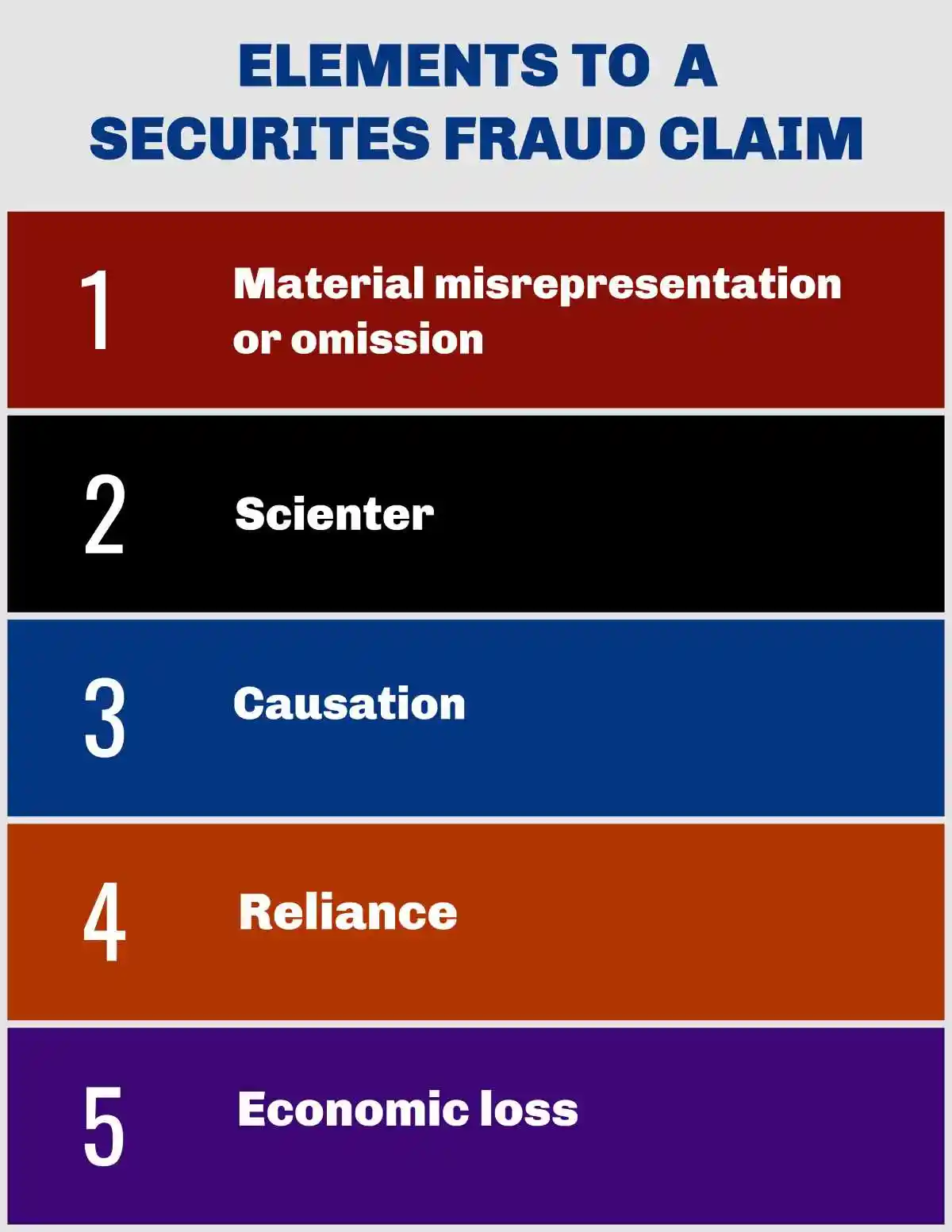

Introduction to Class Certification in Securities Litigation

- Class certification in securities litigation: Represents a pivotal judicial determination process governed by Federal Rule of Civil Procedure 23, where courts evaluate whether a lawsuit meets the stringent requirements to proceed as a class action. This critical determination serves as a fundamental gateway for shareholders seeking to pursue collective legal remedies against corporate defendants accused of securities violations.

- Requirements: For certification to be granted, plaintiffs must demonstrate several essential elements that justify class treatment. These include proving numerosity (sufficient class members to make individual joinder impracticable), establishing common questions of law or fact that predominate across the class, demonstrating that the representative plaintiffs’ claims typify those of the broader class, and showing that class action treatment represents the most efficient and equitable method for resolving the claims. Courts scrutinize these requirements rigorously, recognizing their role as gatekeepers in securities litigation.

- Critical Stage: The class certification stage stands as perhaps the most decisive moment in securities litigation, fundamentally altering the dynamics of the case. A grant of certification dramatically increases settlement pressure on defendants due to the aggregation of claims and potential damages exposure. Conversely, denial of certification often sounds the death knell for the litigation, as individual claims may lack sufficient economic viability to proceed independently.

The Purpose of Class Certification

- A Gatekeeper Stage: Class certification functions as a crucial threshold determination where judges must conduct a rigorous analysis of the evidence and make preliminary factual findings that frequently shape the entire trajectory of the litigation. This analysis often requires courts to analyze complex issues involving market efficiency, price impact, and damages methodologies, even when these issues overlap with the merits of the case. The process serves to ensure that only appropriate cases proceed as class actions, protecting both the judicial system’s resources and the interests of absent class members.

