

Timothy L. Miles, Esq.

Law Offices of Timothy L. Miles

Tapestry at Brentwood Town Center

300 Centerview Dr. #247

Mailbox #1091

Brentwood,TN 37027

Phone: (855) Tim-MLaw (855-846-6529)

Email: [email protected]

Website: www.classactionlawyertn.com

Facebook Linkedin Pinterest youtube

Visit Our Extensive Investor Hub: Learning for Informed Investors