- Determines Viability: The certification decision essentially determines whether the case will continue as a meaningful litigation threat to defendants. Without certification, most securities cases effectively conclude, as the economics of individual prosecution rarely justify continued litigation. However, when certification is granted, the case transforms into a powerful vehicle for collective redress, potentially exposing defendants to substantial damages and creating significant pressure to reach a settlement agreement rather than risk an adverse jury verdict.

Key Requirements Under Federal Rule of Civil Procedure 23

- Numerosity: The class must be sufficiently large that joinder of all members individually would be impracticable. In securities cases involving publicly traded companies, this requirement is typically satisfied easily due to the dispersed nature of share ownership and the efficiency of modern securities markets.

- Commonality: The litigation must present questions of law or fact common to all class members. In securities cases, these often center around alleged misrepresentations or omissions in corporate disclosures, the adequacy of internal controls, and corporate governance practices that affected all shareholders similarly.

- Typicality: The claims of the designated class representatives must be typical of those held by the broader class. This ensures that by pursuing their own interests, the representatives will necessarily advance the interests of absent class members. Courts examine whether the representatives’ trading patterns and economic interests align with those of other class members.

- Adequate Representation: The named plaintiffs and their counsel must demonstrate their ability to protect the interests of all class members vigorously and competently. This includes examining potential conflicts of interest, the resources and experience of plaintiffs’ counsel, and the representatives’ understanding of their fiduciary obligations to the class.

- Predominance (for Rule 23(b)(3) claims): Common questions must predominate over individual issues, and class treatment must represent the superior method for fairly and efficiently adjudicating the controversy. This requirement often becomes a central battleground in securities litigation, particularly regarding damages calculations and causation issues.

Specific Issues in Securities Class Actions

- Price Impact: A critical focus of modern class certification battles involves demonstrating whether alleged misstatements or omissions actually affected the security’s market price. Defendants can defeat certification by showing no “price impact” from the challenged statements, thereby rebutting the fraud-on-the-market presumption of reliance that typically enables class treatment in securities cases.

- Damages Methodology: Plaintiffs must present a damages methodology capable of calculating class-wide damages through common proof. This typically involves sophisticated event studies measuring price inflation attributable to the alleged fraud and its dissipation following corrective disclosures. The methodology must align with the plaintiffs’ theory of liability and demonstrate that damages can be proven on a class-wide basis.

The Significance of Certification

- Settlement Pressure: Class certification dramatically alters the litigation dynamics by aggregating thousands of individual claims into a single proceeding. This aggregation creates substantial pressure on defendants to settle rather than risk potentially catastrophic damages at trial, even in cases where they believe they have strong defenses.

- The Merits of the Case: While class certification technically does not constitute a ruling on the merits, courts increasingly must examine merits issues that overlap with certification requirements. This preliminary merits review often shapes both parties’ assessment of the case’s strength and influences settlement negotiations.

Understanding Class Certification in Securities Litigation

- Class certification represents the most pivotal juncture in securities litigation, functioning as the critical gateway that determines whether individual investor claims can proceed collectively against corporate defendants. This determination fundamentally shapes the litigation landscape, influencing everything from settlement dynamics to the practical viability of pursuing claims for alleged violations of securities laws.

- Collective action: The class action mechanism serves as a transformative procedural tool in securities litigation, fundamentally altering the dynamics between plaintiffs and defendants. By consolidating numerous individual claims into a unified legal proceeding, this mechanism creates substantial leverage for investors while exposing corporate defendants to potentially significant financial liability. The aggregation of claims not only enhances judicial efficiency but also provides economically viable means for pursuing claims that might otherwise remain unaddressed due to individual litigation costs.

- The significance of class certification in securities litigation extends far beyond mere procedural convenience, representing a cornerstone of investor protection in modern financial markets. When shareholders suffer losses due to corporate misconduct, particularly involving accounting fraud or inadequate internal controls, individual claims often lack sufficient economic incentive for independent pursuit. The costs of complex financial litigation, including expert testimony and extensive discovery, frequently exceed potential individual recoveries, creating a practical barrier to justice without collective action mechanisms.

- Securities class actions have emerged as the primary vehicle for aggregating investor claims, serving multiple crucial functions in maintaining market integrity. These actions not only provide a pathway for investor compensation but also act as a powerful deterrent against corporate misconduct. By enabling collective pursuit of claims, they create sufficient economic incentive to challenge sophisticated financial fraud schemes and hold corporations accountable for breaches in corporate governance.

The Legal Framework: Essential Requirements for Class Certification

- To achieve class certification, plaintiffs must navigate a complex legal framework designed to ensure appropriate use of the class action mechanism. These requirements serve as essential safeguards, carefully balancing the efficiency benefits of collective action against fundamental due process rights. Courts conduct rigorous analysis of certification requirements, recognizing their role as gatekeepers in determining which cases merit class treatment.

- Common questions of law or fact represent the foundational requirement for class certification in securities litigation. This commonality requirement ensures that resolving key issues will advance the litigation for all class members simultaneously. In cases involving accounting fraud or misleading financial statements, commonality typically centers on whether corporate disclosures contained material misrepresentations or omissions that affected all investors similarly. Courts examine whether alleged violations of internal controls and corporate governance standards created common injury patterns across the shareholder base.

The superiority requirement demands comprehensive analysis of whether class treatment provides the most efficient and fair method for resolving investor claims. In securities litigation, this requirement frequently finds satisfaction due to the economic realities of modern securities markets. The dispersed nature of share ownership, combined with relatively modest individual losses, often makes class actions the only viable mechanism for pursuing relief. Courts consider various factors including:

- The potential for inconsistent judgments if claims proceed individually

- The benefits of concentrating litigation in a single forum

- The interests of class members in controlling their own litigation

- The manageability of class-wide proceedings

- The existence of alternative remedial mechanisms

The superiority analysis extends beyond mere convenience, requiring courts to evaluate practical considerations that impact the effective administration of justice. This includes assessing:

- The sophistication of potential class members

- The geographic dispersion of affected investors

- The complexity of proving damages on a class-wide basis

- The likelihood that individual members would pursue separate actions

- The judicial resources required for collective versus individual proceedings

Ascertainability demands that the proposed class definition permits objective determination of class membership. In securities litigation, this typically involves defining the class through specific criteria such as:

- Purchase or sale of securities during a defined class period

- Trading in particular securities affected by alleged misconduct

- Objective evidence of transactions through trading records

- Clear temporal boundaries based on corporate disclosures

Adequacy: Evaluating Representation and Conflicts of Interest requires courts to conduct detailed examination of both class representatives and counsel. This analysis focuses on:

- Representatives’ understanding of their fiduciary obligations

- Absence of conflicts between representatives and class members

- Counsel’s experience in complex securities litigation

- Financial resources available for vigorous prosecution

- Track record in similar class actions

- Quality of representation in current proceedings

Superiority: Why Class Action Is the Preferred Legal Mechanism

The second component of Rule 23(b)(3) requires courts to evaluate four key factors that demonstrate why class treatment represents the optimal approach:

- Individual Control Interest: Assessment of whether class members have significant interest in individually controlling separate actions

- Existing Litigation: Examination of any pending litigation concerning the same claims

- Forum Concentration: Benefits of consolidating claims in the selected venue

- Management Challenges: Practical difficulties in managing class proceedings

These factors typically support class certification in securities litigation because:

- Individual claims often lack economic viability

- Centralized proceedings promote judicial efficiency

- Common evidence predominates across claims

- Standardized damage calculations facilitate class-wide resolution

Superiority: Why Class Action Is the Preferred Legal Mechanism (continued)

- The evaluation of class members’ interests in controlling separate actions represents a critical factor in determining superiority. Courts carefully assess whether individual investors possess sufficient economic motivation and resources to pursue independent litigation. In cases involving securities litigation, particularly those stemming from accounting fraud or failures in internal controls, individual claims often lack the financial scale necessary to justify separate proceedings. The sophisticated nature of modern financial fraud schemes typically requires extensive expert testimony, complex discovery processes, and substantial litigation resources that make individual pursuit economically impractical.

- The extent of existing litigation on the controversy provides courts with valuable insight into the practical necessity of class treatment. When multiple individual actions already exist, courts evaluate whether consolidation through class certification would enhance judicial efficiency and promote consistent outcomes. This analysis becomes particularly relevant in cases involving alleged breaches of corporate governance standards, where multiple shareholders might have initiated separate proceedings in different jurisdictions.

Courts strongly favor concentrating claims in a particular forum when dealing with securities violations, especially those involving publicly traded companies with nationwide shareholder bases. This centralization offers numerous advantages:

- Prevents inconsistent judicial interpretations

- Reduces duplicative discovery efforts

- Maximizes judicial resource efficiency

- Facilitates comprehensive settlement negotiations

- Ensures uniform application of legal standards

The management challenges in administering class actions require careful judicial consideration. Courts evaluate practical difficulties such as:

- Providing adequate notice to class members

- Administering claims processes efficiently

- Calculating and distributing damages fairly

- Managing complex discovery procedures

- Coordinating multiple counsel effectively

Daubert Standard for Expert Testimony in Class Certification

The Daubert standard has emerged as a crucial gatekeeper for expert testimony in securities litigation, particularly during class certification proceedings. Courts must rigorously evaluate expert evidence according to several key criteria:

- Scientific testability of methodologies

- Peer review and publication status

- Known or potential error rates

- Existence of controlling standards

- General acceptance within relevant scientific communities

This heightened scrutiny becomes especially significant when experts testify about:

- Market efficiency assessments

- Loss causation analysis

- Damages calculations

- Corporate governance standards

- Internal control evaluations

The Fraud-on-the-Market Theory: Foundation for Modern Securities Class Actions

The Fraud-on-the-Market Theory serves as the cornerstone for contemporary securities litigation, particularly in cases involving publicly traded securities. This doctrine fundamentally transforms the traditional reliance requirement by establishing a rebuttable presumption that investors rely on the integrity of market prices. This presumption proves essential for class certification by eliminating the need to prove individual reliance, which would otherwise defeat class treatment.

The theory operates on several sophisticated assumptions about market behavior:

- Efficient markets incorporate all public information

- Material misrepresentations affect market prices

- Investors reasonably rely on market integrity

- Price distortions harm all market participants similarly

When companies engage in deceptive practices or accounting fraud, these misrepresentations typically create artificial price inflation. The subsequent revelation of truth through corrective disclosures often triggers significant price declines, leading to substantial investor losses and potential securities litigation. This price impact analysis has become increasingly central to class certification decisions, with courts requiring detailed evidence of:

- Market efficiency characteristics

- Materiality of alleged misrepresentations

- Clear price impact from disclosures

- Quantifiable investor damages

Class actions meeting superiority requirements demonstrate clear advantages in:

- Conserving judicial resources

- Reducing litigation costs

- Promoting consistent outcomes

- Enhancing access to justice

- Strengthening market integrity

However, superiority might face challenges when:

- State laws vary significantly

- Individual issues predominate

- Alternative remedies exist

- Management difficulties arise

- Conflicts emerge between class members

Predominance: Proving Common Issues Outweigh Individual Ones

- The fraud-on-the-market theory serves as a pivotal determinant of predominance in securities litigation, particularly in cases involving alleged accounting fraud. This foundational theory establishes a critical presumption of reliance for securities traded in efficient markets, fundamentally transforming how courts approach class certification.

- While individual damage calculations traditionally do not impede certification, the Ninth Circuit’s landmark decision in Bowerman v. Field Asset Services, Inc. introduced important nuances, suggesting class certification may face challenges when individual inquiries become necessary to establish the very existence of damages, rather than merely calculating their extent. This distinction has profound implications for securities class actions, especially those involving complex corporate governance failures or deficient internal controls.

Evidentiary Burden and Use of Expert Testimony

- Modern securities litigation relies extensively on sophisticated expert testimony, particularly during the critical class certification phase. Courts increasingly demand specialized financial and economic evidence to evaluate whether proposed classes satisfy certification requirements. The fraud-on-the-market theory remains central to securities class actions, with its application fundamentally dependent on demonstrating market efficiency.

- Courts systematically apply the comprehensive five-factor test established in Cammer v. Bloom to assess market efficiency, with particular emphasis on the fifth factor requiring expert testimony to establish clear cause-and-effect relationships between corporate events and stock price movements.

- This analytical framework operates on the sophisticated premise that efficient markets rapidly incorporate public information into stock prices without systematic bias. This market efficiency principle enables investors to reasonably rely on market price integrity rather than requiring direct proof of reliance on specific misstatements. Expert testimony often focuses on:

- Quantitative analysis of market efficiency indicators

- Statistical evidence of price responsiveness to new information

- Assessment of trading volume and analyst coverage

- Evaluation of bid-ask spreads and market maker activity

- Analysis of institutional ownership patterns

Materiality: The Cornerstone of Securities Fraud Claims

Materiality represents an essential element in securities class actions, particularly those involving accounting fraud or disclosure violations. Information achieves materiality status when there exists a substantial likelihood that reasonable investors would consider it significant in their investment decisions, or when it would fundamentally alter the total mix of available information in the market.

In cases centered on accounting fraud, materiality analysis typically involves demonstrating that misrepresented financial information carried sufficient significance to influence investor decision-making processes. This might encompass:

- Quantitative analysis showing substantial monetary impact relative to company size

- Assessment of effects on key performance indicators

- Evaluation of impact on critical financial metrics

- Documentation of concealed business challenges or trends

- Analysis of market reaction to corrective disclosures

The materiality assessment becomes particularly intricate in accounting fraud cases, requiring courts to evaluate whether specific accounting irregularities possessed sufficient significance to mislead reasonable investors. Key considerations include:

- Magnitude of financial misstatements

- Impact on reported earnings trends

- Effects on important financial ratios

- Influence on compliance with debt covenants

- Relationship to management compensation metrics

Loss Causation: Connecting Fraud to Financial Harm

- Loss causation emerges as one of the most complex elements to establish in securities class actions, demanding plaintiffs demonstrate direct causal links between alleged fraudulent conduct and specific financial losses. This requirement ensures defendants bear responsibility only for losses genuinely attributable to their misconduct rather than unrelated market factors.

- In cases involving accounting fraud, establishing loss causation typically requires demonstrating clear connections between stock price declines and revelations of previously concealed information through corrective disclosures. These revelations might emerge through various channels:

- Company press releases or SEC filings

- Regulatory investigation announcements

- Independent analyst reports

- Whistleblower disclosures

- Media investigations

- The analysis of loss causation often involves:

- Detailed event studies measuring price impacts

- Statistical analysis of market movements

- Expert testimony on causation chains

- Assessment of confounding factors

- Evaluation of industry-wide trends

- Courts increasingly scrutinize loss causation evidence, requiring:

- Clear identification of corrective disclosures

- Precise measurement of price impact

- Elimination of alternative causes

- Quantification of damages

- Documentation of causal mechanisms

- This heightened scrutiny reflects courts’ commitment to ensuring that securities litigation serves its intended purpose of compensating investors for actual fraud-related losses while preventing recovery for general market risks or unrelated business challenges. The analysis becomes particularly crucial in cases involving failures of internal controls or corporate governance, where establishing direct links between control deficiencies and specific losses often requires sophisticated expert analysis and compelling empirical evidence.

- The loss causation analysis in securities litigation presents unique complexities due to the multifaceted nature of stock price movements in modern financial markets. Stock values fluctuate continuously in response to numerous factors entirely unrelated to alleged fraudulent activities, including macroeconomic conditions, industry-specific developments, changes in competitive dynamics, and broader market sentiment. This inherent market volatility creates significant challenges for plaintiffs attempting to establish clear causal connections between specific instances of fraud and their resulting financial losses.

- In the context of securities litigation, plaintiffs bear the critical burden of disaggregating their total losses into distinct components. They must meticulously isolate and quantify the specific portion of their financial damages directly attributable to the alleged fraudulent conduct, distinguishing these losses from those stemming from:

- General market conditions and systematic risk factors

- Industry-wide trends and sector-specific challenges

- Company-specific developments unrelated to the fraud

- Macroeconomic events and policy changes

- Competitive pressures and market dynamics

- Other intervening events that may impact stock prices

CIRCUIT-BY-CIRCUIT ANALYSIS OF LOSS CAUSATION STANDARD

The federal circuits have developed varying approaches to loss causation requirements in securities litigation, reflecting different interpretations of pleading standards and causation evidence. This circuit-by-circuit analysis reveals important distinctions in how courts evaluate the relationship between corporate fraud and investor losses:

Circuit | Standard | Case Law | Notes |

First Circuit | Implements a relatively permissive standard under Rule 8(a), requiring plaintiffs to present only plausible allegations connecting corrective disclosures to preceding misrepresentations. The focus remains on establishing reasonable linkages rather than definitive proof at the pleading stage. | Massachusetts Retirement Systems v. CVS Caremark Corp. (2013) stands as the seminal case establishing this approach. | Aligns with circuits favoring “plausible” allegations over stringent particularity requirements, reflecting a more accessible path for plaintiffs demonstrating loss causation. |

Second Circuit | Mandates that plaintiffs demonstrate the fraudulent statement’s subject matter directly caused their actual losses. While particularized pleading isn’t required, the analysis emphasizes clear causal connections between specific misrepresentations and resulting damages. | Lentell v. Merrill Lynch & Co. (2005) and Emergent Capital Inv. Mgmt., LLC v. Stonepath Grp., Inc. (2003) establish the framework for evaluating these connections. | Employs “zone of risk” analysis focusing on whether misstatements concerned the precise facts leading to losses, emphasizing the importance of direct causal relationships. |

Third Circuit | Adopts a balanced approach under Rule 8(a), requiring plaintiffs to establish causal connections between misrepresentations and losses that exceed mere possibility or speculation without demanding excessive detail. | McCabe v. Ernst & Young, LLP (2007) and EP Medsystems, Inc. v. EchoCath, Inc. (2000) outline the circuit’s methodology. | Requires demonstration that fraudulent information’s revelation substantially contributed to stock value decline, balancing accessibility with evidentiary rigor. |

Fourth Circuit | Applies heightened Rule 9(b) pleading standards to loss causation claims, requiring detailed explanations of how corrective disclosures relate to prior misrepresentations. This approach demands greater specificity in establishing causal connections. | Katyle v. Penn National Gaming, Inc. (2011) and Teachers’ Ret. Sys. of LA v. Hunter (2007) exemplify this stringent approach. | Joins the Seventh and Ninth Circuits in requiring particularized pleading, setting a higher bar for plaintiffs establishing loss causation. |

Fifth Circuit | Imposes strict requirements for plaintiffs to demonstrate both specific revelation of fraud through corrective disclosures and direct causation of losses. This dual requirement creates a particularly demanding standard. | Pub. Emps. Ret. Sys. of Miss. v. Amedisys, Inc. (2014) and Lormand v. US Unwired, Inc. (2009) establish these rigorous requirements. | Maintains particularly stringent standards regarding connections between corrective disclosures and prior misrepresentations, emphasizing precision in causation evidence. |

Sixth Circuit | Follows a moderate approach balancing accessibility with evidentiary requirements, mandating clear causal connections without imposing Rule 9(b)’s heightened particularity standards. | Ohio Pub. Emps. Ret. Sys. v. Federal Home Loan Mortgage Corp. (2016) and IBEW Local 58 v. Royal Bank of Scotland (2013) define this balanced framework. | Focuses on whether disclosures revealed aspects of prior misrepresentations while maintaining reasonable pleading requirements. |

- This circuit-by-circuit variation in loss causation standards significantly impacts how companies approach internal controls and corporate governance practices. Organizations must carefully consider these differing standards when:

- Designing and implementing internal controls

- Establishing disclosure controls and procedures

- Developing risk management frameworks

- Creating compliance monitoring systems

- Structuring corporate governance mechanisms

- Preparing public disclosures and financial reports

- The evolving landscape of loss causation requirements continues to shape how companies approach risk management and disclosure practices, particularly in contexts involving potential securities litigation. This dynamic environment demands ongoing attention to:

- Emerging judicial interpretations

- Circuit-specific requirements

- Regulatory developments

- Industry best practices

- Risk management strategies

- Compliance frameworks

- Understanding these circuit-specific standards becomes crucial for shareholders and corporate stakeholders in evaluating litigation risks and implementing appropriate governance mechanisms to prevent and detect potential securities violations.

Circuit | Standard | Case Law | Notes |

Seventh Circuit | Implements a heightened Rule 9(b) pleading standard across all elements of securities fraud, including loss causation, requiring detailed particularity in establishing causal connections between misrepresentations and losses. | Tricontinental Industries v. PricewaterhouseCoopers (2007) and Ray v. Citigroup Global Markets (2007) establish this rigorous framework. | Aligns with the Fourth and Ninth Circuits in demanding particularized pleading, creating significant hurdles for plaintiffs in demonstrating loss causation through internal controls failures. |

- | Eighth Circuit | Takes a more lenient approach focused on notice pleading, requiring only that complaints provide defendants sufficient information about how alleged misrepresentations caused claimed losses. This standard emphasizes accessibility over technical precision. | In re Cerner Corp. Sec. Litig. (2005) and Schaaf v. Residential Funding Corp. (2008) demonstrate this more permissive approach to loss causation allegations. | Analyzes loss causation under Rule 8(a)’s more accessible framework, facilitating plaintiffs’ ability to establish connections between corporate governance failures and resulting damages.

- | Ninth Circuit | Strictly applies Rule 9(b)’s heightened pleading requirements to all fraud elements, demanding specific details connecting misrepresentations to losses through clear causal chains. | Oregon Public Employees Retirement Fund v. Apollo Group Inc. (2014) and Metzler Inv. GMBH v. Corinthian Colleges, Inc. (2008) solidified this approach after previous inconsistency. | The circuit’s definitive adoption of Rule 9(b) standards in Oregon Public Employees significantly impacts how plaintiffs must demonstrate causation in securities litigation.

- | Tenth Circuit | Adopts a balanced methodology requiring logical connections between misrepresentations and economic losses without explicitly mandating Rule 9(b) particularity. This approach seeks middle ground between strict and permissive standards. | In re Williams Sec. Litig. (2007) and Nakkhumpun v. Taylor (2015) outline requirements for establishing these logical links. | Centers analysis on whether disclosures revealed aspects of prior misrepresentations, particularly those related to failures in internal controls.

- | Eleventh Circuit | Requires plaintiffs to demonstrate misrepresentations served as “substantial or significant contributing factors” in losses while generally following Rule 8(a)’s framework. This creates a hybrid standard emphasizing causation strength. | Hubbard v. BankAtlantic Bancorp, Inc. (2012) and FindWhat Investor Group v. FindWhat.com (2011) establish this distinctive approach. | Emphasizes proximate causation principles while maintaining relatively accessible pleading requirements, particularly in cases involving corporate governance failures.

- | D.C. Circuit | Maintains limited securities fraud jurisprudence but generally follows a more permissive approach aligned with Rule 8(a), focusing on plausible causal connections rather than technical precision. | Plumbers & Steamfitters Local 773 Pension Fund v. Danske Bank (2020) exemplifies this developing framework. | Generally adheres to Supreme Court guidance from Dura Pharmaceuticals without imposing additional heightened requirements in securities litigation.

The Role of Event Studies in Securities Litigation

- Event studies have emerged as essential analytical tools in modern securities litigation, providing sophisticated statistical methodologies for measuring specific events’ impact on stock prices. These studies serve crucial functions in establishing both materiality and loss causation by:

- Isolating market reactions to particular disclosures

- Controlling for general market movements

- Quantifying stock price impacts

- Distinguishing fraud-related losses

- Supporting damage calculations

- Demonstrating causation elements

- The importance of event studies in securities cases reflects courts’ increasing emphasis on empirical evidence demonstrating clear causal connections between corporate misrepresentations and investor losses. These studies help address the complex challenges of:

- Disaggregating multiple causal factors

- Establishing precise timing relationships

- Quantifying specific damage components

- Supporting loss causation arguments

- Demonstrating materiality requirements

- Evaluating market efficiency claims

- This analytical approach particularly benefits cases involving:

- Failed internal controls

- Inadequate corporate governance

- Financial reporting irregularities

- Disclosure violations

- Accounting fraud allegations

- Market manipulation claims

- The growing reliance on event studies reflects broader trends toward quantitative analysis in securities litigation, especially when evaluating causation and damages. This evolution continues shaping how courts approach:

- Causation standards

- Damage calculations

- Class certification decisions

- Summary judgment motions

- Expert testimony requirements

- Settlement evaluations

- Use of event studies in securities class actions has become increasingly sophisticated, employing advanced statistical methodologies to analyze stock price movements around critical disclosure dates. These studies meticulously examine price reactions when allegedly fraudulent information enters the market or when corrective disclosures reveal the truth.

- By implementing complex regression analyses that control for broader market movements, industry-specific factors, and general economic conditions, event studies can precisely quantify the financial impact of specific corporate disclosures on shareholder value.

- In cases involving accounting fraud, event studies play a particularly crucial role by examining multiple types of market reactions. These include responses to:

- Initial earnings announcements containing potentially misleading information

- Financial restatements that correct previous misstatements

- Disclosures of regulatory investigations into accounting practices

Revelations of weaknesses in internal controls

- News of executive departures related to accounting issues

- The empirical evidence provided by these studies becomes instrumental in establishing the causal link between fraudulent disclosures and investor losses, a critical element in securities litigation.

- The methodology behind event studies represents a convergence of financial economics and statistical analysis, employing sophisticated techniques that have gained widespread acceptance in courts. These methods:

- Utilize regression analysis to isolate company-specific price movements

- Apply statistical significance tests to verify causation

- Account for confounding events that could impact price movements

- Consider trading volume and market liquidity factors

- Evaluate market efficiency assumptions

- Incorporate industry-specific benchmarks

- Assess the timing and magnitude of price reactions

This rigorous analytical framework helps judges and juries understand how efficient markets process information and how fraudulent disclosures can distort normal price discovery mechanisms, particularly in cases involving failures of corporate governance.

Strategic Implications for Litigation Parties

- The class certification decision fundamentally reshapes the litigation landscape in securities litigation, creating significant strategic considerations for all parties involved. For plaintiffs, successful certification:

- Provides essential economies of scale in complex litigation

- Enables cost-effective pursuit of sophisticated expert analysis

- Creates settlement leverage through aggregated claims

- Facilitates access to institutional resources

- Allows efficient case management

- Supports comprehensive discovery efforts

- Enables effective use of event studies

Defendants facing potential class certification must conduct comprehensive risk assessments that consider:

- Potential aggregate damages across the entire class

- Litigation costs through trial

- Insurance coverage limitations

- Impact on ongoing operations

- Reputational consequences

- Shareholder relations implications

- Regulatory exposure

- Settlement timing considerations

- The transformation of individual claims into class actions can exponentially increase potential liability, often reaching hundreds of millions or billions of dollars, particularly in cases involving accounting fraud.

Securities class actions involving accounting irregularities present unique challenges:

- Complex documentary evidence spanning multiple reporting periods

- Technical expert testimony on accounting standards

- Detailed analysis of internal controls

- Extensive electronic discovery requirements

- Multiple expert witnesses

- Complex damage calculations

- Extended discovery periods

- Sophisticated event studies

- These cases typically require substantial resources even when defending against claims that may ultimately prove unfounded.

- Role of the Lead Plaintiff Under the PSLRA

Lead Plaintiff Role: The PSLRA revolutionized securities class action procedure by establishing a formalized lead plaintiff selection process focused on identifying the “most adequate plaintiff.” This presumption typically favors:

- Institutional investors with substantial losses

- Sophisticated investors with significant stakes

- Parties with demonstrated oversight capabilities

- Entities with substantial resources

- Plaintiffs with clear alignment of interests

- Parties without conflicts of interest

- Investors with proven track records

- The presumption can only be overcome through clear evidence that the proposed lead plaintiff:

- Cannot fairly represent class interests

- Faces unique defenses

- Has conflicts with class members

- Lacks adequate resources

- Shows insufficient commitment

- Demonstrates inadequate sophistication

- Has questionable credibility

Lead Plaintiff Responsibilities: Lead plaintiffs must fulfill numerous obligations including:

- Filing detailed certifications

- Reviewing complaint allegations

- Authorizing litigation decisions

- Participating in discovery

- Attending court proceedings

- Monitoring counsel activities

- Evaluating settlement offers

- Protecting class interests

- They must also certify that:

- Their purchase was not counsel-directed

- They will actively serve as representatives

- They understand their fiduciary duties

- They will provide transaction details

- They will disclose other actions

- They accept limitations on recovery

- They will maintain ongoing oversight

Evolving Standards and Future Considerations

- The landscape of class certification in securities litigation continues to evolve as courts refine their approach to emerging issues and new forms of corporate misconduct. Recent developments have placed heightened emphasis on rigorous analysis of class certification requirements, particularly in cases involving complex financial instruments and sophisticated market manipulation schemes. Courts increasingly demand detailed evidence demonstrating that proposed classes satisfy all Rule 23 prerequisites, with special attention to issues of commonality and predominance in cases alleging violations of securities laws and failures of internal controls.

- Courts are increasingly scrutinizing the Fraud-on-the-Market Theory with unprecedented rigor, requiring plaintiffs to present sophisticated empirical evidence of market efficiency and price impact. This heightened scrutiny reflects judicial recognition that modern financial markets operate with varying degrees of efficiency across different securities and time periods. Courts now demand detailed event studies and expert testimony analyzing:

- The relationship between corporate disclosures and stock price movements

- Statistical significance of price reactions to new information

- Market efficiency indicators such as trading volume and analyst coverage

The impact of corporate governance failures on market pricing

- Evidence of price correction following corrective disclosures

- The role of confounding factors in price movements

- Quantification of damages through sophisticated modeling

The integration of advanced statistical methods and event studies has revolutionized how courts evaluate causation and damages in securities litigation. Modern analytical techniques now enable:

- More precise isolation of company-specific price movements

- Better control for industry and market-wide factors

- Enhanced analysis of market efficiency metrics

- More accurate damage calculations

- Sophisticated examination of price impact

- Detailed analysis of trading patterns

- Comprehensive evaluation of loss causation

- These advanced methods have significantly improved the precision of securities litigation analysis while simultaneously increasing case complexity and costs. Courts must carefully balance the benefits of enhanced analytical precision against practical considerations of judicial economy and jury comprehension.

Class certification in securities litigation continues to evolve in response to:

- Emerging forms of market manipulation

- New financial instruments and trading strategies

- Complex corporate structures and relationships

- Sophisticated accounting schemes

- International market interactions

- Technological advances in trading

- Evolving regulatory frameworks

- Changes in market structure

- The intersection of these factors with traditional legal principles creates ongoing challenges for courts applying class certification standards in modern securities cases.

The stakes involved in class certification decisions have never been higher, with potential damages often reaching billions of dollars. These high stakes reflect:

- Increased market capitalization of public companies

- Growing sophistication of trading strategies

- Expanded scope of corporate operations

- Complex international business structures

- Enhanced regulatory requirements

- Stricter internal controls standards

- Greater investor sophistication

- Expanded shareholder rights

- The magnitude of potential liability underscores the critical importance of thorough analysis at the certification stage.

As securities class actions continue serving as primary enforcement mechanisms, courts must balance:

- Investor protection objectives

- Corporate defense rights

- Judicial efficiency concerns

- Market integrity goals

- Regulatory compliance requirements

- International coordination needs

- Resource allocation issues

- Practical litigation management

This balancing act ensures that class certification remains a crucial battleground where fundamental questions of investor rights and corporate responsibilities are defined and enforced.

Frequently Asked Questions about Class

Certification in Securities Class Action Litigation

Q1. What are the key requirements for certifying securities class action lawsuits? Class certification requires satisfaction of Rule 23(a) prerequisites:

Numerosity: Sufficient class size making joinder impracticable

Commonality: Questions of law or fact common to the class

Typicality: Representative claims typical of class claims

Adequacy: Fair and adequate protection of class interests

Additionally, Rule 23(b)(3) requirements must be met:

Predominance of common questions over individual issues

Superiority of class action for fair and efficient adjudication

Manageability of litigation as a class action

Effectiveness of notice to class members

Q2. How many plaintiffs are typically needed to meet class certification requirements? While no strict numerical threshold exists, courts generally find numerosity satisfied with:

40 or more class members in traditional cases

Smaller numbers in complex securities cases

Larger numbers in simple cases

Variable thresholds based on:

Geographic dispersion

Size of individual claims

Judicial economy factors

Practical considerations

In securities fraud cases involving publicly traded companies, numerosity is rarely contested due to widespread share ownership and trading volume.

Q3. What role does expert testimony play in securities class action certification? Expert testimony proves crucial in establishing:

Market efficiency through empirical analysis

Price impact through event studies

Damages through economic models

Causation through statistical analysis

Trading patterns through market data

Corporate governance failures through institutional analysis

Internal control weaknesses through compliance review

Industry standards through comparative studies

Courts rely heavily on expert analysis to evaluate:

Fraud-on-the-market presumption

Loss causation methodology

Damage calculation approaches

Market efficiency metrics

Price impact evidence

Trading volume analysis

Statistical significance tests

Economic models

This expert testimony helps courts determine whether proposed classes satisfy certification requirements while providing essential frameworks for analyzing complex market behavior and corporate misconduct.

Q4. How does the Private Securities Litigation Reform Act (PSLRA) affect the lead plaintiff selection process?

The PSLRA fundamentally transformed the lead plaintiff selection process in securities litigation by establishing rigorous criteria and procedures. Courts must appoint the “most adequate plaintiff,” presumptively the investor or group with the largest financial stake in the litigation outcome. This requirement aims to ensure that sophisticated investors with substantial losses guide the litigation rather than allowing cases to be driven primarily by attorneys. The lead plaintiff bears extensive responsibilities, including filing detailed sworn certifications attesting to their trading history, demonstrating their capacity to actively oversee counsel, and proving their ability to fairly represent the entire class’s interests.

The Act requires courts to evaluate multiple factors when selecting lead plaintiffs, including:

Financial interest in the relief sought

Typicality and adequacy of claims

Ability to monitor class counsel

Experience in managing complex litigation

Understanding of corporate governance issues

Commitment to protecting class interests

Resources to sustain lengthy litigation

Freedom from unique defenses

These requirements promote institutional investor leadership in securities class actions while ensuring robust representation of class interests through enhanced scrutiny of lead plaintiff qualifications and capabilities.

Q5. What strategies do defendants commonly use to challenge class certification requirements in securities cases?

Defendants employ sophisticated multi-faceted approaches to challenge class certification, particularly focusing on undermining the predominance requirement through demonstration of individualized issues. Common defense strategies include:

Attacking market efficiency assumptions by:

Highlighting irregular price movements

Demonstrating weak analyst coverage

Showing inconsistent trading volumes

Identifying market maker influences

Proving information absorption delays

Documenting pricing inefficiencies

Challenging proposed damages models by:

Exposing methodology flaws

Identifying confounding factors

Demonstrating calculation impossibilities

Highlighting individualized damage issues

Questioning loss causation assumptions

Disputing price impact evidence

Emphasizing individual investor differences through:

Varying sophistication levels

Different investment strategies

Distinct reliance patterns

Unique trading histories

Specific risk tolerances

Particular investment goals

Retaining expert witnesses to:

Counter plaintiff efficiency analyses

Challenge price impact studies

Question damage calculations

Dispute causation theories

Examine internal controls

Evaluate market conditions

Defendants also frequently focus on demonstrating the named plaintiff’s atypical circumstances, gathering evidence of differing experiences among potential class members, and highlighting variations in investor knowledge and sophistication that could defeat commonality requirements.

Contact Timothy L. Miles Today for a Free Case Evaluation

If you suffered substantial losses and wish to serve as lead plaintiff in a securities class action, or have questions about securities class action settlements, or just general questions about your rights as a shareholder, please contact attorney Timothy L. Miles of the Law Offices of Timothy L. Miles, at no cost, by calling 855/846-6529 or via e-mail at [email protected]. (24/7/365).

Timothy L. Miles, Esq.

Law Offices of Timothy L. Miles

Tapestry at Brentwood Town Center

300 Centerview Dr. #247

Mailbox #1091

Brentwood,TN 37027

Phone: (855) Tim-MLaw (855-846-6529)

Email: [email protected]

Website: www.classactionlawyertn.com

- Facebook Linkedin Pinterest youtube

- Visit Our Extensive Investor Hub: Learning for Informed Investors